Cryptocurrencies and the blockchain represent a major technological shift in the world of finance, enabling high-speed transactions between accounts anywhere in the world, potentially reducing transaction costs and democratising the global financial system.

As a relatively recent technology, many authorities and large sections of the public have been unsure of what to make of cryptocurrencies. However, as they gradually become more commonplace and better understood, greater numbers of people have started investing in crypto and even using it to purchase goods and services where possible.

With more ways to get started with cryptocurrency than ever before, it is very important for new investors to do their research and find the best crypto brokers to suit their needs. In fact, even factors such as where you are based in the country could have an impact on how accessible or easy it could be for you to get into crypto.

Each state in the US is able to make its own laws relating to the regulation of cryptocurrency, and factors such as accessibility and ease of use can vary wildly from state to state. With this in mind, we at Invezz have created a study that reveals which parts of the United States are the most ready for crypto adoption.

The US states most ready for crypto

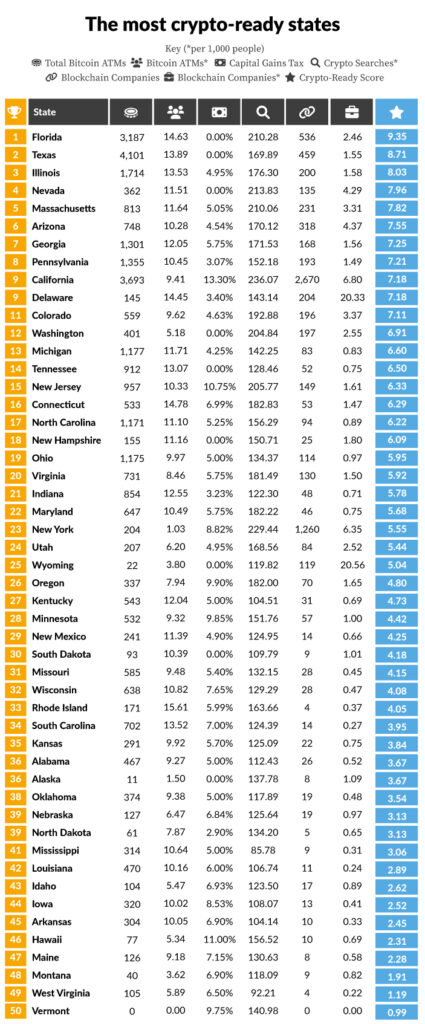

Having looked at numerous factors relating to each state’s preparedness for accepting crypto as a standard form of payment, we have been able to combine them into a single score that represents their overall crypto-readiness. Here we can see which states are most ready to adopt the use of cryptocurrencies.

1. Florida: Crypto-ready score: 9.35

Florida is the state that is most prepared for crypto adoption, with a crypto-ready score of 9.35/10. The sunshine state is well-known for its active engagement with the burgeoning crypto-economy, with Miami being regarded as a crypto capital. Miami’s mayor, Francis Suarez, is a firm believer in the future of crypto and is even paid his city salary in Bitcoin, while the city’s major sporting arena now bears the name of crypto exchange, FTX.

Miami has one of the highest numbers of Bitcoin ATMs per person with 14.63 per 100,000 people, as well as one of the highest rates of public interest in crypto with 210.28 Google searches for crypto topics per 1,000 people. Florida also has no Capital Gains Tax, so profits made from crypto investments are tax-free.

2. Texas: Crypto-ready score: 8.71

Texas takes second place for crypto preparedness with a crypto-ready score of 8.71. This is another state with no Capital Gains Tax, making it fertile ground for crypto enthusiasts, while also benefiting from having 13.89 Bitcoin ATMs per 100,000 people and high levels of public and business interest in the sector.

3. Illinois: Crypto-ready score: 8.03

Illinois is the third most crypto-ready state with an overall score of 8.03. The high number of Bitcoin ATMs in the state, paired with a growing number of blockchain businesses, shows that Illinois is making great strides towards making cryptocurrency a viable alternative to fiat currencies in the state. In fact, the Blockchain Technology Act, which came into effect at the start of 2020 and provides a statewide framework for the use of blockchain technology, shows just how far crypto acceptance has come in Illinois.

