[ad_1]

The essence of maximizing the internal rate of return (IRR) lies in the total amount of leverage contracted to finance a transaction. The less equity a buyout firm has to fork out, the better its potential gains.

This mechanical process is shown in the following table using three hypothetical investments. The higher the leverage ratio, the higher the return on equity and the cash-on-cash multiple upon exit:

Table 1: Leverage’s Effect on Private Equity Returns, in US $1,000s

Understandably, private equity (PE) executives wouldn’t think of boosting their performance through other means without first negotiating the largest and cheapest debt package possible. Yet another factor, the time value of money (TVM), takes center stage.

Leverage and TVM: A Powerful Combination

So, why do PE investors operate the way they do? The following exercise will demonstrate the underlying rationale. The tables below delineate the range of returns that a leveraged buyout (LBO) might achieve. There are eight scenarios with three variables:

- Variable 1 is the amount of leverage — the net debt/equity or net debt/total capital — at inception. We use two different scenarios: 60% or 90% debt.

- Variable 2 is the timing of dividend recapitalizations during the life of the buyout. Again, we review two possibilities: achieving recaps in Year 2 and Year 3, or Year 3 and Year 4, while leaving all the other cash flows unchanged.

- Variable 3 is the timing of the exit. We assume a full disposal in Year 5 or Year 6.

All of these scenarios assume that none of the debt is repaid during the life of the transaction. Assuming no repayment makes the scenarios easier to compare.

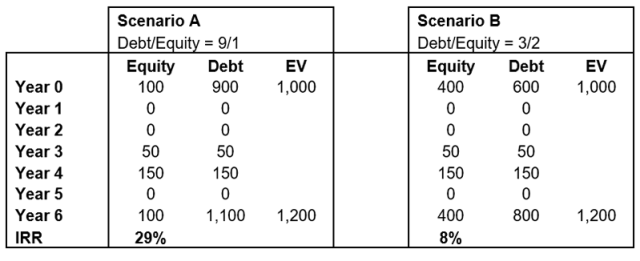

The first scenarios in Table 2 include dividend recaps in Year 3 and Year 4 and an exit by the PE owner in Year 6. Both scenarios have the same entry and exit enterprise values (EVs). These two scenarios only differ in one way: Scenario A is structured with 90% debt, Scenario B with only 60%.

Table 2: Year 6 Exit with Dividend Payouts in Years 3 and Year 4, in US $1,000s

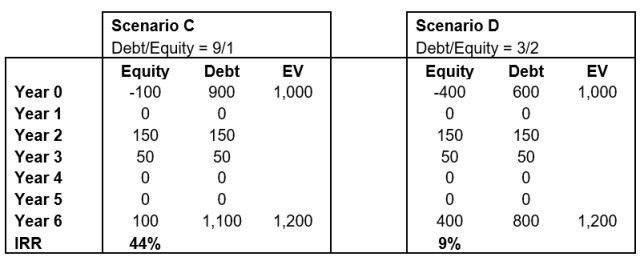

In the next two scenarios, in Table 3, the dividend payouts come in Year 2 and Year 3 and a realization by the buyout firm in Year 6. Again, the only difference in these two scenarios is the leverage: Scenario C uses 90% and Scenario D just 60%.

Table 3: Year 6 Exit with Dividend Payouts in Year 2 and Year 3, in US $1,000s

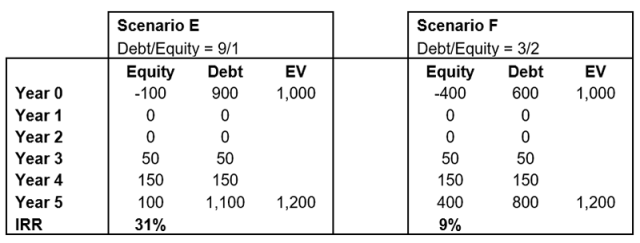

Table 4 shows dividend distributions in Years 3 and Year 4 and a sale by the financial sponsor in Year 5. Again, these two scenarios only differ on the debt: Scenario E is financed with 90% debt and Scenario F with only 60%.

Table 4: Year 5 Exit with Dividend Payouts in Year 3 and Year 4, in US $1,000s

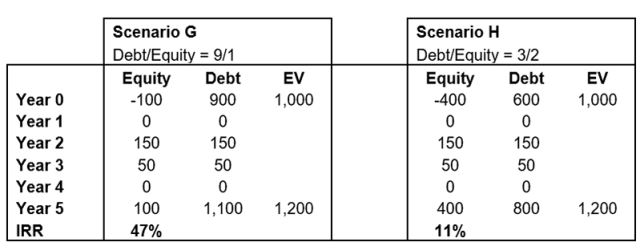

The last set of scenarios in Table 5 looks at dividend recaps in Year 2 and Year 3 and an exit in Year 5. The only difference between them, again, is the amount of leverage.

