[ad_1]

A low interest rate environment makes growth stocks the only ones worth researching.

Turn on Bloomberg, CNBC, or any other finance news network and you will hear professional investors, wealth managers, and commentators mourning the demise of value stocks.

Since value stocks have underperformed growth stocks by a wide margin over the past 10 years, we decided to explore whether fundamental investors looking for mispricings are best off ignoring them altogether going forward.

We did this by modeling the profits an investor would make over different interest rate environments. In each scenario, our hypothetical investor can allocate their time and effort to finding a 10% market mis-estimation in the stock’s terminal value, dividends, or growth rate in dividends. We then calculated the returns generated by finding this mis-estimation over varying federal funds rate environments.

Our method to determine the stock value in all scenarios followed the discounted cash flow model (DCF), with the standard model inputs of interest rate (Federal Funds Rate + Risk Premium), G (Growth Rate in Dividends), D (Dividends), and Terminal Value of the firm.

The model is completely agnostic as to whether growth or value will outperform over the next 10 years. We simply sought to understand where our investor’s attention is most profitably directed in different rate environments. For example, with rates approaching zero today, should the investor research stocks for a market mis-estimation of expected earnings, growth rate, etc.?

To answer this, we first isolated the value to an investor of finding a market mis-estimation of the growth rate in dividends. Our analytical model is presented below and assumes our investor finds a one percentage point mis-estimation in the growth rate of dividends. In this instance, a 1% growth rate becomes a 2% growth rate in dividends.

By finding this mis-estimation, the investor can earn a 13.6% return by doing their research under the other parameters detailed in the example: 1% Federal Funds Rate, 4% Risk Premium, 50-year horizon, $100 Dividend, and $10,000 Terminal Value.

Research Scenario: Shift in Growth Rate

| Before Research | After Research | |||

| Federal Funds Rate | 0.01 | Federal Funds Rate | 0.01 | |

| Risk Premium | 0.04 | Risk Premium | 0.04 | |

| R | 0.05 | R | 0.05 | |

| G | 0.01 | G | 0.02 | |

| D | 100 | D | 100 | |

| Terminal Value | 10000 | Terminal Value | 10000 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | Terminal Value (50) | ||

| PV (Pre-Research) | 3013.5 | 95.24 | 91.61 | 88.12 | 84.76 | 81.53 | 78.42 | 75.44 | 72.57 | 69.8 | 872.04 |

| PV (Post-Research) | 3423 | 95.24 | 92.52 | 89.87 | 87.31 | 84.81 | 82.39 | 80.03 | 77.75 | 75.53 | 872.04 |

| Gain from Research | 13.6% |

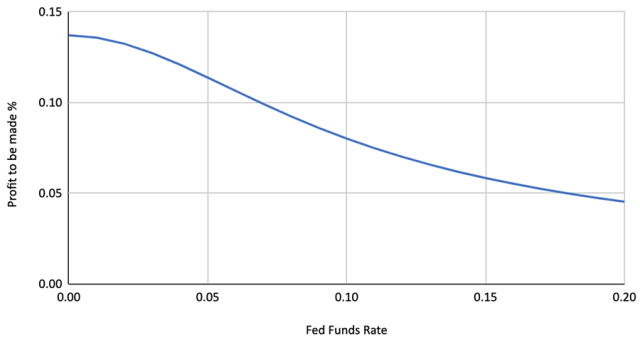

We took this growth rate mis-estimation model and ran it through different interest rate environments, starting with a federal funds rate of 0 and going up to 20%. The following graph details the results using the DCF model and the parameters outlined above. The takeaway? Researching a mis-estimation in the growth rate of dividends yields is most profitable for an investor in low interest rate environments. As the federal funds rate increases, the potential returns of such an approach decline.

Growth Rate Search: Profit to Be Made vs. Federal Funds Rate

Using the same model, we repeated this analysis with a focus on the terminal value of the company, perturbing the terminal value by 10% to represent the returns an investor might generate by researching it. The table below depicts that scenario over 10 years. It nets the investor an 8.39% return.

