[ad_1]

Since the start of the “special military operation”, Russia has been under immense pressure from Western countries to withdraw from its offensive in Ukraine. Sanctions, the key tools of western governments, have been making matters increasingly uncomfortable for Putin.

With neither side willing to give an inch, matters finally came to a head with Russia defaulting on its foreign debt as a key payment deadline expired on Sunday night. This was the first such instance since 1918, way back, when an economically beleaguered, Lenin-led Russia simply canceled its foreign debts, leaving European investors holding the bag.

Are you looking for fast-news, hot-tips and market analysis?

Sign-up for the Invezz newsletter, today.

On Monday morning, Russia was unable to make interest payments on two Eurobonds, worth approximately $100 million, first reported by Taiwanese bondholders.

To clarify, a Eurobond is a bond that is issued in a currency other than that of the issuing country. The name can be a touch misleading but is not specific to euros or Europe in any way.

History may not repeat itself, but it sure does rhyme. More than a century after Lenin, another Vladimir has once again been at the helm, while Russia defaulted on its international obligations. If that sounds bad, it gets worse, when it becomes clear that it depends on who you ask.

According to Juan P. Farah Yacoub, Economist at the World Bank, bond contracts in Russia are often written in broad language, muddling the meaning of even key provisions, and generally favoring the sovereign. Even in the case of a default, pinning down if one has occurred or not, depends on the interpretation of “alternative payment currency and fiscal law clauses”, or in more dire circumstances, could even lead to litigation.

Further, Yacoub points out that “significant changes taking place since 2014” after Russia annexed Crimea, have made it even trickier for the bond documents to reveal their truth.

Regardless of whether this is a default or not, everyone agrees that Russian payments have not reached final bondholders.

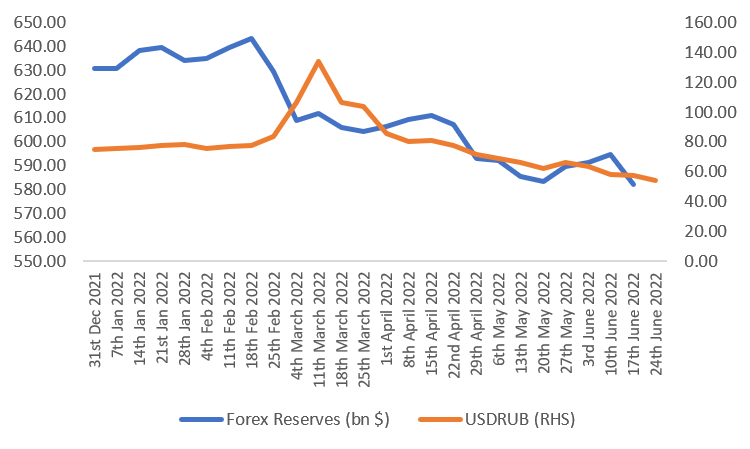

The latest figures from the Bank of Russia state that the country owns USD 582.3 billion in foreign exchange reserves, nearly 6000 times the interest amount. Moreover, the ruble has strengthened 29% this year, reaching a seven-year high, while oil revenues have surged. So, what’s going on?

Western sanctions

The US Dollar is the world’s reserve currency. With its unparalleled economic and political capital maintained throughout the twentieth century, financial institutions have been molded to heavily favor the United States.

For instance, the Society for Worldwide Interbank Financial Telecommunication (SWIFT) system is the gateway to the international payments mechanism and is central to global monetary flows. The dollar dominance has enabled the US to routinely block the use of this system by countries and parties that are acting ‘irresponsibly’.

With its invasion of Ukraine, the US-led international community threatened decisive action against Putin’s Russia. Shortly afterward, Russian banks were systematically excluded from the system in response to this year’s nasty turn of geopolitical events.

Reports suggest that before the war, Russia had access to approximately $640 billion combined in foreign exchange reserves and gold. However, with much of this being held in central banks outside Russia, a large chunk of these accounts was frozen.

The country was effectively side-lined from the global financial system, unable to borrow in the international markets, and later de-listed from several key indices. Rating agencies turned a cold shoulder as well.

However, the domestic economy benefited from a degree of normality, as the US Treasury’s Office of Foreign Assets Control (OFAC), in charge of sanctions, granted the Russian government a 9A license.

The 9A license allowed the Russian government and important financial institutions to service their debts to bondholders and international investors. The Russian central bank was able to deposit rubles in its own clearing house, which were then paid out as dollars to bondholders through US entities, on a case-by-case basis.

Strictly speaking, the general 9A license covered both “debt or equity” issued before February 24, 2022, until May 25, 2022.

Despite the onslaught of sanctions, Russia has been able to stay afloat by deploying various capital controls to maintain a strong currency, while supply disruptions have seen energy revenues soar.

Exemption expired

On April 6, the 9A license was superseded by the general license 9B and then the general license 9C, which meant that “unlike in prior weeks, when Russia was able to use otherwise frozen reserves to at least avert default; the new regulations forced it to choose between uses for declining hard currency reserves.”

Essentially, these licenses wound down the window until May 25th, meaning that Russia could no longer pay in rubles and expect US banks to do the needful. For bonds that did not offer a ruble option in the contract terms, Russia would have to make payments directly in global reserve currencies.

The country was granted a 30-day grace period to make good on interest payments.

