Article content

(Bloomberg) —

[ad_1]

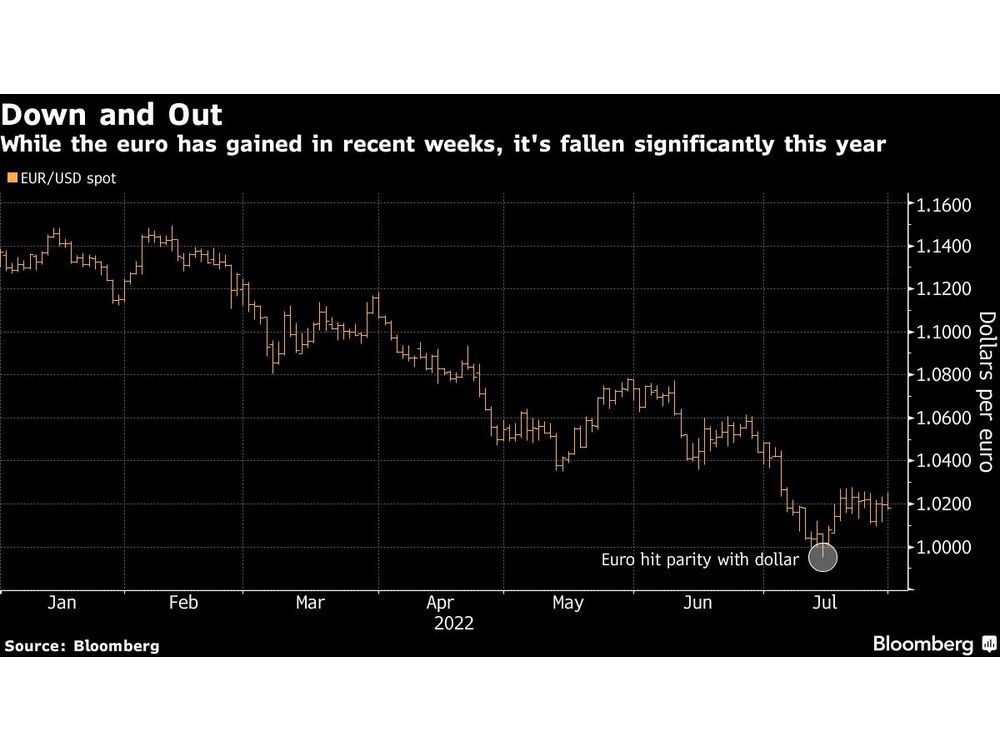

The euro, already beaten down this year to the lowest in two decades, remains an unloved currency stuck under relentless pressure as its economy stumbles toward a recession.

Author of the article:

Bloomberg News

Alice Gledhill

Publishing date:

Jul 31, 2022 • 10 minutes ago • 4 minute read • Join the conversation

(Bloomberg) —

This advertisement has not loaded yet, but your article continues below.

The euro, already beaten down this year to the lowest in two decades, remains an unloved currency stuck under relentless pressure as its economy stumbles toward a recession.

It’s hanging on just above parity with the dollar, after a brief dip below that level earlier this month for the first time in more than two decades. The currency has become a lightning rod for the mounting pessimism about the euro area’s economy. It’s fallen more than 10% versus the dollar this year, and many analysts say the likely direction from here is further down.

Much of the economic gloom is centered on the disruption of Russian energy supplies to Europe, which particularly threatens German industry. Credit Suisse sees a 50% chance of the euro region falling into a recession in the next six months. Goldman Sachs says it may already be in one.

This advertisement has not loaded yet, but your article continues below.

Italy is also a big source of worry amid political turmoil that led to the departure of Prime Minister Mario Draghi. S&P Global Ratings lowered its outlook on the country’s debt, and a key gauge of risk, the spread of Italian bond yields over Germany’s, is around the highest since 2020. Nerves over Italy leaving the euro are showing up in credit default swaps, though it’s seen as a very remote risk.

From a price perspective, the euro is faring even worse than in 2012 — the low that year was $1.20. It was trading around $1.02 after slipping to 99.52 US cents on July 14.

JPMorgan Chase and Rabobank see it sliding as low as 95 cents given Europe’s exposure to the energy crisis. Option pricing puts the odds on a drop to parity by the end of the year at around 70%. The Bloomberg consensus forecast for year end is $1.06.

This advertisement has not loaded yet, but your article continues below.

But for all the negativity, there’s little talk that the region is heading for another existential crisis like it suffered a decade ago, when high debt levels and soaring bond yields led to speculation that the region could break up. That ultimately led to Draghi — at the time European Central Bank president — saying he’d do “whatever it takes” to protect the currency. A schism is a fringe thought now, and the ECB has moved faster to keep markets in check.

Stagnating Economy

“In some ways the situation is more dire than 10 years ago, and in others, more benign,” said Themos Fiotakis, global head of FX & EM Macro Strategy at Barclays Plc. “It’s less of a deleterious problem for the integrity of the euro as a currency. But economically, growth could prove to be a bigger issue than back then.”

This advertisement has not loaded yet, but your article continues below.

Much of the currency’s depreciation is linked to that poor economic backdrop, marked by a mix of slowing growth and spiking inflation. On Friday, data showed Germany — Europe’s No. 1 economy — stagnated while inflation in the 19-member currency bloc soared to a fresh record of 8.9%, surpassing forecasts.

Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

Also in the mix is monetary policy divergence. The ECB raised interest rates by 50 basis points last week, but the Federal Reserve has tightened more than four times as much this year after adding another 75 basis points to its benchmark on Wednesday.

Euro-zone breakup predictions haven’t disappeared entirely. Founder of macro hedge fund EDL Edouard de Langlade argues that it’s possible, and is targeting a euro-dollar rate of 80 cents.

This advertisement has not loaded yet, but your article continues below.

But the ECB is being proactive, remote as they are. Along with its rate hike this month, it unveiled a new tool intended to prevent fragmentation, where there’s an unjustified divergence in the debt spreads of euro members.

“Today, the main risk is inflation risk,” said Nicolas Forest, head of global fixed income at Candriam. “The most important message was how the ECB can normalize the situation, without creating a debt crisis. The idea now is to avoid something, not to fix something.”

The ECB’s job is being complicated — and not for the first time — by Italian politics. The country will hold an election in September, and a rightwing alliance is currently leading in polls. Bond prices are shifting on concern about the policies of such an administration, making it tough for the ECB to step in and say market moves are unwarranted.

This advertisement has not loaded yet, but your article continues below.

Still, far-right leader Giorgia Meloni plans to stick to European Union budget rules if she leads the next government, according to officials familiar with her thinking. Investors say it’s unlikely that Italy would renege on commitments and jeopardize access to about 200 billion euros of European Union funds.

That support is due to be paid as part of the NextGenerationEU program — a major breakthrough in fiscal sharing triggered by the pandemic, and which separates the EU now from the EU of past crises.

“That was Europe crossing the Rubicon that no-one thought it could cross,” said Rohan Khanna, a strategist at UBS Group AG. “It was a high point in European integration. There are still cracks, but it’s a very different world to what it was in 2010.”

This Week

This advertisement has not loaded yet, but your article continues below.

Sign up to receive the daily top stories from the Financial Post, a division of Postmedia Network Inc.

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Financial Post Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

[ad_2]

Image and article originally from financialpost.com. Read the original article here.