[ad_1]

The following is adapted from the “Women and Finance: The 2022 Rich Thinking Quantitative Survey Findings” report by Barbara Stewart, CFA, and Duncan Stewart CFA.

Given all the changes in investing behavior I was seeing as I conducted my interviews over the past couple of years, I wanted to ask six questions and measure how women’s behavior was changing since the COVID-19 pandemic went global in March 2020.

- How many women were investing in assets aside from their own homes?

- How many were investing using online platforms?

- How many were talking to their friends, family, or colleagues about investing?

- How many were interacting with other women investors online through social communities?

- How many were investing in blockchain-enabled assets, such as bitcoin or non-fungible tokens (NFTs)?

- How many were investing in environmental, social, and governance (ESG) or sustainable and diverse assets?

I happen to be married to a global expert on the design, analysis, and interpretation of consumer surveys. Duncan Stewart, CFA, usually does this kind of work on tech-, media-, and telecom-related topics for his employer, but he’s also deeply interested in the topic of women and investing, and I am thrilled to have him as coauthor.

We surveyed more than 2,000 women aged 18 to 75 online between 10 and 12 November 2021 in five countries: 1,057 in the United States — a large enough sample to do statistically significant analysis by age cohorts and income brackets — and 250 each in the United Kingdom, Singapore, Sweden, and Denmark.

Six Shocking Findings

- 64% of 18-to-29-year-old US women already invest or plan to within the year.

- 90% of US women investors aged 18 to 59 use online platforms compared to only 40% of US women investors over 60.

- Globally, 24% of women started talking with friends, family, or colleagues about investing since the start of the pandemic.

- About 90% of Swedish and Danish women investors interact with other women about investing in online social communities. That is double the rate of US women.

- 9% of US women over 60 already invest in blockchain-enabled assets, such as bitcoin, and another 5% plan to start in the next year.

- Young US women aged 18 to 29 are almost three times more likely to invest or plan to invest in environmental, social, and governance (ESG) assets than US women over 60.

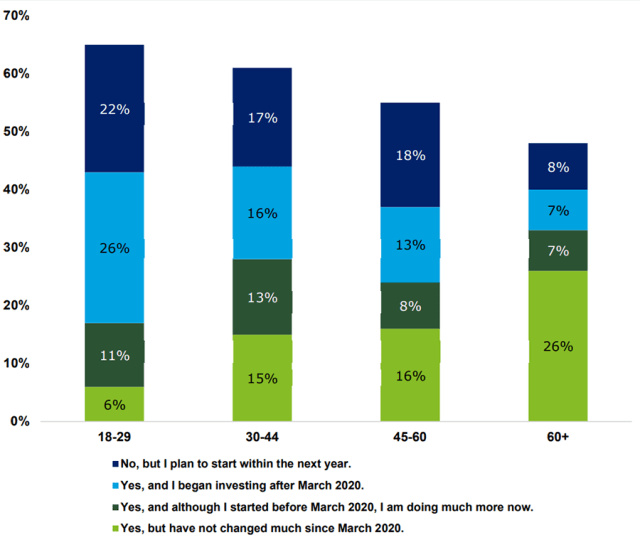

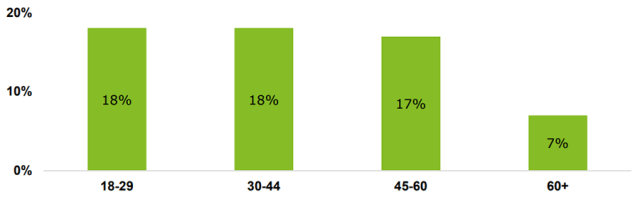

1. Do you invest in any asset classes other than your own home: stocks, bonds, mutual funds, ETFs, alternative assets such as cryptocurrencies, and so on?

