[ad_1]

Two Magic Words

“This time is different” might be the four most dangerous words in investing. “Uncorrelated returns” may just be the two most lucrative. These seven syllables have been applied across the span of the alternative investment industry, from hedge funds and venture capital (VC), to private equity and real estate.

Investors have allocated more than $10 trillion to these alternative investments, paying high fees while hoping that these provide positive returns and diversification benefits for traditional stock and bond portfolios.

But investor sentiment towards alternatives varies across the spectrum. Despite racking up impressive returns in recent years, VC is still tainted by the 2000 implosion of the tech bubble as well as complete write-downs of investments. WeWork-like debacles do give investors pause when they consider VC allocations.

Low alpha generation has sapped hedge funds of much of their prestige in recent years. Improved analytics have also shown that much of their alpha was really alternative beta that could be harvested more efficiently via cheaper liquid alternative products. Consequently, hedge funds have not grown their assets under management (AUM) all that much of late.

In contrast, investor bullishness on private equity may be at an all-time high. It is the most popular alternative asset class, according to the Preqin Investor Outlook for Alternative Assets in 2019, with a 9.9% target allocation for institutional investors based on the assumption of high absolute and uncorrelated returns.

Since some alternative asset classes have already disappointed, however, cautious investors might also question private equity’s core assumptions.

So does private equity provide uncorrelated returns relative to equities?

Private Equity vs. Public Market Returns

As Peter Drucker observed, “If you can’t measure it, you can’t manage it.” While gauging the performance of mutual funds in public markets is relatively easy since investable benchmarks are readily available — usually as cheap exchange-traded funds (ETFs) — alternative asset classes often lack such metrics. This makes it hard to analyze a strategy’s returns and creates an information asymmetry that favors the asset manager over the investor.

In private equity, returns are calculated by money-weighting them in contrast to the time-weighted returns of public markets. These returns are not directly comparable, so researchers have created public market equivalent returns. These invest in public markets by mimicking private equity cash flows.

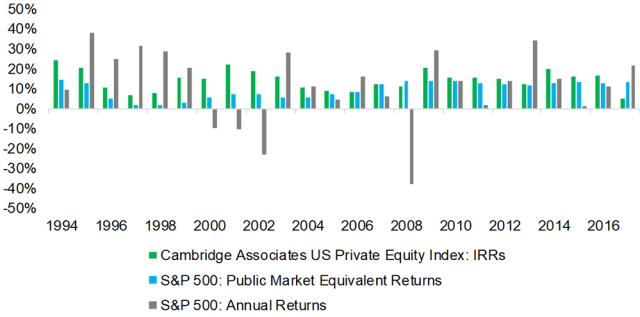

We compared the annual internal rate of returns (IRRs) of US private equity funds, their public market equivalent returns, and S&P 500 returns between 1994 and 2017 using data from the investment consultancy Cambridge Associates.

- Private equity returns outperformed their public market equivalents between 1994 and 2005, but not much thereafter. The average alpha fell from 8.9% to 1.5% per annum. As the private equity industry matured and its AUM ballooned to more than $3 trillion, generating alpha apparently became much more challenging.

- Since 1994, neither private equity nor public market equivalent returns were negative on an annual basis. The S&P 500, by contrast, had four down years. Private equity’s combination of high absolute returns and no bear markets is unique and would provide attractive diversification benefits to a traditional equity-bond portfolio and explains why investors have grown so fond of the asset class.

Private Equity IRRs vs. Public Market Returns

But just how accurate is the private equity returns data?

An investor who allocates to a US-focused private equity fund will get exposure to mainly US-based companies just as they would investing in the S&P 500. Private equity funds have no short positions, cryptocurrency holdings, or land on Mars that would offer true diversification. Investing in private equity is simply a long-only bet on a portfolio of companies.

So it is curious that US private equity funds generated an 11% IRR in 2008 when the global economy was hemorrhaging and the S&P 500 fell 38%. The public market equivalent return was 14%, which is equally difficult to explain.

Since there are no better alternatives, we will sin a little and compare IRRs and public market returns. After all, private equity allocations are often made based on such data.

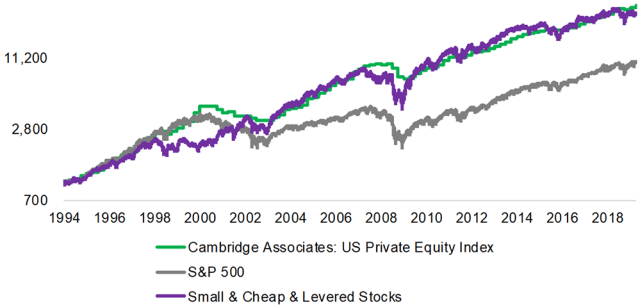

Replicating Private Equity Returns

The returns of US private equity funds can be replicated efficiently with public equities. Private equity companies have historically targeted small and undervalued firms that could be leveraged.

