[ad_1]

Introduction

Digital assets form a new and distinct asset class that despite considerable volatility is rapidly maturing. Bitcoin, the first and largest cryptoasset, laid the foundation for enormous innovation across decentralized finance (DeFi), the metaverse, and various other crypto sectors.

To analyze this nascent asset class, we apply the lens of traditional finance, or what some in the crypto space call “TradFi.” By combining this framework — informed by decades of experience in equities, bonds, hedge funds, and capital markets — with a deep understanding of token technologies and structures, we hope to identify attractive opportunities.

Here we’ll walk through three approaches to crypto analysis: sector classification, valuation methodologies, and risk management techniques.

1. Organize Crypto into Sectors

According to CoinMarketCap, there are 9,749 liquid tokens as of this writing. That’s quite a large universe. To capture the breadth, depth, and evolution of equity market sectors, MSCI and S&P Dow Jones Indices developed the Global Industry Classification Standard (GICS). Digital asset markets have yet to coalesce around a GICS equivalent.

CoinDesk and Wilshire, among other players, are developing what may become industry standard crypto sector classifications, and we have constructed our own proprietary framework. Let us explain.

There is a common misconception that every liquid token is a “cryptocurrency” and thus a competitor to bitcoin. While that might once have been the case, the crypto space has expanded beyond just digital currency. We have identified six investable crypto sectors:

- Currencies are digital forms of money used for peer-to-peer (P2P) transactions without the need for a trusted third party.

- Protocols are assets native to “smart contract”-enabled blockchains.

- Decentralized Finance (DeFi) applications are built on smart contract platforms that perform P2P transactions without a bank or other trusted third party.

- Utilities are used in the service and infrastructure networks that are constructing the middleware layer of blockchain economies.

- Gaming/Metaverse applications are built on smart contract platforms that are disrupting the entertainment sector, including gaming, metaverse, social networking, and fan-related applications.

- Stablecoins have values pegged to other assets, most commonly the US dollar.

These sectors each have subsectors within them. For example, DeFi can be further broken down into decentralized exchanges, borrowing and lending, yield aggregators, insurance, liquid staking, on-chain asset management, and more. Stablecoins are fiat-backed, crypto-backed, and algorithmic.

Why use a sector approach to cryptoassets? First, sector diversification can bring value to long-only crypto investing strategies. Market capitalization in crypto markets is concentrated in Currencies and Protocols. (As of 30 March 2022, 58% and 38% of the top 100 digital assets were either Currencies or Protocols, respectively, though Stablecoins, centralized exchange tokens, and certain other assets were not included in this analysis.) Indeed, many major digital asset indices have little exposure beyond these two sectors. For example, as of 31 March 2022, the Bloomberg Galaxy Crypto Index had no exposure to the Gaming/Metaverse sector and less than 2% each to DeFi and Utilities.

But exposure to some of the smaller, more “up-and-coming,” sectors can be worthwhile. The following table shows that sector correlations in 2021 ran as low as 55%, with Gaming/Metaverse exhibiting the lowest relative to other sectors. (Correlations in 2022 are higher amid a crypto bear market.)

Crypto Sector Correlations, 31 Dec. 2020 to 31 Dec. 2021

Runa’s sectors are market capitalization weighted and rebalanced daily.

Sources: Messari and CoinMarketCap

This sector approach brings several benefits. First, as the crypto space matures and is driven more by fundamentals than narratives, and as investors better understand the differences among the various sectors, these correlations should decline.

Second, cross-sectional analysis across different projects within the same sector yields more “apples-to-apples” comparisons. For example, the same fundamental metrics can be deployed to evaluate DeFi exchanges like Uniswap and Sushiswap. But they may not work as well for Utilities like the distributed file storage networks Arweave and Filecoin. The economic sensitivities and the drivers of risk, revenues, and customer demand just vary too much between crypto sectors. Indeed, the preferred tools an equity analyst deploys to value financial companies like JP Morgan or Goldman Sachs are not likely to work as well for automobile manufacturers like General Motors and Ford.

Of course, unlike equity markets, digital assets are novel, immature, and evolving quickly. After all, DeFi wasn’t much of a sector until the DeFi Summer of 2020, and the Gaming/Metaverse sector became much more important with the rising popularity of non-fungible tokens (NFTs). Digital asset sectors are not something that investors and analysts can “set and forget.” As new sectors emerge, sector frameworks need to adapt with the asset class.

2. Identify Value in Crypto

There is meaningful turnover in the top ranks of digital assets. Additionally, there is real “go-to-zero” risk. Projects can and do fail, sometimes with a bang but often with a whimper, fading in value over time. For example, of the top 300 crypto assets by market cap at year-end 2016, only 25 remained in the top 300 five years later, according to CoinGecko.