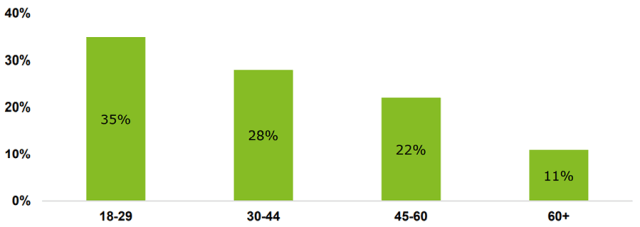

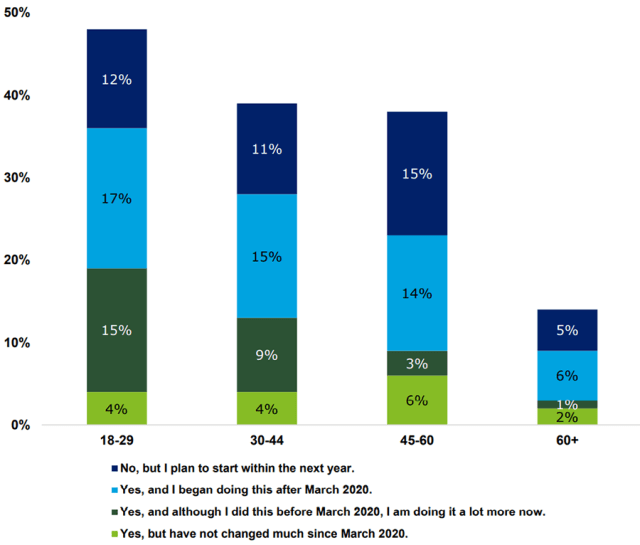

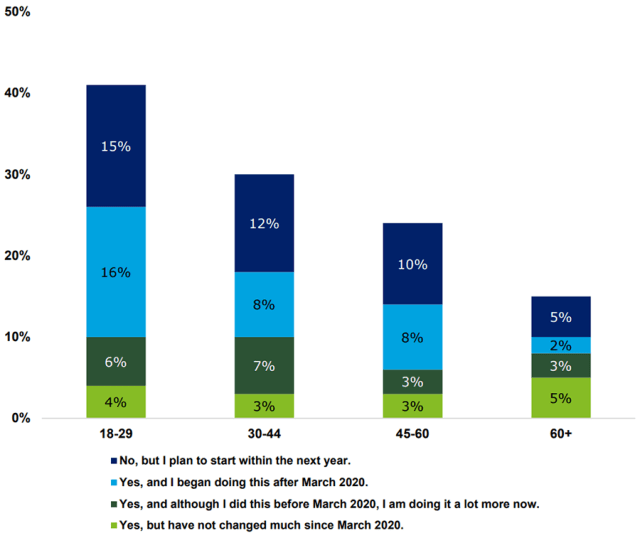

The kids are alright.

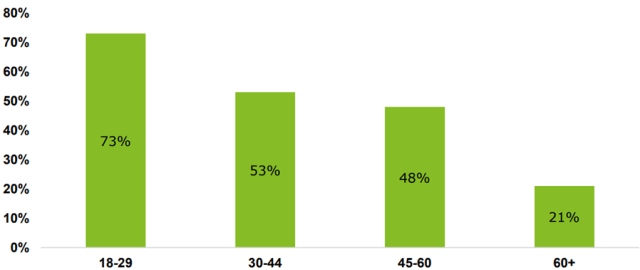

An amazing 64% of US women aged 18 to 29 either invest already or plan to invest within the year. That’s a higher percentage than any other age group, and even when we look at only those actually investing, more than four in 10 US women aged 18 to 44 are investing for their futures. This is a recent development for the youngest cohort: More than half of current investors started only after March 2020, just 20 months prior to this survey. Of course, more than a third of those over age 60 were investing prior to the pandemic.

Given the growth rates we’re seeing around actions and intentions, the clichés about young women and investing have been shattered.

