[ad_1]

The internal rate of return is dead. Long live the IRR.

“Hey, the IRR looks soooo close to the DaRC!” Michele observed.

Michele is our chief technology officer at XTAL Strategies, and I had never asked him to compute and include private equity’s internal rate of return (IRR) in our lines of code before. I had handled that. Now he was working on our new analytics dashboard, which is usually engineered exclusively on duration-adjusted return on capital (DaRC) algorithms, and noticed the similarities.

He was shocked. He had learned since joining my team that I had developed the DaRC methodology precisely to overcome IRR’s limitations as a metric for private equity performance.

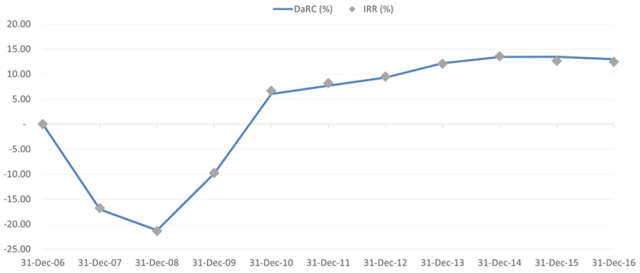

“Why develop the DaRC?” Michele asked. “It is almost identical to the IRR!” He showed me the following chart, which plots the DaRC and IRR over time, for a representative private equity fund.

DaRC vs. IRR

“What’s the point then?” he asked.

The point is that the DaRC is meant to be a more accurate measure that evolves the information set available to investors specifically overcoming the limitations of the IRR.

You can think of it as a “translation tool,” but it indeed is a robust performance calculation methodology that frames the same components of the IRR in the time-weighted context of all other asset classes.

The DaRC methodology, and the concept of duration, adds the critical and absent time framework to the IRR and gives an understanding of:

- The when, on average, the average return from the measured investments that the IRR represents starts to be earned.

- The how long that return is earned for.

Both pieces of information are crucial because performance numbers are useful to investors only if they help them understand how much money they’re making. An IRR of 15%, say, does not mean that investors are making 15 cents for every dollar invested in annualized terms, which is what time-weighted percentages measure.

“Okay, go on,” said Michele.

The fact is IRR figures don’t inform investors about the two points above. In Inside Private Equity, the authors briefly introduce the concept and provide an approximation of the IRR’s net duration — the how long. Others have developed public-market equivalent (PME)-like proxy estimations of the when.

Nevertheless, without precise information about the when and the how long — and, importantly, over which time horizon — the adopted performance metrics won’t give an accurate sense of how much money investors are making (or losing) without any ambiguous approximations.

The DaRC methodology illuminates the IRR’s shortcomings. The IRR does not show that its approximate performance numbers refer to a forward-forward transaction — i.e., the cash in– and outflows happen on average at a later time than the initial subscription of commitment or the closing of the private equity fund.

To fully explain the returns, taking into account the impact of dry powder and of eventual credit and subscription lines, a precise time transfer mechanism with time stamps for the when and the how long is required. The investment horizon may be set ex ante by the interested investor if, for example, it is an expected liability situation that the investment is supposed to match.

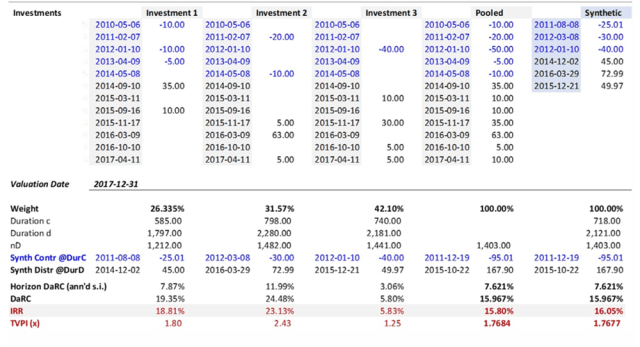

The litmus test of the DaRC methodology’s additivity is visualized in the following table. It shows the individual and average — pooled and synthetic — performance of three investments, which could be portfolio companies or private equity funds. The DaRC, IRR, and TVPI are all calculated for a valuation date set at 31 December 2017.