So, how can we identify those tokens that will stand the test of time? In equity markets, the Gordon Growth Model, a variant of the dividend discount model, is a textbook valuation method that determines a stock’s price based on the company’s future dividend growth.

Gordon Growth Model

P = D1/(r – g)

Where

P = Current Stock Price

D1 = Value of Next Dividend

r = Rate of Return

g = Dividend Growth Expected in Perpetuity

By rearranging the formula and solving for r, the rate of return, we get:

r = D1/P + g

The first term in the formula is current dividend yield, and the second is growth potential. We can adapt the concept behind this model to evaluate a crypto token’s value: The current dividend yield is the economics of the project today, and growth represents the project’s potential. We can quantify the former by using traditional asset valuation principles and techniques. The latter term is more intangible, but there are two ways to think about it: optionality and network effects.

Runa’s Token Valuation Framework

Value of a Token Today = Value of Its Existing Business + Value of Its Potential

Let’s apply this framework to value a digital asset from our Utilities sector. The Ethereum Name Service (ENS) is a domain name registry protocol built on top of the Ethereum blockchain. It allows anyone to register a domain, such as alex.eth, that has various use cases, such as a human-readable wallet address, decentralized website, and email address, among others.

The first term in the framework is the value of the protocol’s existing business. To calculate this for ENS, we use two methods: discounted cash flow (DCF) modeling and price multiples.

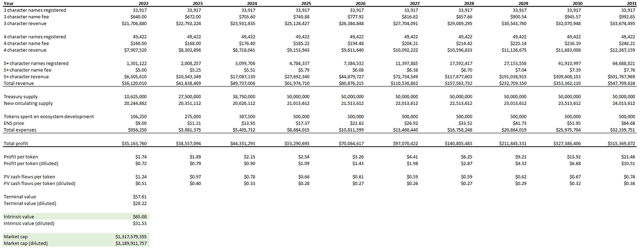

The DCF model simply adds up the present value of the company’s future cash flows and works well with certain revenue-generating digital assets. ENS charges an annual fee to register domains. This is our proxy for ENS’s revenues. By applying growth expectations to the number of domains registered for the next 10 years — based either on historical trends for Web2 email addresses or the expected growth rate from total registrations today — we can calculate expected ENS revenue by year. We can also factor in the costs of further developing the ENS protocol, which is financed through grants from the ENS treasury. These are ENS’s expenses. Revenues minus expenses equals ENS’s expected profit in each of the next 10 years as well as a terminal value — all of which we can discount back to the present to come up with a fair value estimate of ENS, both its fully diluted market capitalization and token price.

Ethereum Name Service DCF Model: Screenshot

For a copy or more information you can reach out to us via email.

So, what about price multiples? How can they inform our ENS valuation? Price-to-sales and price-to-equity ratios help analysts determine whether a stock is over- or undervalued relative to its peers. Similar metrics can work for crypto.

Since the ENS protocol generates revenue, we can compare its price-to-sales multiples with those of other protocols through the website Token Terminal. In other cases, the multiple’s denominator may be more crypto-specific. Tokens within the Protocol sector have a Total Value Locked (TVL) metric, for example, that values all the assets held in the protocol in US dollars or the protocol’s native coin. TVLs and price-to-TVL multiples for various protocols are available on DefiLlama.

The project’s potential value is the second term in our framework. Digital asset valuations today are determined by what the future could hold for each protocol. As such, they are call options on innovation and are rather difficult to value. But considering optionality and network effects can yield insight.

Optionality

What role does optionality play? Imagine valuing Amazon in the late 1990s when it was an online book retailer. We could have built a DCF model estimating future book sales and discounting those cash flows back to the present to come up with a valuation. But that would have completely missed Amazon’s true potential. It wouldn’t have anticipated the company’s eventual dominance of online retail or its entry into cloud computing, the streaming wars, etc.

Ethereum offers similar lessons. The first blockchain to enable smart contracts, Ethereum has rapidly evolved since its 2015 launch. Now, Ethereum has DeFi applications — exchanges, lenders, and insurance providers — built on top of it as well as NFT-related apps such as marketplaces, games, and metaverses. These developments could hardly have been predicted at Ethereum’s initial release.

The principal use case of ENS domain names today is to make Web3 wallet addresses human-readable. But they could also be used for decentralized websites and email addresses, or to provide on-chain identity. Two promises of Web3 are personal data ownership and interoperability. The ability to own our online identities and control our data is extremely powerful — and valuable. What if we could carry that data around the web in a “digital backpack”? That would give us more control and make applications vying for our business more competitive. Imagine being able to move our social media data from one Web2 platform to another, say Twitter to Instagram. Our online identities are not entirely portable today: We need to build them more or less from scratch on each platform. But our ENS domain name could store all that information for us and allow us to share it and transport it how we like. These considerations suggest that ENS’s potential value may be more than its price multiples indicate.