The US states least prepared to adopt crypto

While attitudes towards cryptocurrencies in many states are positive, with many blockchain companies sprouting up and a strong public interest in digital currencies, not all states are as prepared to welcome the era of paying for goods and services with crypto. Here we can see which states are the least ready to incorporate crypto into their daily lives.

1. Vermont: Crypto-ready score: 0.99

Vermont has the lowest crypto-ready score of just 0.99, making it the worst place in the country for the adoption of cryptocurrency. There are currently no Bitcoin ATMs at all in Vermont, as well as no blockchain startups, making the state one of the most crypto-free zones in America. This lack of crypto activity could be largely attributed to lawmakers’ attitudes towards decentralised finance, as the state has gone so far as to make it illegal to engage in the business of buying or selling cryptocurrency without a license. Despite this, there appears to be much more public interest in crypto in Vermont than in West Virginia, as there were 140.98 crypto searches per 1,000 people in the last year.

2. West Virginia: Crypto-ready score: 1.19

West Virginia is the second least prepared state for crypto adoption, with a crypto-ready score of just 1.19. The state has few Bitcoin ATMs relative to its size with just 5.89 per 100,000 people, barely any blockchain-related companies at just 0.22 per 100,000 people, and the lowest number of crypto Google searches at 92.21 per 1,000. The state also has a Capital Gains Tax rate of 6.5%, meaning that profits made from crypto investments will be lower than in many other states.

3. Montana: Crypto-ready score: 1.91

The third least prepared state for the adoption of cryptocurrency is Montana, which received an overall crypto-ready score of 1.91. Montana has a very low rate of public interest in cryptocurrency with just 118.09 searches per 100,000 people, while also having very low accessibility of Bitcoin ATMs. However, the state has proven to be a popular destination for crypto mining operations due to the abundant space and cool climate, which could give new meaning to Montana’s nickname “The Treasure State”.

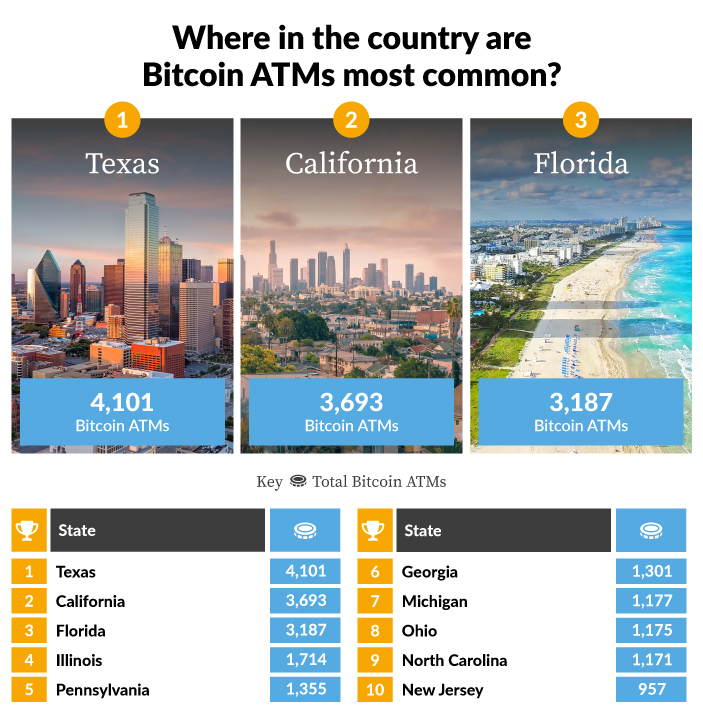

Crypto accessibility: Where in the country are Bitcoin ATMs most common?

The prevalence of Bitcoin ATMs in a state is a good indicator of how easy it would be for people to access their cryptocurrencies and use them in their day-to-day lives. They also represent a willingness on the part of residents to engage with cryptocurrencies, rather than shying away from the new technology. Here we can see which states have the most Bitcoin ATMs, as well as looking at the number of Bitcoin ATMs per 100,000 people and per 1,000 square miles.

