[ad_1]

Like it or not, companies are judged

by flawed standards.

GAAP sometimes misrepresents business reality. Let’s use that fact to generate some alpha.

Continuing from the first memo, we’ll start by examining revenue recognition, the cash conversion cycle, and free cash flow.

“Revenue” isn’t revenue, it’s contract timing.

Revenue is recognized when a contract

between a business and a customer has been performed.

Here’s how it’s done according to FASB:

The Revenue Recognition Process

1. Identify the contract with a customer.

2. Identify the performance obligations (promises) in the contract.

3. Determine the transaction price.

4. Allocate the transaction price to the performance obligations in the contract.

5. Recognize revenue when (or as) the reporting organization satisfies a performance obligation.

Source: FASB

There are several areas where GAAP

revenue recognition can hit a snag and you can find an opportunity.

1. Multiparty Transactions

In multiparty transactions, “revenue” can mean gross revenue dollars in a transaction or a subset that is recognized as one company’s net revenue. Your last $20 Uber ride probably generated $16 in net revenue for the driver and $4 in net revenue for Uber.

Net revenue can get distorted when multiple parties transact before an end customer receives a product. Imagine that a drug manufacturer controls a distributor and the distributor increases its orders in anticipation of end customer demand. These new orders puff up the manufacturer’s net revenue numbers. But what if the end customer demand doesn’t materialize? The manufacturer’s reported organic revenue growth might just be pulling forward future revenue and stuffing it into the distribution channel. These category definition games can present traps for growth investors and potential alpha for shorts.

2. Changes in Performance Criteria

When performance criteria change, reported revenue can become an unstable metric. For example, the same software sale can result in different GAAP revenue numbers depending on whether it is structured as a license or a subscription. Subscriptions show less GAAP revenue early on but may reduce customer churn over time. Shrinking GAAP revenue is not a good look in the public markets. That’s why the perpetual-license-to-SaaS transition is a popular private equity play: You can take a company private to change its accounting standard outside of the spotlight, then bring the company public with freshly cleaned books and a new story. Companies that do make this kind of transition while public, like Adobe, can present meaningful alpha opportunities for investors who understand how the future accounting will turn out.

3. Multiyear Contracts

Should it matter if a transaction is recognized on 31 December or 1 January?

Companies want to report strong year-over-year growth for each period. Savvy customers wait until the end of a quarter and then ask for a discount to book a transaction before the period ends. It’s similar to buying a used car after Christmas from a salesperson who is desperate to make their year-end quota. In bad scenarios, a company can get caught pulling forward discounted demand every quarter just to chase last year’s numbers. In the worst case, that company will run out of future demand to pull and their sales pipeline will fall flat.

But GAAP doesn’t make it easy to distinguish between temporarily pulled forward contracts (noise) and increasing customer demand (signal). This is also true in reverse — GAAP revenue doesn’t differentiate between slowing customer demand (signal) and temporary sales delays (noise).

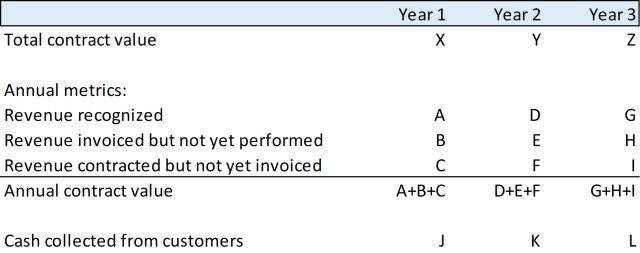

Private investors can look at what I’ll call “the contract term structure.”

The Contract Term Structure

What you’d really like to see in GAAP is annual contract value (ACV) and total contract value (TCV). ACV is the amount of business currently under contract for that year — whether it’s already recognized as revenue, invoiced but not performed, or contracted but not yet invoiced. TCV includes contracts and invoices for future years. With ACV and TCV, you could see revenue recognition within the context of the full sales picture.

