[ad_1]

The toxic cocktail of unanticipated consequences stemming from MiFID II research rules has a potent new ingredient: the coronavirus market drawdown. This may accelerate a regulatory review of MiFID II research rules in a post-Brexit Europe.

While regulation takes time, the impact of MiFID II, combined with COVID-19, on the investment processes of US and European asset managers is unfolding in real time. The active equity strategies of European managers are at significant risk.

As profound economic and structural change may emerge from the pandemic, access to research has never been more important. Yet, never has the global research playing field been less even for asset managers — depending upon their research funding methodology.

Divergent commercial models between US and European asset managers are furthering the already gaping divide between the research haves and have nots. US research budgets are correlated with trading volumes, which are up significantly post-COVID-19, while European (P&L) research budgets are correlated with manager assets under management (AUM)/profitability, which are down significantly post-COVID-19.

This may call into question the “sustainability” of some European funds, particularly in “research-intensive” strategies.

Background

MiFID II was a game changer but did not lead to the global regulatory convergence that European regulators and asset managers hoped for.

- MiFID II resulted in substantial research budget cuts by the vast majority of European P&L managers. While research costs to asset owners are low, when this cost is transferred to an asset manager P&L, it’s frequently their second largest cost — exceeded only by staff compensation. This creates a direct conflict between research spending and manager profitability.

- The French regulator (AMF) sponsored a report in January 2020 that concluded MiFID II had:

- a negative effect on SME research.

- caused French asset managers to cut research budgets by between 50% and 75%.

It recommended a raft of MiFID reforms including exempting smaller managers from MiFID II and a Europe-wide review of the research inducements regime. ESMA is currently gathering data on this issue.

- In the United States, the Securities and Exchange Commission (SEC) has no appetite for research via P&L over concerns about research spending cuts damaging the US research ecosystem.

- MiFID II is an issue for US asset owners because, while they continue to pay for research, their managers are frequently absorbing research costs for European clients. However, US asset owners are in no hurry to repeat the European experience.

- US asset owners — and CFA Institute — have recommended that the SEC maintain the current research commission system with the proviso that asset managers:

- disclose the quantum of research payments at the fund/client level.

- demonstrate that the asset owner’s research commissions are being used for its portfolio alone — not for other investors. So no cross-subsidization.

This suggests that the US market will continue to use client money for research. Does this research funding divergence matter?

The Data

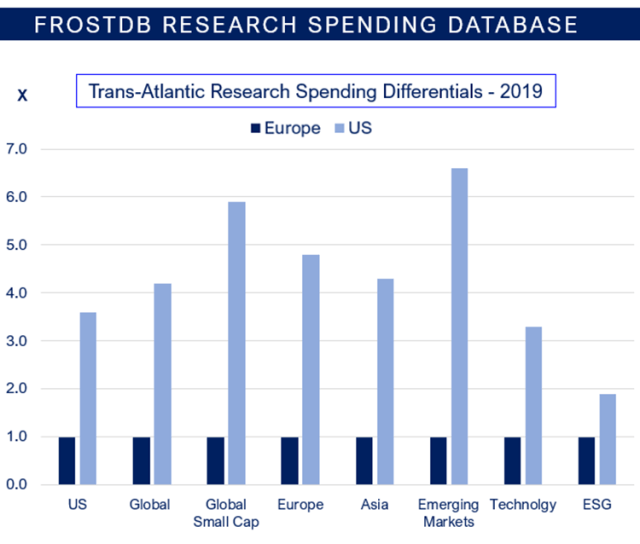

The FrostDB research database illustrates immense gaps in research spending between US (client money) and European (P&L) managers. This is before the COVID-19 impact.

On average, US managers in 2019 spent 4.1 times the amount on research for global equity mandates versus European managers. This represents less than 10 basis points (bps) of spending in a category that returned 2,500 bps in 2019. However, the spending gap is wide enough to have a material impact on the information available to investment teams. The biggest divergences appear in the most research-intensive categories, small-cap and emerging markets.

