[ad_1]

The Bank of Japan (BOJ) widens the 10-year yield trading range.

The BOJ announced its latest yield curve control (YCC) change on 19 December, raising the 10-year yield cap from 25 basis points (bps) to 50 bps. Some interpreted the shift as the first in a forthcoming series of hawkish moves from the BOJ, and the yen rallied from 137.41 to 130.58 before paring gains.

Previously, when Japanese government bond (JGB) yields rose toward the BOJ cap, the yen weakened. But the recent policy shock briefly restored the traditional macro-dynamic: The higher the yields, the stronger the currency in expectation of capital inflows.

Nevertheless, there is reason to be cautious about the nascent yen rally.

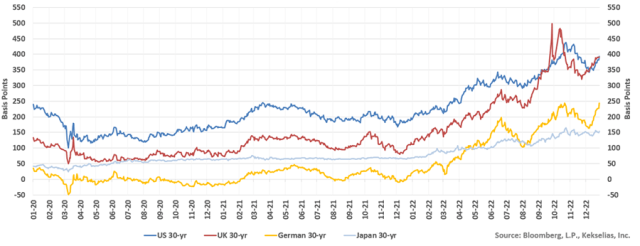

While the market expects the BOJ to loosen YCC further, the bank’s next move in that direction, barring any policy surprises, may still be months away. Amid the yen’s renewed strength, rebounding global long-term interest rates may again exert upward pressure on JGB yields. This is consistent with the framework of co-movements between global long-term sovereign bonds that are “close substitutes,” as outlined by Governor Lael Brainard of the US Federal Reserve.

Co-Movement in Global Long-Term Interest Rates

Should global yields spike, the BOJ may have no choice but to defend its new 50 bps yield cap by creating new cash reserves to buy 10-year JGBs and reestablish curve control. That would come with a cost: The yen would weaken as short USD/JPY momentum unwinds, even if the BOJ shifts further later in the year.

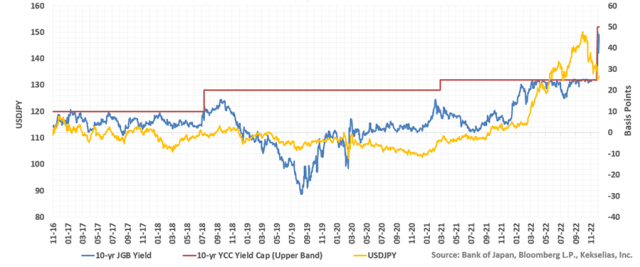

This isn’t the first time the BOJ has revised its 10-year trading band. After the central bank inaugurated quantitative and quality easing (QQE) with YCC in September 2016, it established a precedent with two policy shifts. On 31 July 2018, the Policy Board expanded the 10-year trading range from +/–10 bps to +/–20 bps, and then to +/– 25 bps on 19 March 2021. BOJ intervention weakened the yen when the 10-year JGB yield tested the policy ceiling in 2022. Until YCC ends, there is nothing to keep that from happening again.

Japan 10-Year Yield vs. Yield Curve Control “Ceiling”

Potential Triggers for Renewed BOJ Yield Curve Defense

As the global economy continues to evolve beyond pandemic-related disruptions, revived overseas growth and greater demand for energy commodities, among other factors, may offset the demand destruction dynamics. In the United Kingdom, fiscal stimulus has supplanted fiscal austerity, as the government plans to extend former prime minister Liz Truss’s energy subsidy plan into spring 2024. Japan’s economy is sensitive to global commodity prices, and a price spike could lift domestic inflation expectations and exert upward pressure on the 10-year JGB yield.

Thus, the anticipated timeline of BOJ hawkishness may become decoupled from market developments. If the next BOJ policy shift is expected in the second quarter of 2023, what happens if rising yields test the BOJ’s yield curve defense early in the first quarter? The BOJ may transform the JGB rout into a weaker yen, printing money to finance yield defense at its 50 bps line in the sand.

Conversely, softer-than-expected global growth, a return to fiscal austerity among major economies, easing geopolitical tension, and falling commodity prices could lower the 10-year JGB yield and reduce the likelihood of forceful BOJ interventions. In effect, the yen remains sensitive to the spread between the 10-year JGB and the BOJ policy cap.

In other words, moving the goalposts further down the field doesn’t mean the ball won’t get there. So long as there are goalposts, they will have to be defended, and the BOJ has yet to signal its readiness to abandon yield curve control altogether.

If you liked this post, don’t forget to subscribe to Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images/ Hiro_photo_H

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.