The states with the most Bitcoin ATMs

| Rank | State | Bitcoin ATMs |

|---|---|---|

| 1 | Texas | 4,101 |

| 2 | California | 3,693 |

| 3 | Florida | 3,187 |

| 4 | Illinois | 1,714 |

| 5 | Pennsylvania | 1,355 |

| 6 | Georgia | 1,301 |

| 7 | Michigan | 1,177 |

| 8 | Ohio | 1,175 |

| 9 | North Carolina | 1,171 |

| 10 | New Jersey | 957 |

1. Texas: Bitcoin ATMs: 4,101

Texas is the state which has the most Bitcoin ATMs, with as many as 4,101 ATMs available for public use. This indicates that Texans have excellent access to their cryptocurrency should they choose to use it in their day-to-day lives.

2. California: Bitcoin ATMs: 3,693

California has the second most Bitcoin ATMs in the country with 3,693. A traditionally forward-thinking state, with several large cities such as Los Angeles, San Diego and San Francisco, it’s no surprise that Bitcoin ATMs have become so prevalent.

3. Florida: Bitcoin ATMs: 3,187

Florida has the third most Bitcoin ATMs with 3,187 spread across the Sunshine State. The bulk of these are in and around the Miami area, which is a hub of crypto activity and support.

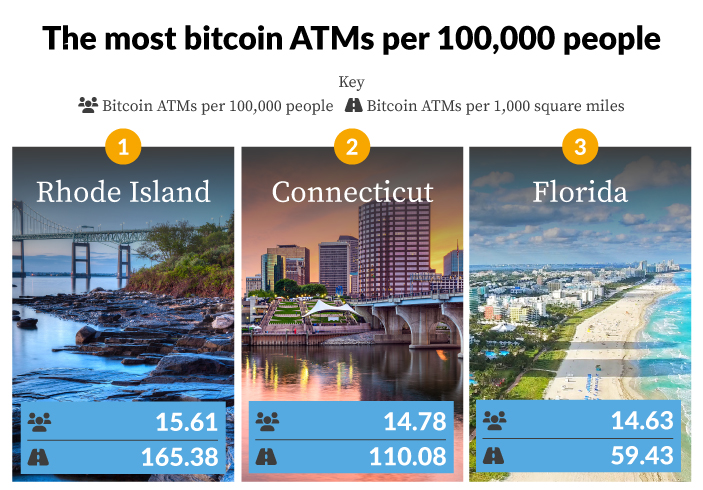

The most Bitcoin ATMs per 100,000 people

1. Rhode Island: Bitcoin ATMs per 100,000 people: 15.61

Bitcoin ATMs per 1,000 square miles: 165.38

Rhode Island is the state with the most Bitcoin ATMs for its size, both in terms of its population and its geographical landmass, which is the smallest in the country at just 1,034 square miles. This small East Coast state has 15.61 Bitcoin ATMs per 100,000 people, and 165.38 per 1,000 square miles, making it the easiest place in the country for residents to find a Bitcoin ATM.

2. Connecticut: Bitcoin ATMs per 100,000 people: 14.78

Bitcoin ATMs per 1,000 square miles: 110.08

Connecticut has the second highest number of Bitcoin ATMs per 100,000 people at 14.78, while it has the third highest number per 1,000 square miles at 110.08. The high number of Bitcoin ATMs in the state makes using and accessing Bitcoin much simpler in the Constitution State than in most parts of the country.

3. Florida: Bitcoin ATMs per 100,000 people: 14.63

Bitcoin ATMs per 1,000 square miles: 59.43

Florida has the third most Bitcoin ATMs compared to its population, with 14.63 per 100,000 people. However, Florida ranks seventh for the number of Bitcoin ATMs compared to its overall landmass, with 59.43 per 1,000 square miles. This means that while there is a relatively high number of Bitcoin ATMs per person, their accessibility may be much more dependent on whereabouts in the state you live.

