[ad_1]

It is sometimes quipped that Europe is built on crises. And, yes, the COVID-19 pandemic, following on the heels of Brexit, proved powerful enough to break the taboo on the creation of a long overdue pan-European fiscal policy.

This is in line with our prediction that when faced with severe crisis, the EU would take bold steps towards establishing a common bond to finance a fiscal expansion at the center. Our other prediction — that a safe asset would be created that eurozone banks could invest in, in lieu of risky national sovereign bonds, to reduce the economy’s sensitivity to adverse macroeconomic shocks — has not come true. It may still happen, but perhaps only after another major crisis.

The Recent Package

On 21 July 2020, the European Council adopted a €750 billion measure — equal to around 6.5% of GDP — to fund governments in pandemic-induced distress. Composed of €390 billion in grants and €360 billion in soft loans, the package is financed based on the issuance of EU bonds against the EU budget, with a slight increase in the latter funding the debt servicing.

This initiative came roughly three months after the European Council adopted a €540-billion package — the equivalent of around 4.5% of GDP. This included €100 billion for a European unemployment fund (“SURE”), €200 billion in loans to small- and mid-sized enterprises (SMEs) from the European Investment Bank (EIB), and a €240-billion credit line for distressed governments made available by the European Stability Mechanism (ESM).

This, in turn, came on top of massive national fiscal stimulus, with spending and revenue measures equivalent to 5% of GDP in Germany and 2% in Italy and France. The lending programs add up to 30% of GDP in Germany and Italy and 15% in France. Loans are below the line, so do not affect the deficit but do affect debt.

The fiscal stimulus is robust and will certainly help contain the downturn in the wake of the pandemic. But it adds massive debt both at the national and central levels. Moreover, while it may carry its recipients through the first stages of the crisis, it will burden them with EU loans and add to their market debt, which is probably already unsustainable.

Debt will need to be repaid, and the €2.5-trillion question is when, how, and at what cost.

The menu of possibilities is limited. We envision three potential scenarios.

Scenario 1: Fiscal Austerity

The “standard” outcome in the EU is that the fiscal rules — which are temporarily on hold since the “general escape clause” was invoked in March — will kick back in. That will require member states to adopt severe fiscal austerity for many years. That implies persistent economic headwinds and potentially prolonged European economic stagnation.

Some of the most hard-hit EU member states will probably default rather than endure the stigma and potential electoral fallout of accepting a strings-attached ESM rescue program.

Banks hold much of the debt. They will face balance sheet problems and may lose market funding. Conversely, national sovereigns may have to come to their rescue. That will weaken their position further and could lead to a reprise of the sovereign-banks doom loop that heralded the previous euro crisis. The European Central Bank (ECB) can only step in through targeted bond purchases (OMT) if a country requests an ESM program, which looks unlikely given the politics. In fact, even “standard” quantitative easing (QE), allocated across issuers of sovereign debt according to the country’s share of GDP, would not pass muster with the German Constitutional Court.

This fiscal austerity scenario will undermine whatever public support is left for the European project. Which makes it a distinctly unappealing option for most European leaders, especially in view of the Brexit debacle. Indeed, such a scenario could prompt the euro’s demise. If Italy or another country leaves, it is hard to see how it survives.

The fall of the euro would be a cataclysmic black swan event, one that could catalyze another catastrophe: the gradual unraveling of the EU and the redrawing of the geopolitical map. That would reflect a world where globalization has ground to a halt and gone into reverse.

Such a realignment could mean a new Iron Curtain. The nations of Western Europe would remain in the US orbit while their eastern counterparts would be drawn into some other sphere of influence. What would that mean for the US role in the world or its system of overseas alliances? For risk assets globally, the outlook would be bearish.

Against this backdrop, sovereign spreads could potentially increase on the back of a rout in peripheral debt amid unforgiving bond markets. The VIX may spike and euro-denominated equities, banks in particular, could plunge given how much national sovereign debt they hold.

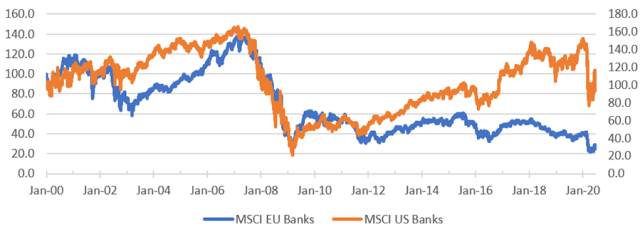

This would prolong the outperformance of US banks over their EU peers, which as demonstrated in the chart below, started to take root during the European sovereign debt crisis. Hints of a reversal only emerged amid the COVID-19 pandemic and growing hope that the EU would form some sort of fiscal union.

EU vs. US Banks: Relative Performance

US Treasuries will no doubt serve as a safe haven for a while. Of course, they offer little return and how long can they provide protection if the US Federal Reserve keeps on monetizing deficits? Since the euro is by far the largest constituent of the DXY index, which measures dollar strength, the DXY will continue its upward trend and the recent euro appreciation will prove short-lived. A strong dollar has bearish implications for developing economies and could lead to a dramatic selloff of currencies, bonds, and equities in fragile twin deficit countries like South Africa, Turkey, Argentina, Brazil, and potentially India. Gold has a strong negative correlation to the DXY so would likely trend down.

