[ad_1]

Have you ever thought about moving to a different state? Maybe one with nicer weather, lower taxes, more responsible government, or better public services?

When you live in Chicago, my hometown, it’s hard not to. While Illinois doesn’t have a monopoly on fiscal mismanagement or rough weather, it has more than its fair share.

As 2020 draws to a close, many tax- and residency-related matters are coming to the fore to which clients may want to pay attention and make conscious decisions about.

The following analysis is meant to help facilitate and inform those discussions. To be sure, changing states is not a simple decision, nor are the nuances of state-by-state tax comparisons, so what follows is meant to raise awareness about some important topics rather than provide any specific investment or tax advice.

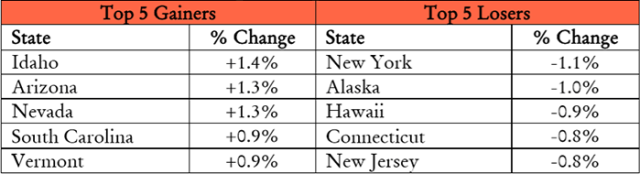

Change in Population by US State, 2018

Why Do People Move?

The US Census Bureau provides extensive data on migration patterns among the US states. We tested whether people move for career prospects, climate, cost of living, or taxes using the following state-by-state proxies for each of the four factors, respectively: median income, average annual temperature, cost of living index, and marginal tax rate.

The top and bottom five states for each of our four relocation factors are listed below:

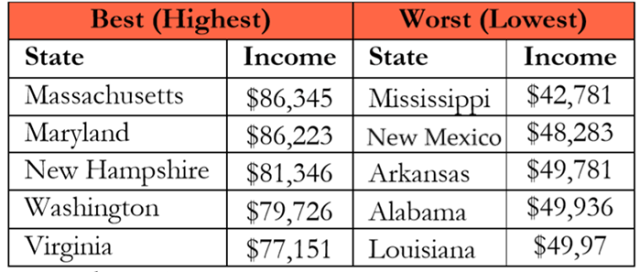

Best and Worst: Median Income by US State, 2018

Best and Worst: Average Annual Temperature, 2020

Best and Worst: Cost of Living Index

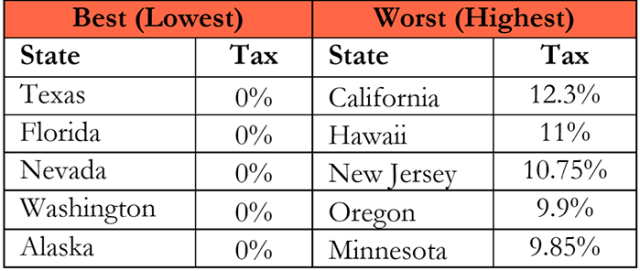

Best and Worst: Marginal Tax Rates*

* Wyoming and South Dakota also have no state income tax.

To understand how the four factors influence relocation decisions, we ran a regression analysis of change in population against each of our variables. We theorized that people are attracted to states with better career prospects and warmer weather and avoid states with higher costs of living and higher tax rates. As such, we expected median income and weather to have a positive correlation with migration gain, while cost of living and taxes would have a negative correlation.

So what did the data reveal? Why are people heading to Idaho and Arizona and leaving New York and Alaska?

Correlations of Migration with Explanatory Factors

| Career Prospects | -0.10 |

| Climate | 0.06 |

| Cost of Living | -0.38 |

| Taxes | -0.23 |

Three of the factors — weather, cost of living, and tax rates — display the correlations we anticipated. The big surprise? Median income has a negative correlation to population migration. People are leaving high-income states. Could the advantages of higher income in Massachusetts and other high-earning states be more than offset by the colder weather and increased taxes and cost of living?

Recent Developments on the Tax Front

The financial shortfalls many states face have been well documented and the COVID-19 pandemic has made them significantly worse. It is hard to see how states will find a way out of this predicament without raising income, property, sales, or estate taxes.

At the national level, the federal government has taken on extraordinary debt in recent years as well and it is reasonable to expect that tax increases will be required to pay it down.

President-elect Joe Biden is due to take office in January with a Democratic majority in the House of Representatives but probably not in the Senate. This should delay the higher taxes that in the long run are likely inevitable even under future Republican administrations.

What sort of tax measures might future administrations and Congress consider? Let’s look at Biden’s proposals.

Income Tax: An increase of the highest marginal tax rate from 37% to 39.6% on income above $400,000.

Tax on capital gains and qualified dividends: An increase in the tax rate from 20% maximum to 39.6% for those earning over $1 million.

Estate tax: Decrease the tax-free transfer limit from about $23 million per couple to possibly about $10 million, or even $7 million.

How to Deal with Taxes

Investors don’t have an abundance of options in the face of high or rising federal income taxes. To be sure, they can look to tax-exempt municipal securities, but tax considerations should guide investment strategy only so much. And with the deteriorating financial conditions of municipalities, such securities may not be as safe as they were in the past. Clients might consider converting traditional IRAs to Roths to lock in today’s lower tax rate and access the Roth’s less onerous mandatory distribution requirements, among other advantages. This strategy makes more sense for those who expect their tax rate in retirement to remain high.

That the capital gains tax rate could almost double for certain clients requires attention. Investors tend to defer capital gains and accelerate the harvesting of capital losses. But if higher taxes loom in the near future, the opposite strategy may make sense for high-income investors. By harvesting long-term capital gains, investors could lock in lower taxes and by postponing loss harvesting, make them more valuable when taxes go up.

Estate taxes are also an urgent matter for clients with large estates. Such clients should take advantage of the liberal limits now in place before they are removed.

Should Taxes Influence Where You Live?

Along with income taxes, some states also levy estate and inheritance taxes, Such taxes come on top of the federal 40% estate tax and can be as high as 20% of the estate. So moving from, say, New York to Florida can not only reduce incomes taxes by 8.8%, but also lower estate taxes by 16%.

Of courses, taxes are hardly the only factor that comes into play in residency decisions. Social networks — family and friends — are critical. As are business and income opportunities, health care, and crime and safety considerations. And of course, the local culture and environment are important factors as well.

Such a diverse set of criteria can be hard to navigate, but while the decision is highly personalized, dividing the factors into three categories — deal breakers, important, and less important — offers a logical framework to consider the options.

Deal breakers are the one or two fundamental requirements that must be met in order for the client to make the move. Think proximity to family or minimal tax burden. Less important factors, on the other hand, can be completely ignored. Once the deal-breaker criteria are met, the decision process becomes something of a give and take among the important considerations. Of course, the reality is the benefits of estate planning do not accrue to the planners so much as the heirs, which is worth keeping in mind while evaluating the trade-offs.

These are highly subjective decisions, and smart, logical people may come to opposite conclusions. For example, one couple might decide that their social and health care networks in New York are worth more than the larger estate a move to Florida would provide. While another would gladly find new health care providers in exchange for warmer weather.

One important consideration: Meeting state residency requirements can be much more complicated than simply staying in a state for a particular number of days. Few high-tax states will give up their high earners and the taxes they contribute without verifying that they have indeed permanently moved to another state. Their tax authorities are highly vigilant and will conduct the audits necessary to determine that their former residents have indeed relocated.

Elvis Presley once sang “Home Is Where the Heart Is.” But for those changing states, it is not as straightforward as that. For them, home is where the tax authority determines it to be!

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Juan Silva

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.