US Women Investing in Any Non-Home-Ownership Assets, by Age Group

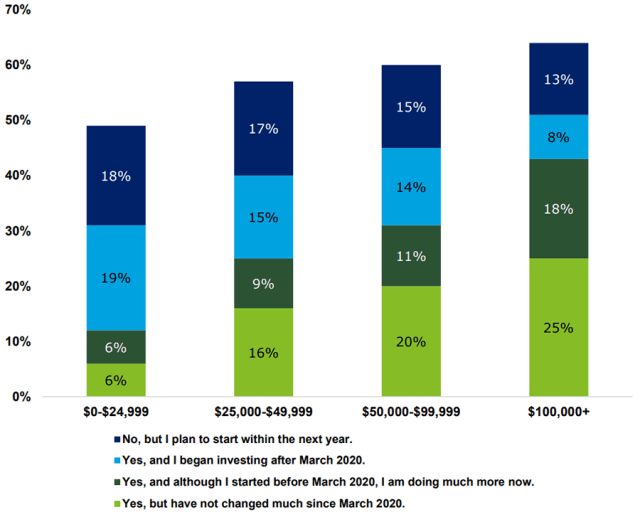

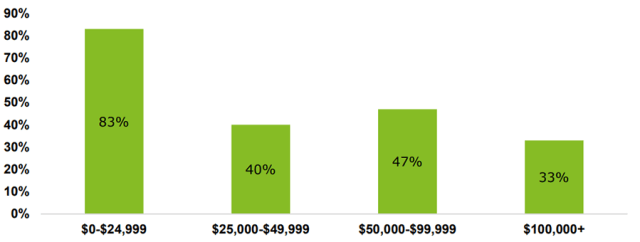

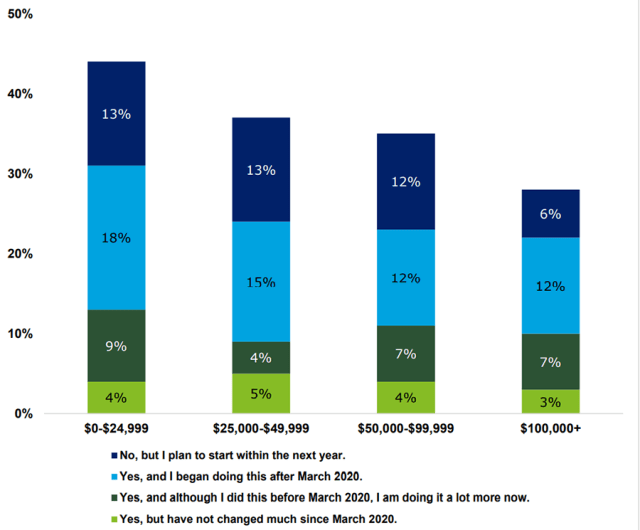

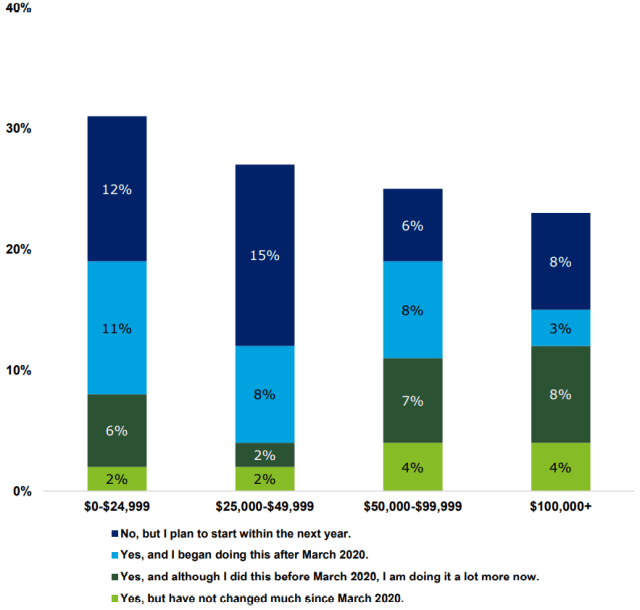

Money matters.

