[ad_1]

Shareholder activism has been on the rise in Japan. Will the trend continue in the post–COVID-19 world?

Shareholder activism in Japan rewards shareholders with positive abnormal returns, at least in the short run. That’s according to a new study we conducted at the Monash Centre for Financial Studies.

This finding suggests that by actively engaging with investee companies, investors could potentially unlock shareholder value. However, recent protectionist moves by the Japanese government may hinder such efforts, especially for foreign investors.

Shareholder activism is broadly defined as the application of pressure by shareholders to influence or change company behavior. It comes in various forms and can involve public campaigns as well as private engagement between shareholders and companies.

Unlike in the United States and Europe, where investors are increasingly focused on environmental, social, and governance (ESG) issues, in Japan thus far business performance and governance have been shareholder activism’s dominant focus.

Until about a decade ago, public shareholder activism in Japan was rare, and nearly always unsuccessful, particularly when it involved hostile campaigns by foreign investors. The most famous of these came in 1989 when US investor T. Boone Pickens made a bid for three board seats at Koito Manufacturing Co. Toyota, a key Koito shareholder and customer, along with other shareholders, voted it down. It was one of several high-profile early examples of cross-shareholdings — a common feature of corporate culture in Japan — and the use of business ties to suppress activist shareholders.

Although levels of cross-shareholding have decreased in recent years, they can still be significant enough to present a barrier to external pressure.

Activists face other persistent challenges. Given the historical dependence of Japanese companies on debt rather than equity financing, there is cultural resistance to the notion of shareholder rights. There is also a widespread belief that a company’s first obligations are to employees and customers rather than shareholders.

Still, the growth in shareholder activism in Japan has been buttressed over the last decade by substantial changes in the corporate legal and regulatory environment. Often referred to as “Abenomics,” these measures were implemented under Prime Minister Shinzo Abe.

The Corporate Governance Code (2015) and Stewardship Code (2014), and subsequent revisions to both, featured reforms meant to enhance corporate value and capital efficiency after decades of stagnation. In the new environment, cash-rich firms with low valuations, low efficiency, and low profitability have been targeted by activist shareholders.

The nation’s largest investor, the Government Pension Investment Fund of Japan (GPIF), has also helped change the corporate governance and stewardship landscape by requiring its asset managers to disclose and explain their voting records at the annual general meetings (AGMs) of investee companies.

From January 2013 to June 2019, a total of 246 activist campaigns targeted 130 different Japanese companies. Approximately two-thirds of the targeted firms were in the consumer goods, services, and technology sectors. While there were more public demands on large-cap firms initially, demands on small-cap and micro-cap firms have grown more strongly of late.

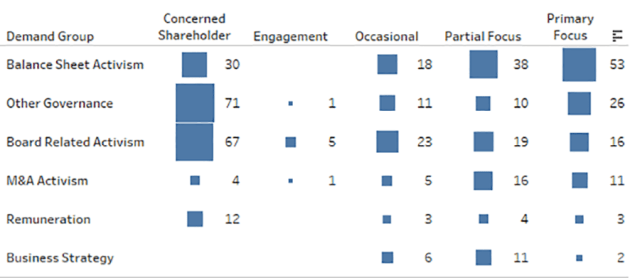

Through these campaigns, shareholders filed 456 demands with the companies. Most of these pertained to issues related to the firms’ balance sheets and boards. The top three concerns among investors involved dividend payments, board representation, and CEO/director removal.

Types of Demand by Activist Groups

Activist shareholders

pursuing M&A and board issues held a significantly higher level of equity than in other cases.

Shareholder activism without a substantial block of shares was less effectual. The average equity held by shareholders whose proposals succeeded was approximately 17%, significantly higher than those associated with ongoing / unresolved (8.1%) or unsuccessful proposals (5.2%).

The rate of successful and partially successful cases based on the whole sample was 12.5%. The success rate of institutional shareholders with “engagement” strategies was highest at 33.3%, while individual activist shareholders had the lowest success rate.

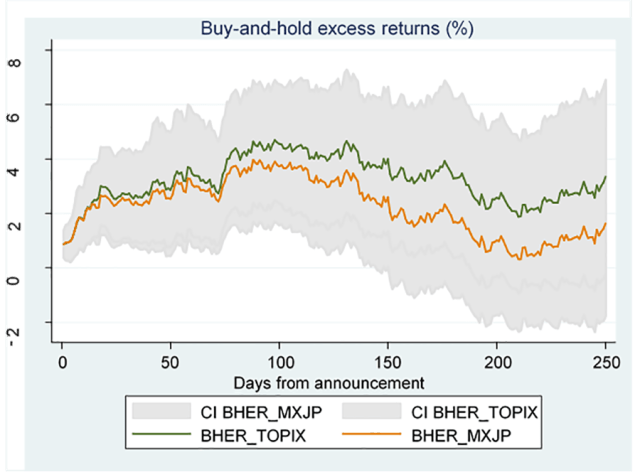

The study shows that shareholder activism created positive abnormal returns to shareholders, or different rates of return from what would be normally expected, given the level of risk relative to the market.

On the announcement date of the demand, the mean abnormal return was 0.68%. Since these firms had a total market value of almost US $1.23 trillion, this adds up to a one-day return of $8.4 billion for shareholders.

After that short-term surge, does shareholder activism increase share values over longer timeframes?

The study found that by buying the stock on the announcement day and holding it for 120 trading days or less, investors could earn significant positive buy-and-hold excess returns (BHER) — the return in excess of the market return based on the TOPIX Index or the MSCI Japan Small-Cap Value Index (MXJP).

Beyond 120 days, however, BHERs were not statistically significant.

Excess Returns over TOPIX and MXJP Indices

While the abnormal returns only held up over the short run, it does not necessarily follow that shareholder activism in Japan has little impact. Shareholder activists and companies often engage behind closed doors, so the extent and outcome of this activity could go well beyond what is measured in this study

The Japanese Government, however, has recently made some disappointing protectionist moves to ostensibly “prevent leakage of information on critical technologies and disposition of business activities for national security reasons.”

According to the newly amended Foreign Exchange and Foreign Trade Act, effective June 2020, foreign investors investing in 1% or more of the total shares of a listed company in designated sectors must submit prior notification if they want to become board members or propose transfer or disposition of important business activities of the invested company to the general shareholders’ meeting.

In another move, in December 2019, the government amended the Companies Act to limit the number of proposals a shareholder can submit at a shareholder meeting to 10.

Although the government said that the amendments will not restrict shareholder rights or engagement with invested companies, foreign activists will have more difficulty accessing their toolbox.

In the near future, as the impact of these amendments unfolds and companies struggle to recover in the post–COVID-19 world, shareholder activism in Japan may start to wane. These regulatory moves could unwind much of the Japanese government’s efforts at corporate governance reform over the last decade.

For more insight on this topic, the full research paper by Nga Pham, CFA, is available on the Monash University website.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / yongyuan

Professional Learning for CFA Institute Members

Select articles are eligible for Professional Learning (PL) credit. Record credits easily using the CFA Institute Members App, available on iOS and Android.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.