With the Ukraine war showing no signs of abating, the United States elected to tighten the noose, with the Treasury Department allowing the licensing arrangement to expire, effectively preventing Moscow from servicing foreign debt payments at all via the US banking system.

On the 30th of June, a similar agreement with the UK is set to expire as well.

Russian response

The Russian government lays the blame for non-payment squarely on international clearing houses that did not convert ruble deposits into international currencies of choice, failing to satisfy the bondholders’ claims.

Despite being flushed with funds in principle, Finance Minister Anton Siluanov was quoted as saying, that the country has no “other method left to get funds to investors, except to make payments in Russian rubles.” He added that the “situation, artificially created by an unfriendly country…” is a “farce”.

For Russia, another $2 billion in payments is due by the end of the year, although most contracts post 2014 will allow for ruble payments in case of events “beyond its control”.

According to Adam Solowsky, a Partner at Reed Smith’s Financial Industry Group, with expertise in sovereign bond defaults, debt-burdened countries would ordinarily look to renegotiate the terms of their issued bonds. This is a unique case because “nobody can do any business with them.”

International markets were not sympathetic to Russia’s protests, with the Credit Default Determination Committee of The International Swaps and Derivatives Association, Inc, finding as early as June 7th, that Russia had been unable to pay the interest on bonds to international bondholders. However, given the politically charged situation and fluid nature of the war, the Committee did not recommend further actions.

Russian law, however, “considers its obligations paid in full with the transfer of the amount in rubles” to the National Settlement Depository (NSD).

This was supported by a Kremlin notice earlier this month from the offices of President Vladimir, which stated that “Obligations under the Eurobonds issued by the Russian Federation shall be recognized as properly met if executed in rubles… payment to the central depository. “

To operationalize this system, bondholders would need to open ruble and dollar accounts with Russian financial institutions to receive payments. According to Siluanov, the process would be similar to that for executed gas exports to Europe, but in reverse.

This may have appeared to be a promising avenue, with the NDS not subject to US sanctions at this point.

However, on the 24th of June, the European Union imposed additional restrictions on the NSD, stifling its room to maneuver.

Moreover, governments and multinational companies are unlikely to open such accounts, knowing full well, that it could harm their reputation and may expose them to sanctions action as well.

Russia is trying to pressure its European neighbors to make ruble payments for oil and gas, with some success.

Long-term impacts

Ambiguity in the contracts, modifications in debt instruments past 2014, expectations of bondholders, and the sovereignty of the Russian currency have come to loggerheads, clouding the question of whether Russia is even in default.

According to Yacoub,” From the vantage point of creditors, the event of default would be unequivocal – a missed payment. From the debtor’s point of view, it is making payments, presumably in accordance with its own law.”

Having already been excluded from the international markets, being officially labeled a defaulter may seem like a symbolic measure.

However, Russia is likely to fight tooth and nail, to rid itself of such a moniker. The effects of an official default status could be catastrophic, with borrowing costs rising sharply and capital drying up.

Global ratings hold great sway over the perception of creditworthiness in the financial markets.

In such an event, any chance of access to international finance would be dashed, even from partners such as China, as this could have knock-on effects on their creditworthiness as well, resulting in higher borrowing costs for that country.

Prospects for litigation

As discussed earlier, the standard protocol of renegotiating terms with the debtor country is off the table.

Investors must seek out alternative approaches.

What makes this more complicated is that different bonds have vastly different contract terms, especially those prior to and after 2014, and post the infamous poisoning incident in the UK in 2018.

To formally declare a default, 25% or more of the bondholders need to report that they have not received their payments. After this, they could seek a court judgment to direct payment.

To get a better idea of the potential scenarios at play, consider reading this report from the World Bank. Some important terms to keep in mind include cross-acceleration, pari passu, asset seizures, and English law.

Litigation, especially so early in the game, may eventually swing either way and may hurt investors in the long run. As per Jay S Auslander, a sovereign debt lawyer at Wilk Auslander, it is better to “hang tight for now” due to several unknown factors.

Moreover, Russia does not accept the jurisdiction of any court over what it views as a sovereign matter while sticking to its guns, that it has not defaulted.

Zia Ullah, Partner at Eversheds Sutherland does not accept this line of reasoning, saying,” … if you know the money is stuck in an escrow account… you have not satisfied the conditions of the bond.”

Next steps and Russia’s broader economic problems

Timothy Ash, the senior emerging markets sovereign strategist at BlueBay Asset Management, believes that with permanent restrictions from OFAC preventing any dealing in US dollars, “the move will keep Russia in default for years to come”, until “the U.S. Treasury gives bondholders the green light to negotiate terms.”

With so much geopolitical, economic and legal uncertainty, most bondholders will likely take a wait-and-watch approach for the time being.

In the meantime, Russia’s exclusion from the global financial system and ever-appreciating ruble may lead to a crash in export revenues and precipitate a deep recession, amid falling international demand.

If Russia continues to be squeezed and corporate exits continue at the rate of knots, eventually, this would lead to lower foreign investment, a drop in living standards, and a sustained decline in its economic power.

International pressure continues to mount, with the G-7 expected to announce new actions against Russia on Tuesday, the 28th.

Despite the dire situation in Russia, Kristalina Georgieva, IMF Managing Director insists that this will “definitely not be systematically relevant”.

eToro

10/10

68% of retail CFD accounts lose money

[ad_2]

Image and article originally from invezz.com. Read the original article here.