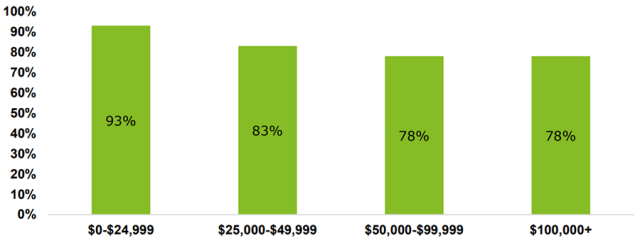

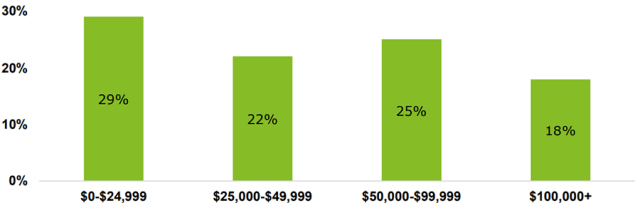

Higher-income US women are more likely to invest and more likely to invest more since March 2020. Where it gets really interesting is around lower-income US women: The median US household income is $79,900 and one in five women with household incomes below $25,000 started investing since the beginning of the pandemic, over 30% are currently investing, and another 18% intend to start within 12 months. This feels new and different.

One final observation: One in seven US women in the highest income bracket also plan on just “getting started” in investing. Since over half were already investing, doesn’t this suggest the sky’s the limit?