But any FASB proposal to add the contract term structure to GAAP would meet with stiff resistance. School would be a lot easier if you could grade your own homework. Imagine a high schooler’s incentive to give their parents “strong guidance” for this semester’s report card. Even the best students would want to keep their performance secret — why let the competition know how you are doing? So the contract term structure will likely stay hidden and, thus, be an excellent spot to hunt for opportunities.

Revenue is just GAAP contract timing.

So long as public investors overweight these reported numbers, the

contract-to-revenue recognition process should remain a recurring alpha source.

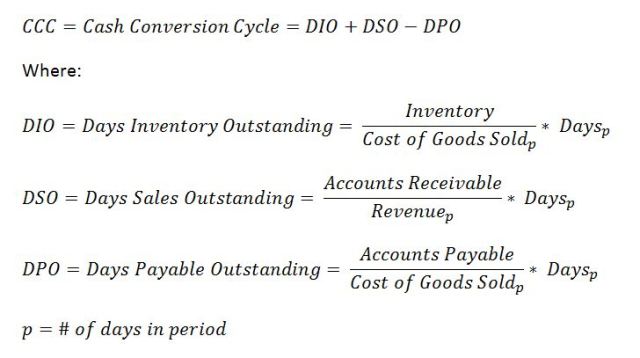

The cash conversion cycle should be measured as a percentage and include deferred revenue.

The cash conversion cycle

(CCC) measures how long each dollar of working capital is invested in the

production and sales process of an average transaction.

The idea is to track working capital

efficiency from the cash paid to suppliers to the cash collected from customers.

The Cash Conversion Cycle (Current Formula)

The CCC is like a mini return on

equity (ROE). Each driver can be improved in order to increase the return on

working capital. But unfortunately, there are two flaws with the current CCC

metric.

The first problem is that the CCC is calculated in days. What we’re really measuring is capital efficiency over a period of time, usually a year. That’s a ratio. Nobody calculates ratios in days. We should measure the CCC as a percentage.

The second and more critical problem

is that a term is missing. The CCC currently includes accounts receivable (cash

owed by customers), accounts payable (cash owed to suppliers), and inventory

(cash paid in advance to suppliers).

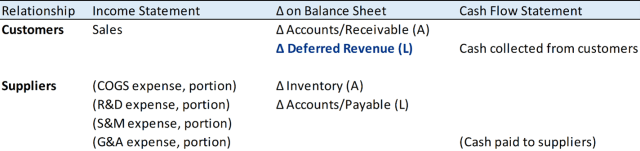

What’s missing is current deferred revenue (cash collected in advance from customers). It’s easy to see the CCC’s oversight when we look at the other working capital line items related to customers and suppliers:

The Cash Conversion Cycle Should Include Deferred Revenue

Updating the CCC makes it easier to

identify capital-light businesses.

Businesses that collect cash from their customers ahead of contract performance (deferred revenue) can be highly cash-efficient. But if the CCC excludes deferred revenue, then investors might overlook that these businesses can expand at GAAP net income losses without dilutive equity raises. This omission may explain why SaaS and consumer subscription businesses were misvalued five years ago. If you can find the parallel today, you’d be like the public SaaS investors of 2016, well ahead of the curve.

The updated CCC also makes it easier to flag the dreaded SaaS death spiral. Quickly growing companies can be quite fragile when they depend on deferred revenue to meet ongoing cash needs. If their GAAP revenue growth peters out, they may rapidly find themselves in a cash shortfall. Bizarrely, these companies can show excellent GAAP revenue numbers while teetering on the edge of bankruptcy. If the CCC doesn’t include deferred revenue, you won’t be able to see the canary in the coal mine.

“Free cash flow” isn’t free cash flow, it’s an accrual metric.

“Free cash flow” doesn’t always equal the actual cash generated by a business.