Crypto business: The states with the most crypto and blockchain startups

Ever since Bitcoin and the blockchain first emerged as an alternative method of conducting financial transactions, there has been a growing number of startups that specialise in developing this technology and incorporating crypto into our daily lives. The number of crypto and blockchain businesses in each state is a good indicator of how engaged the business sector is in the crypto economy in each state, potentially making it a hotspot for cryptocurrency adoption.

The states with the most blockchain startups

| Rank | State | Blockchain companies |

|---|---|---|

| 1 | California | 2670 |

| 2 | New York | 1260 |

| 3 | Florida | 536 |

| 4 | Texas | 459 |

| 5 | Arizona | 318 |

| 6 | Massachusetts | 231 |

| 7 | Delaware | 204 |

| 8 | Illinois | 200 |

| 9 | Washington | 197 |

| 10 | Colorado | 196 |

1. California: Blockchain companies: 2,670

California has the most blockchain companies, with 2,670 calling the state home. Home to Silicon Valley and many Big Tech corporations, California is a well-developed tech hub the obvious choice for many startups.

2. New York: Blockchain companies: 1,260

New York has the second most blockchain companies in the country with 1,260 being based in the state. Home to the vibrant and bustling New York city, the state is able to attract talent from all over the world to work in the burgeoning crypto sector.

3. Florida: Blockchain companies: 536

Florida has the third most blockchain companies choosing to make the state their home at 536. Florida is often referred to as a crypto hub, with Miami acting as the focal point for crypto activity in the state.

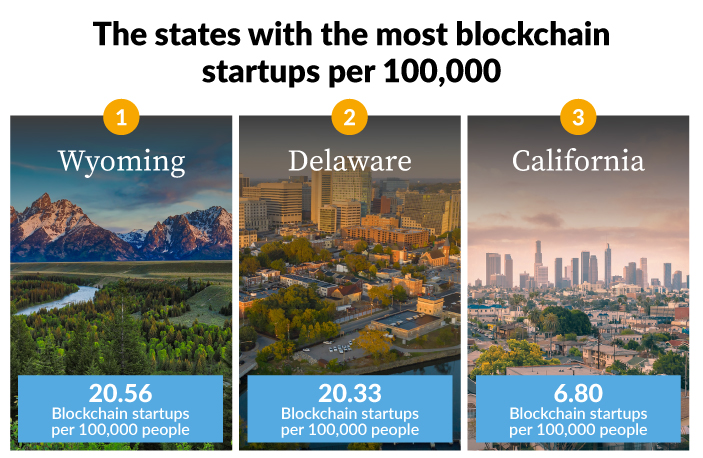

The states with the most blockchain startups per 100,000

1. Wyoming: Blockchain startups per 100,000 people: 20.56

Wyoming has the most blockchain startups in the country compared to its population, with 20.56 per 100,000 people in the state. Wyoming has become a hotspot for blockchain and cryptocurrency businesses due to the state adjusting financial rules to promote the crypto sector in an attempt to diversify the state economy away from a reliance on traditional industries such as coal, oil and gas.

2. Delaware: Blockchain startups per 100,000 people: 20.33

Delaware has the second most blockchain startups per 100,000 people at 20.33, which is just a fraction less than first-place Wyoming. With approximately two thirds (67.8%) of Fortune 500 companies being incorporated in Delaware, it is the traditional choice for many companies to call home. However, as the state has not made blockchain businesses its speciality, who knows how long it can retain a strong foothold in the crypto sector.

3. California: Blockchain startups per 100,000 people: 6.80

California has the third highest number of blockchain startups compared to its population, with 6.80 for every 100,000 people. California has long been a leader when it comes to tech businesses, being home to the famous Silicon Valley, which makes it a natural choice for blockchain startups. There is, however, a significant gap between California and our top two states in this category, which could be explained in part by California’s huge population watering down the numbers.