US Women Investing in Any Non-Home-Ownership Assets, by Household Income

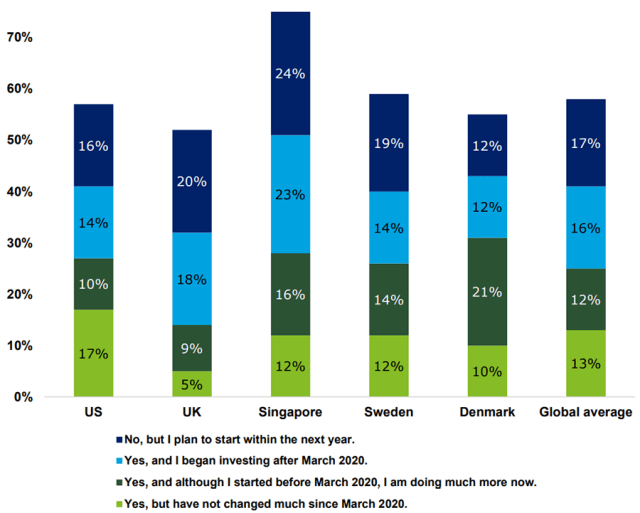

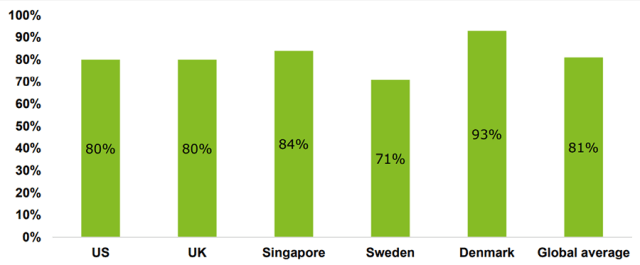

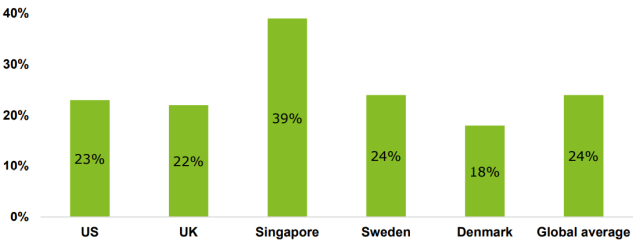

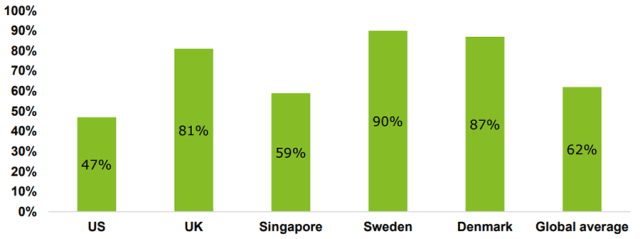

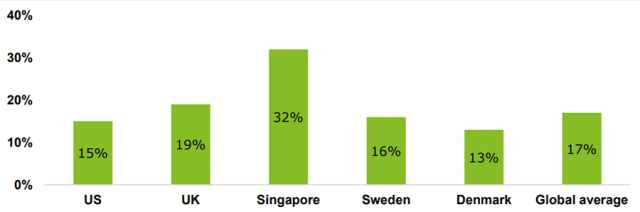

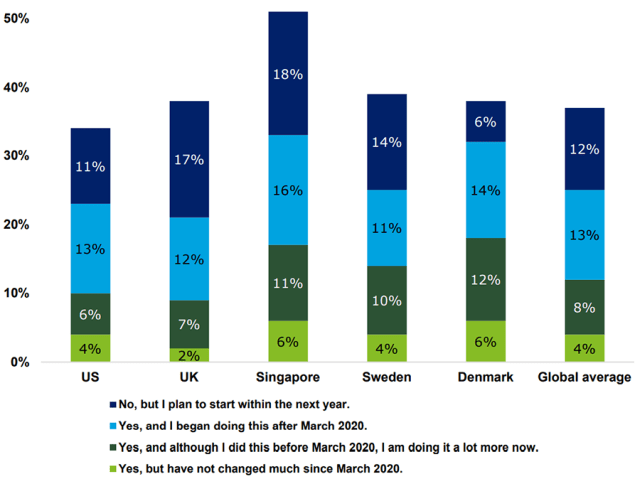

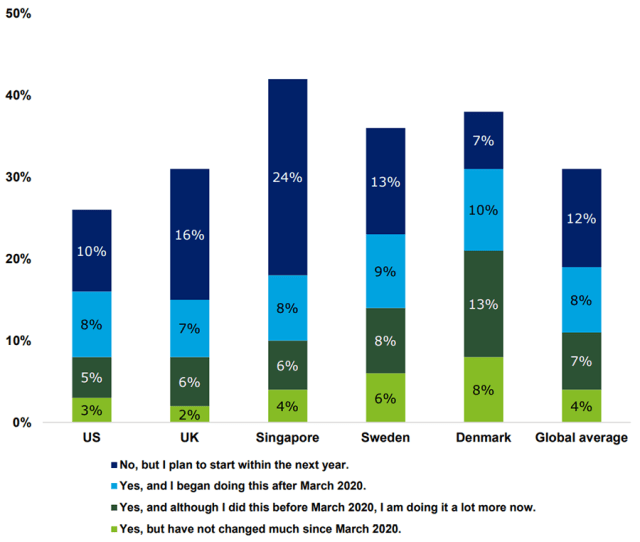

One of these things is not like the others.

Singaporean women are reinforcing their country’s money-savvy reputation: Over half are already investing and another quarter are preparing to dive in over the next year. Still, this is a relatively new development: A quarter of Singaporean women started to invest after March 2020.

The United Kingdom jumps out at the other end of the spectrum: Although 20% of respondents intend to start investing, fewer than a third had taken the plunge as of November 2021. That’s well below the global average of 41%. Moreover, only 14% were investing pre-pandemic. In the Nordics, Swedish and Danish women showed fairly similar investing habits.

Women Investing in Any Non-Home-Ownership Assets, by Country

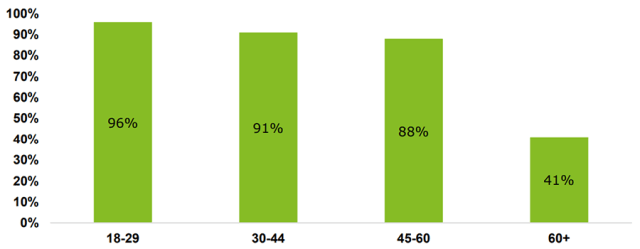

2. Do you invest using an online platform, such as Robinhood, E*TRADE, or others?

Mind the gap — the generation gap.

There is a demographic cliff on this topic: US women investors over 60 are less than half as likely to use an online platform as their younger peers. Among 18-to-29-year-old US women investors, meanwhile, these platforms are ubiquitous.

Although women investors aged 30–60 are a little less likely to invest using online platforms than the youngest cohort, they are still highly likely, at 90% or more. Remarkably, though almost one in three 18-to-29-year-old US women don’t invest, 60% intend to make the leap on an online platform. The age gap in online platforms is wide for senior women, with only 11% of those over 60 expressing any interest. Given the trends, that gap looks like it will widen even further. Still, the over-60 crowd may have larger or more complex portfolios and may therefore prefer traditional wealth management advisers over digital alternatives.

