[ad_1]

Introduction

Direct indexing is hot. In October 2020, Morgan Stanley bought the asset manager Eaton Vance primarily for its direct indexing subsidiary Parametric. BlackRock followed one month later by purchasing Aperio, the second-largest player in the space. This year, JPMorgan bought OpenInvest in June, Vanguard took over their partner JustInvest in July, and in September, Franklin Templeton acquired O’Shaughnessy Asset Management (OSAM) and its Canvas direct indexing platform.

The giants of the asset management industry are clearly intrigued by direct indexing and it’s not hard to see why. The rise of exchange-traded funds (ETFs) has steadily eroded the management fees of mutual funds and of ETFs themselves, and with more than 2,000 US ETFs and 5,000 US equity mutual funds all based on a universe of only 3,000 stocks, there is little room left for additional products. The industry is looking for new revenue-generating business areas and growing client interest in customized portfolios has not gone unnoticed.

Direct indexing should be an easy sell for the marketing machines of Wall Street: A portfolio can be fully customized to the client’s preferences by, for example, excluding any stocks that contribute to global warming or prioritizing high-quality domestic champions. On top of that, tax-loss harvesting can be offered. And all of this in a fairly automated fashion using modern technology stacks at low cost.

Like many proposals in investing, direct indexing seems like a free lunch that is too good to pass on. But is it?

An Overview of Direct Indexing

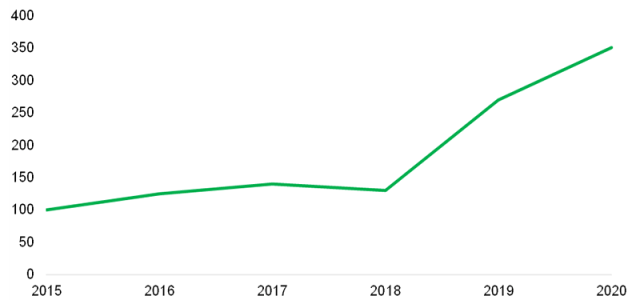

Although firms like Parametric have been offering direct indexing to their clients for decades, the market’s AUM really started to grow since 2015. Over the last five years, direct indexing’s AUM expanded from $100 to $350 billion. In part, this is due to the software-creation technology becoming cheaper and easier to use, which opened the field to new entrants. The surge has also been driven by millennials seeking personalized portfolios, often with a focus on environmental, social, and governance (ESG) considerations.

Assets under Management (AUM) in Direct Indexing, US Billions

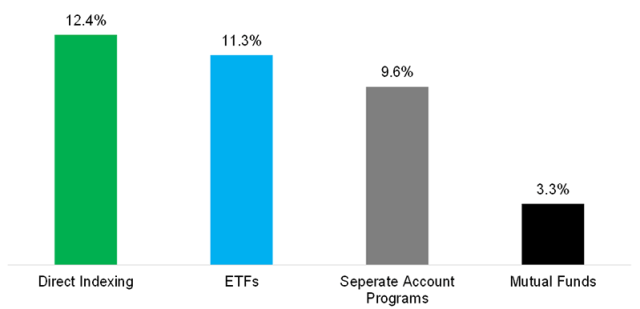

How strong is the momentum in the direct indexing space? A market research study by Cerulli Associates in the first quarter of 2021 anticipated higher AUM growth in direct indexing over the next five years than in ETFs, separate managed accounts (SMAs), and mutual funds.

Of course, a cynic might argue that direct indexing is not much more than an SMA in a modern technology stack. That may be a fair point, but it is a discussion for a different day.

Projected Five-Year AUM Growth Rates by Product, as of Q1 2021

The Dark Side of Direct Indexing

Direct indexing marketing materials emphasize that each client receives a fully customized portfolio. The copy might describe a unique, tailor-made, or bespoke portfolio: the grande, iced, sugar-free, vanilla latte with soy milk from Starbucks versus the traditional coffee from Dunkin’ Donuts.

What’s not to like about being treated like a high-net-worth UBS client? Everyone deserves a personal portfolio!

However, this pitch leaves one thing out. What is actually being sold is pure active management. A client who eliminates or underweights certain stocks they consider undesirable from the universe of a benchmark index like the S&P 500 is doing exactly what every US large-cap fund manager is doing.

