[ad_1]

Retirement planning is the primary objective of retail investors. Indeed, 47% of respondents in the 2022 CFA Institute Investor Trust Study indicated saving for retirement was their most important investment goal.

Yet the conventional pathway to retirement savings — the traditional stock and bond portfolio — is not as effective as it used to be. Weaker diversification, declining real returns, and rising inflation all present major challenges to both defined benefit and defined contribution (DC) pension funds. As funds struggle to meet their return targets, investors are demanding they provide access to new and potentially riskier products. Fund managers must weigh these demands in the context of their fiduciary duty, or duty of care, obligations.

With these challenges in mind, for better or worse — or at least until regulators weigh in — many pension funds are exploring allocations to cryptoassets.

So, what does that mean for the future of trust in the financial services industry?

Slower wage growth, an aging population, and lower investment returns have all been identified by the Mercer CFA Institute Global Pension Index as critical threats to the future sustainability of pension funds. Asset owners know the headwinds they face: Only a small percentage believe they are very likely to reach their annual return target over the next several years.

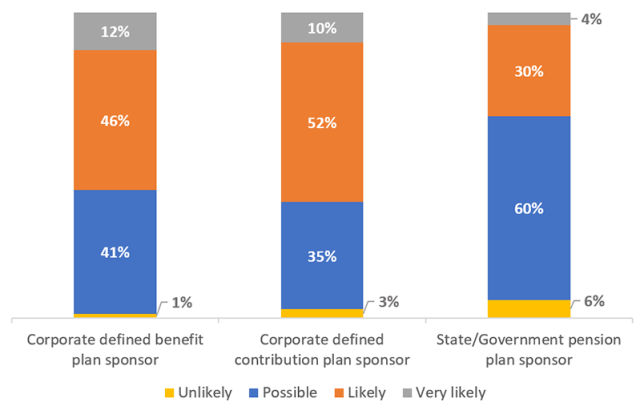

How Likely Is It That You Will Attain Your Current Target Return over the Next Three Years?

That means benefit cuts are not off the table. Of corporate and state-sponsored defined benefit plans, 60% say it is likely or very likely that they will need to adjust benefits downward within the next 10 years.

Plan participants depend on retirement fund payouts. That pension funds may reduce their expected outlays creates a deferred trust deficit, one that could undermine faith in the whole retirement funding system.

To address the potential return shortfall and cover unfunded liabilities, pension funds have branched out into digital assets and their supporting infrastructure. According to the trust survey, 94% of state and government pension plan sponsors said they invest in cryptocurrencies, along with 62% of corporate defined benefit plans and 48% of corporate DC plans.

The crypto market has had a turbulent history, particularly of late. Volatility has been the norm, with soaring peaks giving way to extreme drawdowns and vice versa.

When crypto was near its all-time heights, studies showed that a small allocation to digital assets as part of a diversified portfolio could increase returns, improve the Sharpe ratio, and lower the portfolio’s maximum drawdown. Of course, amid the latest crypto downturn, such conclusions may no longer be operable.

Mindful of the risk of direct investments in digital assets, such funds as CalPERS and CDPQ have allocated capital to crypto-adjacent assets, seeking to capitalize on the popular momentum around cryptocurrencies and the potential of blockchain technology while avoiding the day-to-day volatility of direct crypto investment.

DC plans have also dipped their toes into the space. Fidelity Investments plan participants will be able to invest as much as 20% of their portfolios in cryptocurrencies.

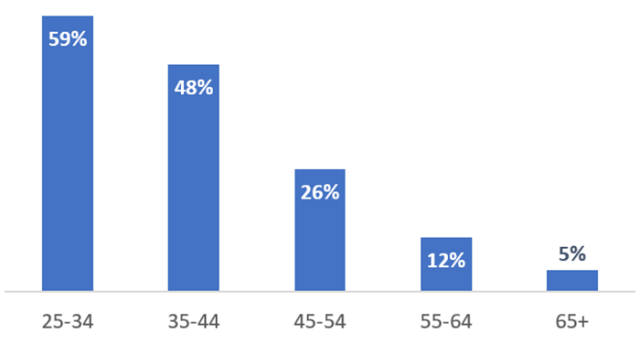

So, what does crypto demand look like? It skews toward younger investors, with 59% of those between the ages of 25 and 34 saying they currently own cryptocurrencies. As digital natives become a larger share of plan participants and hold more assets, pressure on plan sponsors to provide access to digital products will only increase.

Percentage of Those Investing in Cryptocurrencies by Age Group

But skepticism about expanding access to cryptocurrencies and derivative products is widespread. The US Department of Labor registered its ambivalence in response to Fidelity’s inclusion of cryptocurrency in its 401(k) offerings, stating:

“The assets held in retirement plans, such as 401(k) plans, are essential to financial security in old age — covering living expenses, medical bills and so much more — and must be carefully protected. That’s why plan fiduciaries, including plan sponsors and investment managers, have a strong legal obligation under the Employee Retirement Income Security Act to protect retirement savings.”

Warren Buffett, meanwhile, has described cryptocurrencies as speculative assets and predicted “cryptocurrencies will come to bad endings.”

Pension funds face an unenviable choice: chase higher returns (and more volatility) or underdeliver on performance. Fund inflows are not matching projected outflows, and plan participants have a growing appetite for new, alternative investment products. So, how can the industry respond to these challenges and maintain client trust?

Pension plan sponsors want to adopt new products early. Indeed, 88% stated as much in the trust survey. But if those products are unregulated and their long-term performance is unknown, plan sponsors must evaluate if they can be safely incorporated into portfolios without jeopardizing the trust of plan participants or the viability of their retirement savings.

As fiduciaries, pension plans must take the long-term view on investment growth and carefully consider and responsibly manage any allocation to new asset classes. They must communicate to plan participants the risks associated with these new asset classes, crypto among them, to ensure the investments align with client goals.

To continue to grow investor trust in financial services, retirement planning must be supported by robust due diligence. Pension funds and their participants must understand and believe in the products they are investing in. Without that standard, the trust deficit will only widen.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images/Who_I_am

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.