The perils of this scenario are clear. Which explains why German chancellor Angela Merkel and French president Emmanuel Macron are pushing new pan-European fiscal stimulus. But the plans as conceived won’t be enough so long as austerity hangs like a sword of Damocles over the economy’s head.

Scenario 2: Mutualization

So what can be done instead? The EU could buy most of the national debt, financing the purchase through the massive issuance of additional joint bonds. This is essentially the safe asset proposal we suggested in the spring.

The safe asset could be swapped for national sovereigns on the balance sheets of the banks and the ECB. The latter could commit to granting exclusive eligibility to the joint bond as collateral for repos as well as its asset purchases. This would effectively nip the doom loop in the bud, particularly since the joint budgets of the member states and the ECB would serve as deep-pocketed backstops.

How the financial markets would respond to this scenario is a blueprint of what we envisioned. The euro will appreciate relative to the dollar because mutualization addresses most of the structural flaws of the current monetary union without a fiscal union. Spreads would converge as yields on peripheral debt will fall at first and markets recognize that all of Europe is on the hook if one country fails.

In the long term, national sovereign yields across Europe would probably rise somewhat but remain low. European equity markets would outperform their US counterparts in the short and possibly long term. Financials in particular should benefit as yield curves steepen. The euro will improve its status as a reserve currency. If the Fed keeps on monetizing its deficits, the price of gold will hold up and maybe even reach new highs, demonstrating the negative correlation between it and the DXY.

Scenario 3: Monetization

If mutualization proves politically unacceptable and austerity becomes the default scenario, the only remaining option is the monetization of national and potentially EU debt by the ECB. The ECB would purchase the bulk of the debt and then cancel most of it.

While this would indicate a nominal accounting loss for the ECB, in reality it’s really just the permanent swap of securities for legal tender, or helicopter money by a different name.

Debt monetization could save Europe’s ailing banking system and reduce spreads between Italy and Germany. But it would do little to address more fundamental problems. The question underlying this policy is whether loans will eventually reach the SMEs and corporates that need them the most. These policies will do very little to help the real economy in the long run. Quite the contrary. It is a poorly concealed attempt to avoid the inevitable: Either Europe comes together and forms a United States of Europe fiscal union or abandons the euro all together.

Under such an either / or scenario, the long-term implications for financial markets will be much more binary. If Europe abandons the common currency, austerity will be the order of the day. If it become a federal state with central fiscal capacity, financial markets will rerate according to our mutualization scenario. But that could be years away, and until it happens, yield spreads between bunds and BTPs will likely hover around current levels or compress slightly. That’s assuming the moral hazard argument is abandoned, at least temporarily, and the ECB buys more peripheral debt than capital key rules previously allowed.

Initially, monetization should be (marginally) positive for equity markets. Taking a page from the Fed, the ECB will act as a lender of last resort, flood the market with liquidity, and monetize whatever shortfall needs to be funded. We wouldn’t expect EU equities to outperform their US counterparts. The Fed isn’t likely to turn off the printing presses and both central banks will continue their historically unprecedented practice of creating liquidity out of thin air.

Therefore, as the ultimate hard currency, gold should set new highs on the back of surging demand. In a worst-case scenario, people might start to question the “store of value” principle, which would only strengthen the case for non-cash alternatives such as gold, certain real assets, and possibly cryptocurrencies. The long-term outcome could be ugly.

Wrapping Up

To be sure, fiscal austerity on the order of 20% of GDP is highly unlikely. The more probable outcome is a blend of the three scenarios, although the weights are hard to call at this stage. What would such an outcome augur for the markets?

We expect the future to be weighed more toward mutualization and monetization than austerity and for markets to focus on the positives. Under such a blended scenario, the euro’s small rally of late should gather a bit more steam.

European sovereign debt markets should remain fairly sanguine, provided austerity measures are kept to a minimum. Yield spreads will likely hover near current levels and possibly compress a bit but shouldn’t rise to or exceed the highs set earlier in the year, although national sovereign curves might steepen somewhat.

Assuming economies begin to normalize in a post–COVID-19 world, European equity markets should continue to recover. Domestic industries and exporters, particularly intra-euro exporters, should benefit the most given how the expected appreciation of the euro will help overseas exporters and boost internal demand.

Furthermore, European companies will “onshore” more production and manufacturing activity from facilities in Asia and elsewhere. What this means for EU equities relative to US ones is contingent on many external factors. But, if further integration continues apace and Europe implements structural reforms, cuts much of the red tape in the system, and makes progress towards more of a fiscal union, EU equities could outperform by a significant margin, especially if the US debt addiction eventually hits rock bottom.

Gold prices should hold up as well under this scenario. Why? Mainly because the major central banks — primarily the Fed — will continue to monetize their deficits for a long time to come.

All in all, this blended scenario is a watered-down version of what is needed to safeguard the euro and the EU at large. Nevertheless, it constitutes a big step forward from where the old continent was only a few months ago.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

The views, opinions, and assumptions expressed in this paper are solely those of the author and do not reflect the official policy or views of JLP, its subsidiaries, or affiliates.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Nastco

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.