Three Hypothetical Investments: DaRC, IRR, and TVPI

The top of the table includes inputs for cash flows, dates, and amounts, with negative numbers for contributions in blue, positive figures for the distributions in black. The Pooled case is simply the arithmetic sum of the cash flows of the three prior investments, while the Synthetic case is calculated using the DaRC methodology.

The DaRC methodology uses the Duration mechanism to determine the modeled Synthetic transactions: zero coupon — one bullet contribution, one bullet distribution — like in fixed income. These are equivalent to the stream of cash flows they represent. The bottom of the chart illustrates the details of the Synthetic transactions, dates, and amounts, using the same conventions of the raw data, as well as the output calculations for the DaRC, IRR, and the Horizon DaRC, or the annualized rate of return that investors can expect to earn (and actually receive) over the predetermined time horizon.

The DaRC and IRR are indeed quite similar: They both represent the period return produced during the timespan when the capital is deployed. But just the DaRC carries along the precise timespan “ID card” information.

This ID card makes DaRC and Horizon DaRC two sides of the same coin that can be reconciled at any time — in Pooled and Synthetic form. The Synthetic model represents the Pooled sum through the duration characteristics.

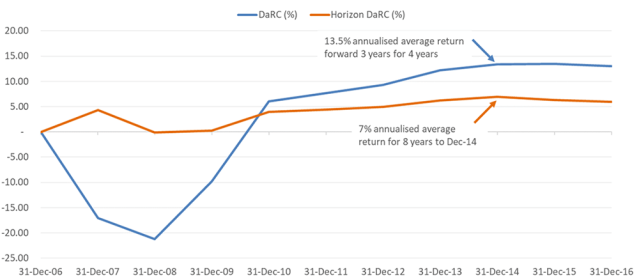

How the DaRC and Horizon DaRC yields of our representative fund move over time is visualized in the chart below. The implicit difference? The DaRC is the rate of return the invested capital produces over time for the net duration — the difference of the durations of Distributions (DurD) and Contributions (DurC) — while the Horizon DaRC is the actual annualized rate of return that investors earn for the predetermined time horizons.

DaRC vs. Horizon DaRC

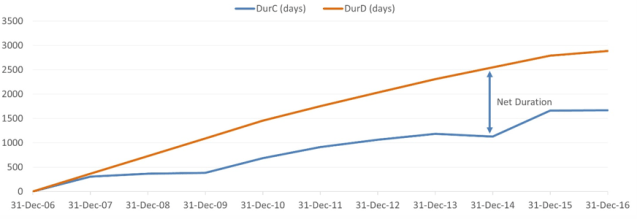

The Horizon DaRC then is a true yield curve where the 7% plot at the end of 2014 shown by the orange arrow is the annualized-since-inception return. It represents the actual total return yield that investors are actually receiving from the investment in the fund. The DaRC line in the chart only shows the return for the net duration as it materializes while the fund matures. Consequently, the 13.5% plot at the end of 2014 shown by the blue arrow is the DaRC recorded with the information available as of that date for the Net Duration of approximately four years (1,422 days), shown in the following table.

DurC vs. DurD

“Okay. This may require some basic math, but I get the substance,” Michele said. “What are the implications?”

It is

impossible to replicate the computations above using IRRs and PMEs. Why?

Because these methodologies lack additivity and time transferability

properties. In fact, the non-homogeneous timeframes and notional references of

cash flows they use in their calculations mean that their averages and rankings

are mathematically incorrect. So IRR quartiles are essentially meaningless.

Moreover, calculations based on IRR, PME, and cash flows of average returns,

risk premia, alpha, and dispersion, among other variables, may have to be

revised in academic studies. And finally, existing private equity indices are

not accurately representing the underlying physical investments.

That’s why DaRC’s duration time stamps are critical for preserving the time-weighted value of money.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Pavel Abramov

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.