[ad_1]

Growing up on a cattle ranch in central Texas, I developed a certain respect for the tools of the trade. Horses, tractors, trucks, trailers, bailing wire, and duct tape were all daily-use items for us.

Each tool has its purpose, of course, and each tool has advantages and disadvantages for a particular job. Take, for example, the contrast between horses and tractors.

As you might well imagine, you can get quite a lot done with a tractor. You can plow a field, fix fences, haul hay. But the best thing about a tractor is that you can get up every morning and turn it on, do your work, come home, and turn it off. So long as it has fuel, it will do what you tell it to do.

You can also get a lot done with a horse. Horses have different advantages, like getting to those hard-to-reach places on your land. Their agility makes them particularly good at herding other animals. But horses are bigger and stronger than we are and unlike tractors, they have a mind of their own. If you wake up to a horse who has decided she isn’t going to work today, there really isn’t much you can do about it!

One of the biggest mistakes I see investors make — especially professional investors — is to treat financial markets like tractors. They expect to wake up every day to a reliable and consistent tool that helps them achieve their financial goals. “So long as we keep this tractor well-oiled, maintained, and full of diesel,” the thinking goes, “it’ll keep moving us closer to our goal.”

But

in my experience, financial markets are much more like horses. They have a mind

of their own and they are bigger and stronger than we are! Sure you can get a

lot done with markets, but there are some days they would just as soon buck you

off as get your work done.

To be fair to my professional colleagues, economic theory presents financial markets as though they are tractors. By reducing the world to equations, it is easy to be trapped into thinking that markets are the equation — x goes in, y reliably comes out. Equations may help us better understand the relationships between variables, but they get us no closer to controlling the mind of the market. At best, all of our economic equations are a bridle to a powerful horse — useful and helpful, but not the final word.

And as anyone who has spent time around horses will tell you: Always treat a powerful horse with respect — bridled or not.

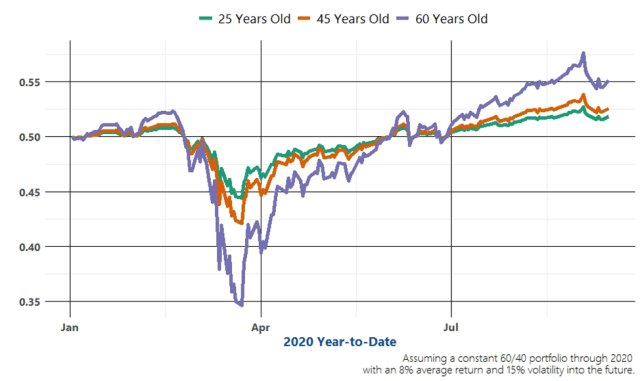

The year 2020 is a perfect example. The volatility of a traditional 60% stock, 40% bond portfolio has been about double the longer-run average. For folks within a few years of their goal, 2020 has driven wild swings in their ability to achieve it. As you can see from the following chart, a 60-year old has seen their probability of reaching retirement swing between 56% and 35% — almost 21 percentage points! By contrast, a 25-year old has seen theirs swing by only about five percentage points through 2020.

Probability of Goal Achievement by Age

The same market and portfolio yields vastly different outcomes in the lives of different people with different goals.

This is, of course, the effect for which glide-path portfolios attempt to compensate. Glide-path portfolios, however, are a tangential way to manage this very real risk. Rather than directly address the risk of failing to achieve a goal, glide-path funds sacrifice more and more return to mute volatility as a goal approaches.

That is like buying smaller and smaller horses as you grow older. Sure they may not kick as hard, but they also do considerably less work.

Rather than “sort of” deal with the risk we care about, why not address it head on? It would seem better to account for the specific variables inherent in each goal — current wealth, time horizon, and required wealth — and couple that with some market technique. Depending on individual goal parameters, risk controls may be an effective way to improve the chances of attaining our goals.

I can, at this moment, hear my “markets-are-tractors” colleagues mumbling that downside risk controls yield underperformance relative to a benchmark. That may very well be true. But “beating the benchmark” is not the objective of goals-based investors — achieving their financial goals is. In that context, downside risk controls may not just be a psychological comfort, they may be mathematically rational.

In the end, investors of all stripes would do well to move away from the image of markets as an always-cooperative tool that does what we need when we need it. As Jean L.P. Brunel, CFA, once pointed out, there are precious few institutional investors large enough to be genuine price-makers. The rest of us must be content as price-takers.

That means markets are much more like horses than they are tractors: They are bigger and stronger than we are and if they decide to kick us in the teeth one day, all we can really do is get out of the way.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Gail Shotlander

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.