Network Value

Network value is another way to think about a crypto project’s potential. The success of Web3 projects hinges on network effects. The concept is simple: The more users in a network, the more valuable the network. Web2 companies leveraged network effects too, but the benefits tended to accrue to the companies themselves. Web3 value creation is primarily retained by participants: the miners, validators, governance providers, customers, and other token-specific roles.

The engineer and entrepreneur Robert Metcalfe formulated what came to be known as Metcalfe’s law to quantitatively describe network effects. We believe it explains much of the stock price movement of Web2 leaders like Meta as well as digital asset leaders like bitcoin.

Adoption and user growth are among the key fundamental indicators we track for existing and prospective investments. As digital assets are increasingly adopted, their network effects are growing.

To be sure, optionality and network effect considerations may not deliver a perfect valuation to base our trades, but analyzing investments from these angles can help us triangulate toward what a potential long-term fair value might be.

3. Manage Portfolio Risks

Constructing digital asset portfolios is not much different from building stock portfolios. How the assets and their weightings influence each other and constitute a whole portfolio are key considerations. Though diversified across several assets, there could be shared risks. Knowing what those risks are and whether they are acceptable is critical, especially for a volatile asset class like crypto. Here are three TradFi investment risk management techniques that can help assess digital assets.

Correlations are one of the primary building blocks of portfolio construction. They describe the relationships among all portfolio assets and whether there is potential exposure to a single sector, ecosystem, or theme.

Risk factor models can also help quantify a portfolio’s elemental risk drivers. In equity markets, the capital asset pricing model (CAPM) includes a single factor — the market — to explain a particular stock’s systematic vs. idiosyncratic risk. The latter can be diversified away, the former cannot.

Can a similar model be applied to digital assets? We found compelling evidence for a shared risk factor in digital assets that might form the foundation of a digital asset-specific risk model as well as the core of a digital asset portfolio allocation, similar to equity beta’s role in equity risk models and portfolio allocations.

We have expanded that initial factor model research to include two macro factors — equities and inflation — in addition to a crypto market factor. This three-factor model can determine which factors — macro or crypto-specific — are responsible for portfolio risk. Why is this important? Because crypto markets periodically become entangled with macro markets, and this model measures and monitors that shared exposure over time.

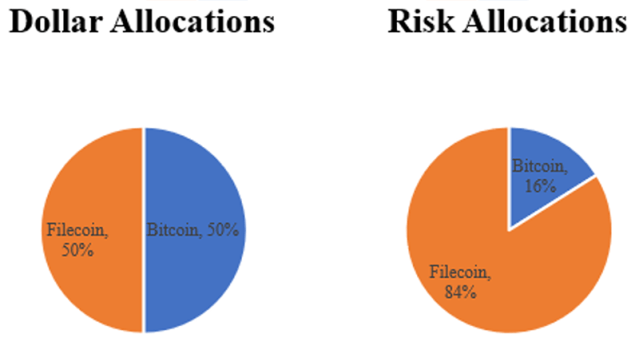

Finally, we tend to think of a token’s portfolio weight in dollar terms. In the classic 60/40 portfolio, 60% of the dollars are held in stocks and the rest in bonds. But given their higher volatility, stocks account for much more than 60% of portfolio risk. It is probably closer to 90%.

Digital assets’ risk profiles have enormous variation. Bitcoin has the least volatility, with an annualized rate in the 70% to 90% range. Other tokens, even some in the top 100 by market cap, have exhibited annualized volatilities in excess of 200%. Imagine we allocate half our dollars to low-volatility assets like bitcoin and the rest to higher risk tokens like Filecoin. The risk allocation is not even close to 50/50.

Bitcoin-Filecoin Portfolio: Dollar vs. Risk Allocation

Source: Messari

Of course, while traditional finance’s risk metrics can help us better understand the risk profile of cryptoassets and our larger portfolio, they do not reveal the full picture. These metrics must be deployed alongside qualitative, token-specific, and crypto-native risks, including smart contract and regulatory risks.

Conclusion

While not all traditional investment management techniques are applicable to digital assets, sector breakdowns, DCF models, and risk factor modeling, among other timeless investment principles, are solid starting points. There is tremendous value in bringing these tools to bear on this emerging asset class. They can help construct digital asset portfolios with the best chance of surviving and thriving over the long-term.

If you liked this post, don’t forget to subscribe to the Enterprising Investor

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images/ D-Keine

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.