Of US Women Who Invest, Percentage Using an Online Platform, by Age Group

Of US Women Who Don’t Invest, Percentage Planning to Start Using an Online Platform, by Age Group

Unpacking Time

The two following charts make for complicated analysis. Higher incomes often correlate with older age groups that may not be as technology savvy and open to online platforms as their younger peers. At the same time, higher incomes also mean bigger and more complicated portfolios. So, are US women with household incomes over $50,000 less likely to use online platforms because they are averse to technology or are they more inclined towards traditional investment advisers because of the greater size and complexity of their portfolios?

The same questions can be asked about the (relatively) low intent among those who are not currently investing but plan to start using an online investing platform in the next 12 months.

Of US Women Who Invest, Percentage Using an Online Platform, by Household Income

Of US Women Who Don’t Invest, Percentage Planning to Start Using an Online Platform, by Household Income

It’s a Scandinavian Split.

Women in Sweden and Denmark tend to have fairly similar habits around money and investing — but not when it comes to online platforms. The other countries surveyed are close to the global average of 80% in online platforms. But there’s a 22-percentage point gap between online-platform users in Denmark and their Swedish counterparts. Further work is needed to explain that gulf.

On the other side, of the 50% of Singaporean women who are not yet investing, nearly 40% say they intend to start on a digital platform. The equivalent figure in Denmark is only 18%, which may reflect Danish women’s already-high engagement on these platforms.

Of Women Who Invest, Percentage Using an Online Platform, by Country

Of Women Who Don’t Invest, Percentage Planning to Start Using an Online Platform, by Country

3. Do you talk about investing with your friends, family, or colleagues?

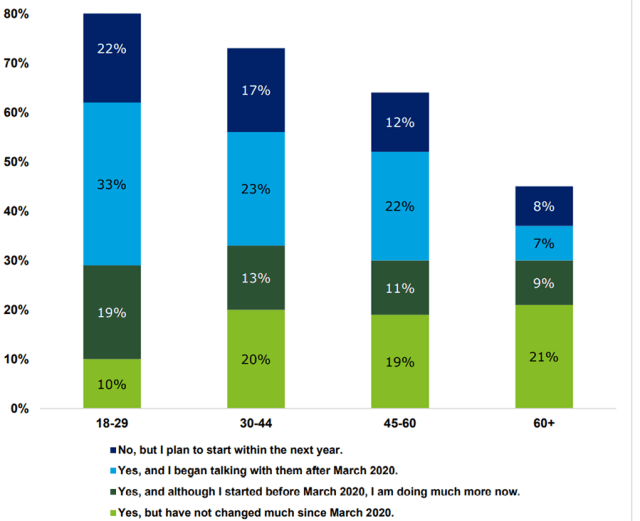

A Pandemic Shift

Roughly 30% of US women in all age groups spoke about investing with friends, family, or colleagues before March 2020. But while 7% of women over 60 began conversations after that date, three times as many women aged 30 to 60 and almost five times as many aged 18 to 29 did as well.

Why was COVID-19 such an inflection point for all but the oldest age group? We think the pandemic was more disruptive for those under 60. Lockdowns and work- and study-from-home arrangements all pushed younger women to change their habits more than their older peers. Being at home, being online, and perhaps feeling a novel sense of isolation and lack of physical community may have encouraged these women to reach out more about investing and probably other topics as well.

Among the youngest cohort, 22% plan on speaking about the topic within the year. If they do, four out of five young US women will be chatting about investing by the end of 2022.

US Women Who Talk about Investing with Friends, Family, or Colleagues, by Age Group

Money matters again.