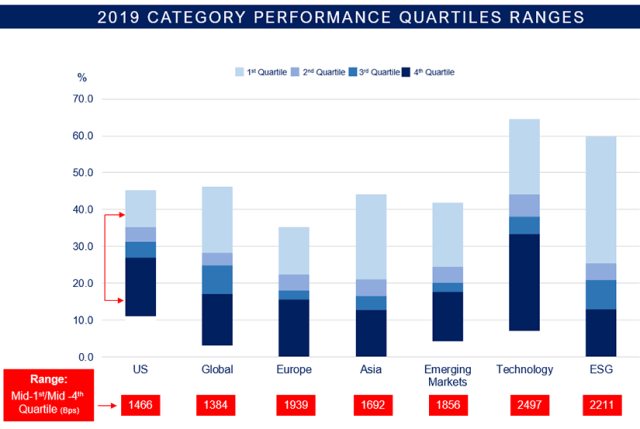

Research Costs Dwarfed by Differences in Fund Performance

Frost Consulting has updated work done with Stanford examining the relationship between research costs for asset owners — less than 10 bps — and the variance in fund returns. This should be a major factor in asset owner deliberations on research funding models and may explain why US asset owners are willing to continue to pay for research.

Across 16 equity categories in 2019, the average difference between mid-first and mid-fourth quartile performance — in the red boxes — averaged 1,500 bps. This is a vast multiple of any research budget. The total range per category frequently exceeded 4,000 bps.

Impact of Research Spending on Performance?

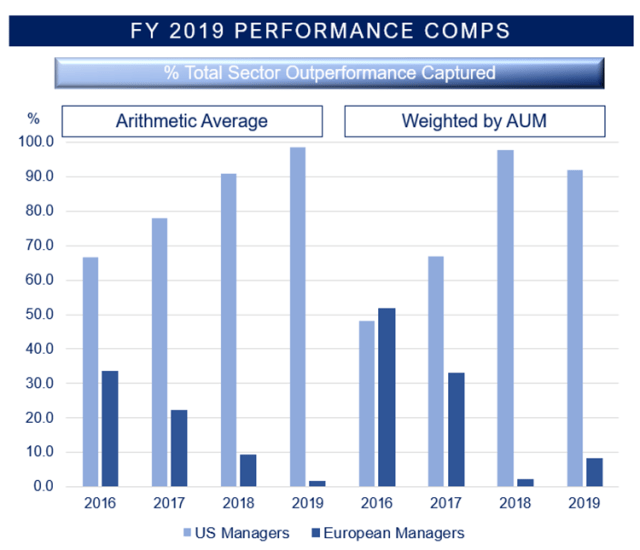

Frost Consulting and EvercoreISI examined multi-year performance trends of funds in like-for-like categories — US; equities; emerging markets; environmental, social, and governance (ESG); etc. — run by both US and European managers. In total, ~5,000 funds with AUM of ~$10 trillion were included. The data captures both pre-MiFID II/pre-2018 and the aftermath when trans-Atlantic research spending gaps became pronounced.

US managers, despite running 80% of the AUM, have harvested the bulk of the outperformance over the period. While many factors can contribute to performance, research is an important input.

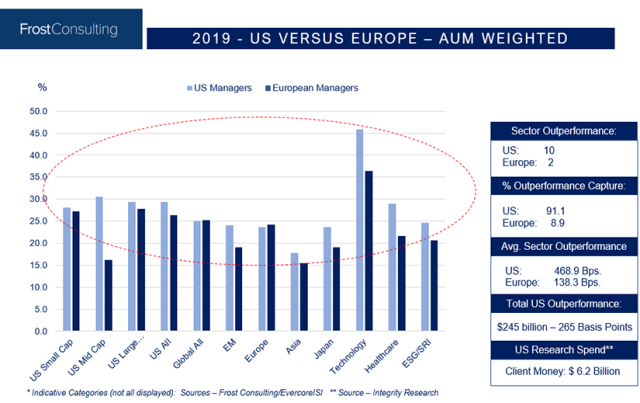

Representative Sector Detail

US managers outperformed in the vast majority of sectors. In aggregate, the 2019 US outperformance totaled 265 bps — roughly $245 billion. This compares to an estimated $6.2 billion of asset owner research commissions spent by US managers on external research.

COVID-19 Overlay

US managers outspent European managers in 2019 by ~3.8 times in our sample. Frost estimates this may have jumped to ~5.8 times as of April 2020 (assuming a full year), as 40% higher equity volumes boost US research budgets and 20% lower AUM/profitability at European managers has a leveraged negative effect on theirs.

Ironically, the lower markets (and AUM) go, the less research European managers will be able to access.

This raises the question of whether the minimal research “savings” for asset owners from the P&L method are serving their interests or meeting the transparency objectives of MiFID II.

Is European fund research spending an ESG issue? It certainly calls into question fund sustainability, transparency, and governance. Perhaps COVID-19 will be the catalyst for a sober re-examination of the risk / reward balance in research funding methods.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / brytta

Professional Learning for CFA Institute Members

Select articles are eligible for Professional Learning (PL) credit. Record credits easily using the CFA Institute Members App, available on iOS and Android.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.