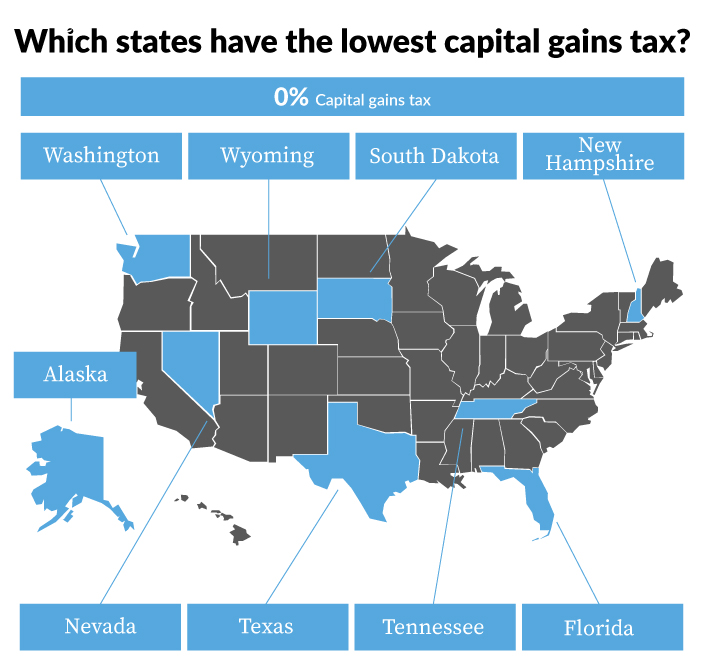

Crypto taxes: Which states have the lowest capital gains tax?

In the United States, cryptocurrencies are subject to Capital Gains Tax (CGT) on any profits made from investments. While there is a Federal Capital Gains Tax rate that all American citizens are subject to, individual states can apply their own CGT on top of this.

Therefore, states with lower or no state-level CGT at all are ideal locations for the proliferation and popularisation of crypto, making it easier and more profitable for residents to engage with the crypto economy. Here we can see which states have the lowest rates of CGT in the country.

1. Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, Wyoming

Capital Gains Tax: 0%

A total of nine states in the US have zero Capital Gains Tax, making them great places for people to invest in cryptocurrencies as they will be able to keep hold of any profits they make after paying the Federal rate of CGT. These states are Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington and Wyoming.

Crypto interest: Which states are most interested in cryptocurrencies?

The general public’s interest in cryptocurrencies and blockchain technology is another determining factor in how ready a state is to adopt crypto as a standard form of payment. By assessing the number of searches for crypto-related terms in each state, we can build a clearer picture of the level of interest that crypto has garnered across the country.

1. California: Crypto searches per 1,000 people: 236.07

California is the state with the biggest public interest in cryptocurrencies and blockchain technology, with the highest rate of crypto-related searches at 236.07 per 1,000 people. Always at the forefront of popular trends and new technologies, California is something of a trendsetter, so it’s no surprise that public interest in crypto is so high in the state.

2. New York: Crypto searches per 1,000 people: 229.44

New York has the second highest rate of public interest in cryptocurrency with 229.44 searches per 1,000 people in the state. The Big Apple is possibly the biggest melting pot of cultures and ideas in the United States, which could explain the high level of interest in this cutting-edge technology within the state as a whole.

3. Nevada: Crypto searches per 1,000 people: 213.83

The state with the third most public interest in crypto is Nevada, where there were 213.83 searches per 1,000 people, and is closely followed by Florida and Massachusetts where the rate of crypto searches was just over 210 per 1,000 people in both states.

Crypto legislation in the United States

Legislation surrounding the adoption, use, and tax of cryptocurrencies is important to consider when discussing how well-prepared a state is to adopt crypto. Laws can be put in place for many different reasons, such as to make it easier for crypto-businesses to start up.

However, laws relating to cryptocurrency are not always there to make crypto easier to adopt, as restrictions can be placed on their usage and taxes can be raised to disincentivise their adoption. For instance, New York state implemented a law whereby any business dealing with cryptocurrency must apply for a BitLicense, which comes with dense compliance requirements and a fee of $5,000.