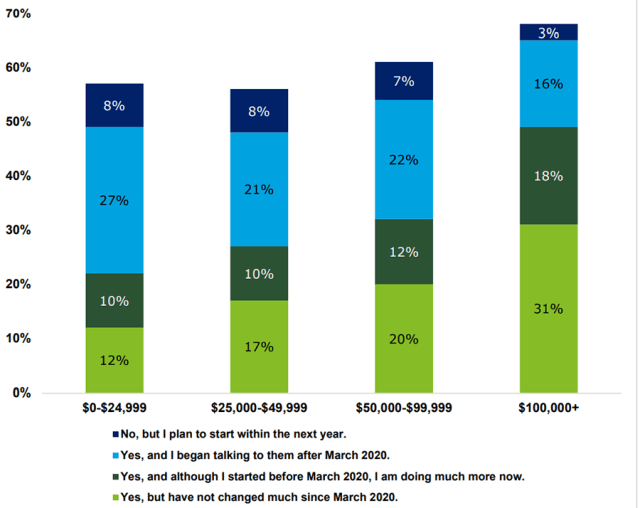

Prior to March 2020, US women with higher household incomes were more likely to talk about investing than those from lower income households. Nearly half of women with incomes over $100,000 were discussing investing, compared to only 22% of those making less than $25,000 annually.

But that lowest income group could be catching up. One in four are beginning to have investing conversations. Since lower incomes skew younger, the same age-related factors mentioned above may be driving this trend. Nevertheless, while the income-related investing “conversation gap” was quite large pre-pandemic, it may be closing, and 60% to 70% of US women of all incomes could soon be having these discussions.

US Women Who Talk about Investing with Friends, Family, or Colleagues, by Income

Keep Calm (and Don’t Talk about Money)

The British are renowned for their reticence around financial matters, and pre-pandemic only 24% of UK women surveyed spoke about investing with their friends, family or colleagues. That compares to a 31% global average.

But there has been a change since March 2020. More than a quarter of UK women are now chatting about investing, and another 7% plan to in the next year.

It’s interesting how uniform this habit will be by the end of this year: Across the United States, United Kingdom, Sweden, and Denmark, 60% to 62% of women discuss investing. Singapore is the obvious outlier, with more than three quarters of women surveyed talking about investing. But based on Barbara’s interviews with women in Singapore, that finding isn’t unexpected.

Women Who Talk about Investing with Friends, Family, or Colleagues, by Country

Sweden, n=250, and for Denmark n=250. Q. Do you talk about investing with your friends, family, or colleagues?

4. Do you interact with other female investors via an online social community such as Facebook, eToro, or others?

Not a surprise.

Since younger women are much more likely to use social media and online networks, it makes sense that they’d discuss investing on these platforms to a greater extent than their older peers. But the gap between younger US women and those over 60 is striking. Nearly half of 60-plus US women are on social media, they just don’t talk about investing on them. Nor does it look like they are about to start: Only 7% of non-investors over 60 say they plan to use these platforms to communicate about investing in the next year.

Of US Women Investors, Percentage Interacting via Online Social Communities, by Age Group

Of US Women Who Don’t Invest, Percentage Planning to Start Interacting via Online Social Communities, by household Income

Household Income: Two Factors at Work

Those with lower annual household incomes are likely to be younger — and over-index on the use of social platforms — and they also might access these communities for pricing reasons. Paying for full-service brokers or research may make sense when your household income is six figures or above, but free or low-cost online advice looks much more compelling to those in the lower income brackets.

Of US Women Investors, Percentage Interacting via Online Social Communities, by Household Income

Of US Women Who Don’t Invest, Percentage Planning to Start Interacting via Online Social Communities, by Household Income

Nordic women are leaders.

Barbara knew based on years of research on investing’s online social communities that these networks were more popular in Europe and the Nordics in particular. That about 90% of women who invest in Sweden and Denmark are using social communities to share ideas, do their research, and even compete against other investors was no shock to her. Although the United States is trailing on this, nearly half of US women already access these networks. In Singapore, meanwhile, almost one in three women who don’t invest plan to interact with these investing communities in the year ahead.

Of Women Investors, Percentage Planning to Start Interacting via Online Social Communities, by Country

Of Women Who Don’t Invest, Percentage Planning to Start Interacting via Online Social Communities, by Country

Sweden, n=250, and for Denmark, n=250. Q. Do you interact with other female investors via an online social community such as Facebook, eToro, or others?

5.Do you invest in any blockchain-enabled assets, such as bitcoin, other cryptocurrencies, or NFTs?