Table 5: Year 5 Exit with Dividend Payouts in Year 2 and Year 3, in US $1,000s

We can draw several conclusions from these scenarios:

- It is better to leverage the balance sheet as much as possible since –assuming all other parameters remain constant — a capital structure with 90% debt yields significantly higher IRRs for the equity holders than a 60/40 debt-to-equity ratio: Scenario A beats B, C beats D, E beats F, and G beats H.

- Dividend distributions are best performed as early as possible in the life of the LBO. A payout in Year 2 generates higher average annual returns than one in Year 4: Scenario C beats A, D beats B, G beats E, and H beats F.

- The earlier the exit, the greater the profit — if we assume a constant EV between Year 5 and Year 6 and, therefore, no value creation during the extra year — which obviously does not reflect all real-life situations. Still, scenarios with earlier exits generate higher returns than those with later realizations, hence the popularity of “quick flips”: Scenario E beats A, F beats B, G beats C, and H beats D.

Our first point underlines the mechanical effect of leverage shown in Table 1. But there are two other benefits related to debt financing:

- The second benefit relates to taxes. In most countries, debt interest repayments are tax-deductible, while dividend payouts are not. This preferential treatment was introduced in the United States in 1918 as a “temporary” measure to offset an excess profit tax instituted after World War I. The loophole was never closed and has since been adopted by many other jurisdictions.

Borrowing helps a company reduce its tax liability. Instead of paying taxes to governments and seeing these taxes fund infrastructure, public schools, and hospitals, the borrower would rather repay creditors and improve its financial position. The PE fund manager’s sole duty is to their investors, not to other stakeholders, whether that’s society at large or the tax authorities. At least, that’s how financial sponsors see it.

Earlier we referenced the concept of TVM. Despite their protestations to the contrary, PE fund managers prefer to get their money back as soon as possible. Conflicting interests abound between the financial sponsor — for whom an early exit means windfall gains thanks to a higher IRR — and the investee company’s ongoing management and employees who care about the business’s long-term viability.

That said, financial sponsors can easily persuade senior corporate executives — and key employees — by incentivizing them with life-changing equity stakes in the leveraged business.

Leverage’s Role in Value Creation

To keep attracting capital, PE fund managers use many tools to highlight their performance. The value bridges developed by fund managers to demonstrate their capabilities as wealth producers are deeply flawed, as illustrated in Part 1, and only emphasize operational efficiency and strategic improvements in the fund manager’s profitable deals.

That leverage is excluded entirely from value bridges is another major deficiency. As KPMG explained, “The value bridge fails to relate the amount of debt a buyout repays to the size of the initial equity investment in the deal.”

The complexity of determining how LBOs create economic value explains the wide discrepancies in the research on leverage’s contribution to investment performance.

The study “Value Creation in Private Equity” found that “the leverage component in value generation for deals made during the last buyout “boom” (2005-2008) was 29%,” but the impact of leverage was as high as 33% during the pre-boom years.

Other analyses have found that leverage plays a larger role in delivering outperformance. In “Corporate Governance and Value Creation: Evidence from Private Equity,” the authors analyzed the value bridges of 395 PE transactions and found that the leverage effect amounted to almost half of total IRR. Another study, “How Important Is Leverage in Private Equity Returns?” indicated that the use of debt could account for more than half of value creation.

Value creation in PE is impossible to break down, which means managers are free to make grandiose claims about their operational skills. That’s understandable. We’d all rather be known as wealth generators than simply financial engineers. Nevertheless, the debt-fueled enhancement of investment returns is an inescapable trick of the PE trade, as the aforementioned studies demonstrate.

Indeed, Sequoia partner Michael Moritz once observed that the asset class was called leveraged buyouts “before some marketing genius fastened on ‘private equity’ as a way to disguise the fact that the business still rests on a mountain of debt.”

By downplaying leverage’s pivotal role, the value bridge exaggerates a fund manager’s operational skills to help secure commitments from capital providers.

Parts of this article were adapted from The Debt Trap: How Leverage Impacts Private-Equity Performance by Sebastien Canderle.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images/aluxum

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.