But a client who creates their own portfolio based on personal preference, even if a financial adviser manages the direct indexing software, probably won’t be better at stock picking or portfolio construction than a full-time Goldman Sachs or JPMorgan Asset Management fund manager.

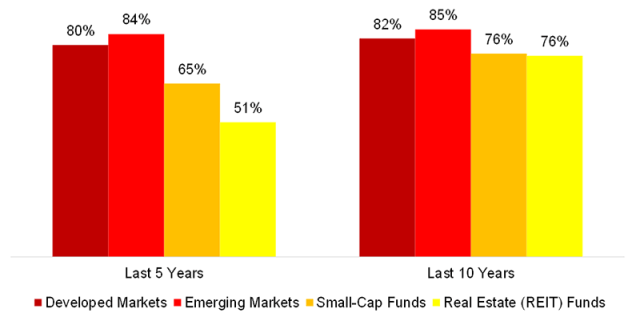

Worse, most professional money managers lag their benchmarks over the short and long term, whether they’re investing in US or emerging markets, small-caps, or niche equity sectors. The fees on direct indexing portfolios tend to be lower than for equity mutual funds, giving them a leg up, but investing based on personal choice is unlikely to outperform already poorly performing fund managers.

So direct indexing clients should not expect to match the market.

Equity Mutual Fund Managers Underperforming Their Benchmarks

The Risks of Tax-Loss Harvesting

While their portfolios may underperform, direct indexing investors still have access to another important feature: tax-loss harvesting.

Here, stocks with losses are sold when capital gains from profitable trades are realized, thus reducing the net tax liability. Practically stocks that were sold can only be bought back 30 days after the sale, which means that an investor needs to buy something else instead.

There are various arguments why the tax benefit is far lower in practice than in theory. Indeed, some maintain that the liability is only deferred rather than reduced.

Regardless, managing an investment portfolio based on tax decisions is wrong in principle and carries significant risks, for example, selling losers at an inopportune time, say during a stock market crash. Typically, the worst-performing stocks rally the most during recoveries. So, if these have been sold off, the investor captures the full downside but only a portion of the upside. Furthermore, replacing losers with other positions changes the portfolio’s risk profile and factor exposure.

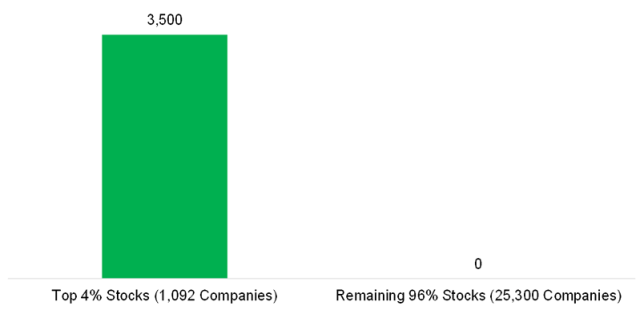

But the most critical case against tax-loss harvesting is that, like direct indexing, it is just more active management. Hendrik Bessembinder demonstrated that just 4% of all stocks accounted for almost all the excess returns above short-term US Treasury bonds since 1926. Most stock market returns come down to a handful of companies, like the FAANG stocks in recent years. Not having exposure to any of these in order to, say, maximize tax benefits, is just too risky a choice for most investors.

Shareholder Wealth Creation in Excess of One-Month US T-Bills, 1926 to 2016, US Trillions

Further Thoughts

Investors have realized that active management is challenging and thus allocated more than $8 trillion to ETFs. If you can’t beat the benchmark, invest in the benchmark. This may sound simple and a little boring, but it’s an effective solution for most investors.

Direct indexing is the antithesis of ETFs and is a step backward for investors. Like ESG or thematic investing, it is no free lunch. Investors need to know that their choices come with a price. Since most investors have underfunded their retirements, they should aim to maximize their returns and avoid any unnecessary risks.

Fully customized portfolios have historically been the exclusive domain of high-net-worth clients. Perhaps they should remain so.

For more insights from Nicolas Rabener and the FactorResearch team, sign up for their email newsletter.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Aaron McCoy

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.