This raises a problem for academic finance because the keystone model for stock valuation is John Burr Williams’ discounted cash flow (DCF) analysis. You might ask, if investors can’t reliably measure free cash flow (FCF), how can they reliably discount and value those cash flows? Good question.

Here’s the standard definition for free cash flow:

The Standard Free Cash Flow Equation

| Factor | Location |

| + Cash Flow from Operating Activities | Statement of Cash Flows |

| + Interest Expense | Income Statement |

| – Tax Shield on Interest Expense | Income Statement |

| – Capital Expenditures (Capex) | Statement of Cash Flows (Cash Flow from Investing Activities) |

| = Free Cash Flow |

Source: Investopedia

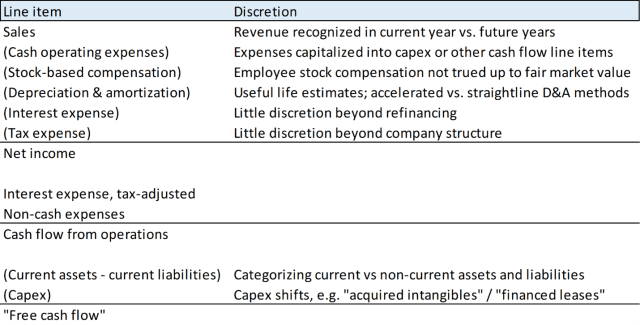

This all seems straightforward until

you look at how much discretion goes into the accrual numbers for a given

period and how much those accrual numbers impact FCF.

Why “Free Cash Flow” Might Not Be Free Cash Flow

Internally-developed intangible assets are the danger area in today’s market. Most investors agree that we should capitalize some portion of R&D and SG&A expenses, but no one is sure how long these intangible assets will last. Google’s search engine should endure in some form for decades to come; AskJeeves, not as likely. How can we come up with a consistent rule to amortize the Google and AskJeeves engineering efforts ex-ante?

To make matters worse, intangible capex may be hidden in line items that aren’t included in FCF calculations. If you look closely, a company’s acquired intangibles and financed leases might just be capex in disguise. Properly accounting for internally developed intangibles may be the most significant unsolved problem in GAAP.

Investors who focus on free cash flow yield often analogize equity dividends, rightly or wrongly, to bond coupons. But because current FCF is chock full of these accrual assumptions, we can’t naively project current FCF to estimate normalized FCF. Companies have a strong incentive to pump that perceived equity coupon. That juiced FCF yield is akin to a shaky bond with a high yield, also known as a fool’s yield.

The alpha opportunity is identifying when normalized FCF will differ significantly from current FCF. Stocks where the company needs to cut the equity yield — be it dividends, stock buybacks, or debt payments — can be good shorts. Long opportunities can arise when a major portion of current capex, R&D, or sales spend flips to an amortizable fixed cost. The real difficulty is ensuring that the fixed asset you are betting on isn’t about to become stranded — lest you end up backing AskJeeves instead of Google.

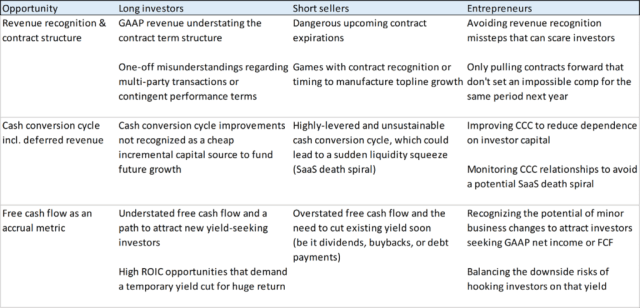

Moving to the Balance Sheet

Here’s how the puzzle pieces begin to fit together for longs, shorts, and entrepreneurs:

We can recharacterize the balance sheet too. From there, we can revisit the weighted average cost of capital as well as the market value of equity and share-based compensation.

You can read more from Luke Constable in Lembas Capital’s Library.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Photo by Darío Martínez-Batlle on Unsplash

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.