We can rank stocks according to these characteristics and construct an index that closely tracks the US Private Equity Index’s performance based on quarterly IRRs. Naturally, this replication index provides daily liquidity and full transparency. And would presumably have low fees. All of which is preferable to locking up capital for years and paying high management fees.

Replicating Private Equity Returns in the United States

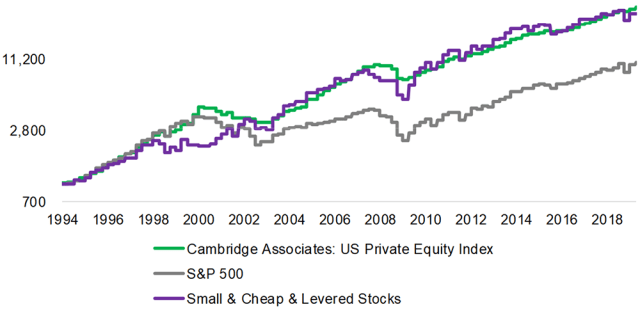

Adopting Private Equity Reporting for Public Equities

Although private equity returns can be replicated, the replication index composed of small, cheap, and levered stocks shows much more volatility than the US Private Equity Index. Naturally, this is partly because private equity firms report performance on a quarterly basis. However, there is no reason, other than intrinsic self interest, why private equity firms cannot provide daily valuations for portfolio companies using public market multiples.

Alternatively, investors could follow public market performance on a quarterly basis, which would smooth the reporting differences relative to private equity. The law requires that most investment products like mutual funds report daily net asset values, though it is up to investors how to deal with them.

Adopting Private Equity Reporting for Public Equities

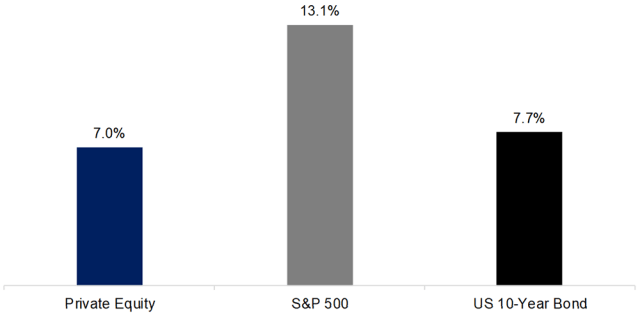

Private Equity Volatility

Private equity’s appeal is obvious. It has generated high returns along with low volatility, which results in high risk-adjusted returns. But the volatility of the US Private Equity index was almost 50% lower than the S&P 500’s and even below that of the 10-year US government bond.

Yet private equity funds represent equity positions in corporates. Hence this low volatility must be artificial, the product of smoothed valuations. Private equity portfolio companies are influenced by the economic tides just as much as public companies, even if they don’t want this reflected in their valuations.

Private Equity vs. Equity and Bond Market Volatility, 1994–2019

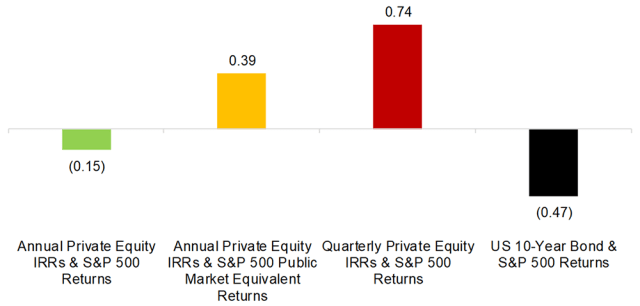

Private Equity Correlations

So private equity returns are probably exaggerated and their volatility understated. That adds up to less appealing risk-adjusted returns than advertised. But maybe private equity and public market returns are uncorrelated. Perhaps the asset class offers real diversification benefits.

The correlation is negative based on annual IRRs and S&P 500 returns. So a private equity allocation makes sense in an equity-bond portfolio. But use public market equivalent returns or quarterly data, and the correlation becomes positive and elevated. Since private equity represents a bet on the equity of a diversified portfolio of corporates, this is not totally unexpected.

In comparison, bonds were negatively correlated to equities from 1994 to 2019 and so offered better diversification.

Private Equity Correlations to Equities, 1994–2019

Further Thoughts

Private equity firms serve a useful policing function in the financial markets: They identify poorly run companies, acquire, improve, and ultimately sell them. This strategy has merit and has generated attractive returns over the last couple of decades.

But that track record was fueled in part by increasing valuation multiples and falling financing costs. Such favorable tailwinds can’t be counted on going forward. Multiples tend to mean-revert and interest rates can hardly fall much further.

Even worse, with fewer potential targets and increasing AUM, most private equity firms have drifted away from the original “buy it, fix it, sell it” business model. In 2018, of all the private equity-backed businesses that were exited, 48% were taken over by other private equity firms. Which raises questions as to what more can be improved upon at the company level.

While private equity’s siren song — “uncorrelated returns” — is hard to resist, investors should be looking forward rather than backward.

For more insights from Nicolas Rabener and the FactorResearch team, sign up for their email newsletter.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images/Lawrence Manning

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.