Research Scenario: 10% Shift in Terminal Value

| Before Research | After Research |

|||

| Federal Funds Rate | 0.01 | Federal Funds Rate | 0.01 | |

| Risk Premium | 0.12 | Risk Premium | 0.12 | |

| R | 0.13 | R | 0.13 | |

| G | 0.01 | G | 0.01 | |

| D | 100 | D | 100 | |

| Terminal Value | 10000 | Terminal Value | 11000 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | Terminal Value | ||

| PV (Pre-Research) | 3508.04 | 88.50 | 79.10 | 70.70 | 63.19 | 56.48 | 50.48 | 45.12 | 40.33 | 36.05 | 32.22 | 2945.88 |

| PV (Post-Research) | 3802.63 | 88.50 | 79.10 | 70.70 | 63.19 | 56.48 | 50.48 | 45.12 | 40.33 | 36.05 | 32.22 | 3240.47 |

| Gain from Research | 8.39% |

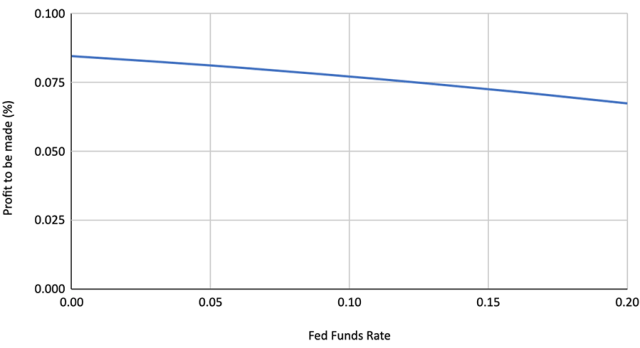

Again, we mapped this out over different interest rate environments and found that this approach pays off the most in low-rate environments. In longer horizon models — with a 30-year rather than 10-year model — returns decline much more steeply as the federal funds rate increases.

Terminal Value Research: Profit to Be Made vs. Federal Funds Rate

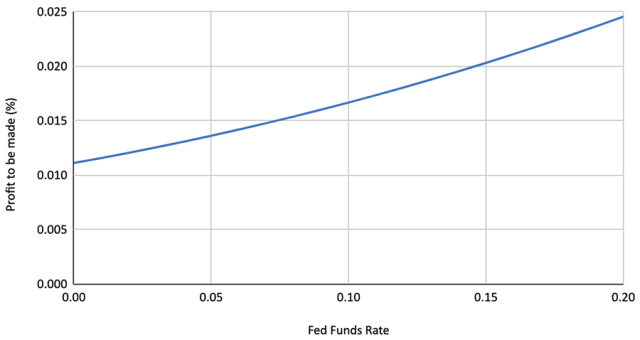

Finally, we ran the analysis with a focus on current dividend paid. We perturbed the current dividend paid by 10% and ran the scenario over different interest rate environments. As the following graph demonstrates, researching the current dividend paid nets investors the greatest returns in high interest rate environments.

Current Dividend Analysis: Profit to Be Made vs. Federal Funds Rate

We re-ran all the above analyses using different time horizons, risk premium levels, and dividend levels and find qualitatively similar results as those in the preceding graphs.

All in all, the results highlight that in a near-zero interest rate environment, investors ought to keep an eye out for companies with high terminal values and significant growth rates in their earnings/dividends. In other words, growth stocks.

On the other hand, in a high interest rate environment like that of the 1980s, investors would be better off targeting the true current dividend paid by a firm. Which means they should be on the lookout for value stocks.

Back in June, US Federal Reserve chair Jerome Powell said, “We’re not even thinking about thinking about raising rates in the near future.”

What does that mean for fundamental investors?

In this current low interest rate environment, they should concentrate on researching, debating, and trading growth rather than value stocks. The better their estimates of the correct terminal value or growth rate in earnings / dividends, the more profit they can make.

And that means focusing their efforts on determining the true value of the Teslas, Snaps, and Zooms of the world for the foreseeable future.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / MirageC

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.