When it comes to crypto, you’re never too old for FOMO

Nearly half of US women aged 19 to 29 either invest in blockchain-enabled assets or plan to within the year. The pandemic was a big accelerant: Investing in this category among all age groups has picked up since March 2020.

There are two ways of looking at the over-60 cohort and crypto: As an age group, over 60s are much less likely to invest in bitcoin and the like. On the other hand, they are emphatically not at zero when it comes to this asset class. Almost one in 10 US women over 60 already invest in it and another 5% are planning to. Also, since only 39% of women in this cohort say they invest in any non-real estate asset class and 9% are investing in blockchain assets, that means about a quarter of women investors over 60 hold some crypto.

US Women Investing in Blockchain-Enabled Assets, by Age Group

You don’t have to be rich to invest in blockchain-enabled assets.

Because younger women tend to have lower incomes, the high proportion of lower-income women who are investing in crypto assets may be an age effect. On the whole, a very consistent 23% to 24% of those with incomes over $25K already invest in these products, with 19% in each income bracket saying they started investing or are investing more since the beginning of the pandemic.

Only 6% of women with household incomes over $100,000 plan on investing in digital assets over the next year — that’s half the rate of all other income brackets. Is that because crypto and NFTs are seen by some as more like “get-rich-quick” schemes and lottery tickets than actual investments?

US Women Investing in Blockchain-Enabled Assets, by Income

The Blockchain Sun rises in the East . . . Southeast Asia, that is.

More than half of the Singaporean women surveyed either already invest in blockchain-enabled assets or plan to within the year. That’s well ahead of women in all the other countries. The United States and the UK trail Singapore and the Nordics in this regard, and only 11% of US and 6% of Danish women plan to start investing in these assets. This is both surprising and much lower than in the other nations surveyed.

Another interesting data point: When actual investing and intent to invest in these products are combined, Sweden and Denmark are tied. The Danish were quicker to invest in blockchain assets — 18% of respondents were already invested prior to March 2020 — but the Swedes look poised to catch up, with 14% planning to invest within a year.

Women Investing in Blockchain-Enabled Assets, by Country

6. Do you invest in sustainable or diverse assets, such as ESG, socially responsible investing (SRI), gender equality funds, or others?

Young women are leading the ESG investing charge.

More than four in 10 US women aged 18 to 29 either invest in ESG-type assets or plan to within the next year. That’s almost triple the percentage among those over 60. Once again, the pandemic changed a lot for this young age group: Of the 26% of respondents in this category who invest in ESG, well over half of them started after March 2020.

The activity and intent around sustainability and diversity in investing is clearly influenced by age: The propensity to invest or intent to invest drop for older groups. Frankly, it’s a little shocking that only 10% of US women over 60 are investing in any ESG-type assets. Perhaps younger women should be educating their mothers and grandmothers?

US Women Investing in ESG Assets, by Age Group

Money doesn’t matter much when it comes to ESG investing.

There’s little clear income effect on this behavior, except around the intention to invest: The two lower income brackets — and probably younger respondents, on average — are roughly twice as likely to say they plan to start in the next year. As far as who is actually investing in ESG, no group departs meaningfully, either higher or lower, from the US national average of 16%.

US Women Investing in ESG Assets, by Household Income

We’re all on the same planet, aren’t we?

It’s a little hard to tell that by the chart below. The Danes are most committed to ESG-type investing: A whopping 31% of Danish women say they are currently investing this way, compared to the 19% global average. But that’s not all that jumps out: As with blockchain-enabled assets, US and UK women are lagging the trend. The pandemic may have helped move the needle on this, with 13% to 21% of respondents either starting to invest or investing more in ESG and ESG-related securities.

Finally, the Singapore results are interesting. In a study Barbara conducted in 2018, some of the global leaders from the region she interviewed said that people there were not interested in ESG-style investing: “All we care about is making money!” they said. We wonder if the 24% of Singaporean women who intend to start ESG investing means that mode of thinking has changed. Or have they realized that ESG investing can be just as profitable?

Women Investing in ESG Assets, by Country

For more on this topic, read the full report “Women and Finance: The 2022 Rich Thinking Quantitative Survey Findings” report by Barbara Stewart, CFA, and Duncan Stewart CFA.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Prasit photo

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.