States with the most crypto legislation

Despite some states choosing to support crypto-adoption, while others choosing to hinder it, the number of laws passed relating to crypto in each state can reveal where lawmakers are most engaged with the digital finance revolution. This engagement shows just how disruptive cryptocurrencies have been to the traditional financial markets.

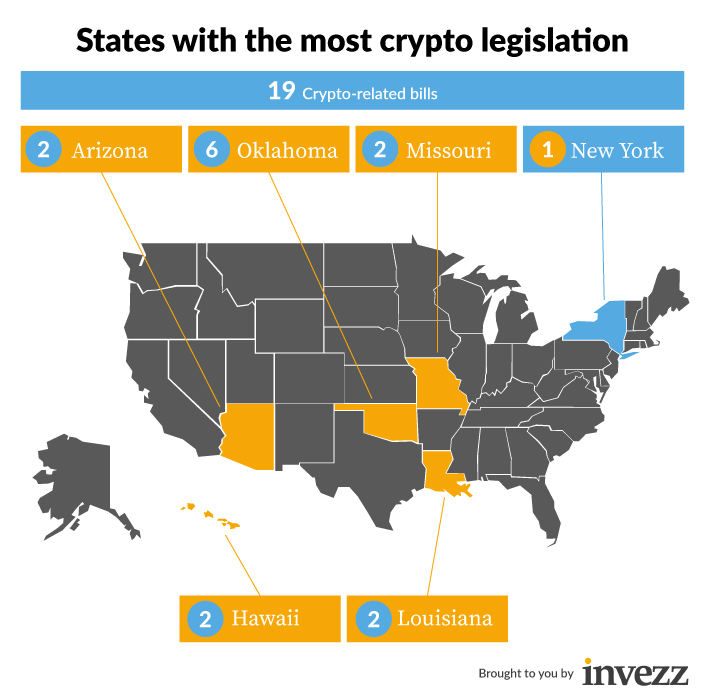

1. New York: Crypto-related bills: 19

New York has the highest number of crypto-related bills introduced by lawmakers at 19, which is more than twice the amount of any other state. In fact, the next highest number of bills is eight, on which Arizona, Hawaii, Louisiana and Missouri are all tied for second place.

There are also many states where there has been no legislation introduced that refers to cryptocurrency, meaning that crypto in these parts of the country is largely unregulated and treated like any other asset. The nine states with no specific crypto-related laws are Arkansas, Delaware, Kansas, Maine, Maryland, New Mexico, Oregon, South Carolina and Wisconsin.

Explore the full US Crypto Report

Having explored some of the key points in our US crypto report, you can explore the full results for all 50 states below.

Methodology

We wanted to investigate how prepared for crypto different parts of the United States are. We used data from Coin ATM Radar to find the number of Bitcoin ATMs in every state and used population data from the U.S. Census Bureau to calculate the number of ATMs per 100,000 people. We then took land mass data from World Population Review to calculate the number of Bitcoin ATMs per 1,000 miles.

Capital Gains Tax rates for each state were also taken from World Population Review, while the number of blockchain companies per state was taken from Tracxn, which was then worked out as a rate per 100,000 people.

Google search data was then acquired for a list of eighteen crypto-related terms for each state, with the number of searches being calculated per 1,000 people. This data, along with the number of Bitcoin ATMs per 100,000 people, the Capital Gains Tax rates, and the number of blockchain companies per 100,000 people were all combined into a single “Crypto-Ready score” which assigned each state a score between 0 and 10, reflecting how prepared they are for crypto adoption.

In addition to this, we also collected data from the National Conference of State Legislatures showing the number of crypto-related bills introduced in each state. While this data was not used to formulate the overall Crypto-Ready score, it did give context to the wider crypto landscape in the United States.

Commentary regarding the adjustment of laws in Wyoming to make it a better place for crypto businesses to prosper was informed by information from Reuters, while information regarding specific crypto regulation in New York state was taken from Crowell and Moring LLP.

[ad_2]

Image and article originally from invezz.com. Read the original article here.