[ad_1]

As ever more capital is allocated to private equity (PE), pundits and practitioners attribute PE’s success to extraordinary performance.

That premise is difficult to corroborate.

The purpose of the four-part Myths of Private Equity Performance series is to debunk the most prevalent fables surrounding the PE industry and its supposed accomplishments.

Myth I: Performance Reporting Is Reliable

The mythography of outstanding results from PE fund managers originates in the twilight zone of performance reporting. As an underregulated, loosely-supervised segment of the asset management industry, private equity is enshrined in secrecy.

Any marketeer knows that to attract customers it helps to mythicize a product’s values and benefits. Consumerism gained mass appeal once advertisers adopted standard manipulative techniques to influence behaviors and encourage emotional purchases. Promoters of sophisticated financial products follow the same rules around communication, differentiation, segmentation, and positioning, but the complexity of these products gives salespeople more scope to lure and potentially even dupe prospective buyers.

The internal rate of return (IRR) is PE’s key performance indicator and measures the annualized yield achieved over the holding period of an investment.

There are two reasons why the IRR is not a reliable yardstick:

1. IRRs can be fabricated.

Throughout the life of a fund, managers themselves determine rates of return. Only once the fund is fully realized can the IRR be labeled “final.” Typically, the IRR is only known for sure after more than a decade of investing. Indeed, Palico research from April 2016 indicates that almost 85% of PE firms fail to return capital to their investors within the contractual 10-year limit.1

Until it is fully exited, a fund will report what’s called an interim IRR, or an annualized return that includes “realized” and “unrealized” results.

Once an investment holding has been sold or exited, that particular asset’s IRR is deemed realized. In some cases, such as public listings or disposals of a minority stake in the business, the relevant IRR can be treated as partially realized.

Inversely, assets still held in a portfolio have an unrealized IRR. This is calculated by fund managers using data from public peers. As such, fund managers can easily manipulate the unrealized IRR and artificially inflate its value by, for example, choosing richly priced or even overrated comparables.

Most advocates of the current practice contend that evidence does suggest IRR calculations are fairly accurate. That IRR numbers are audited is usually their first argument. But valuation is not a science, it is a judgment. It is very easy for fund managers to come up with numbers that suggest better underlying performance than is justified by fundamentals just as they can currently fudge EBITDA numbers for their portfolio companies by applying addbacks. No external auditor can assertively challenge the fund managers’ views of their portfolios.

More explicitly, information released by PE fund managers is rarely, if ever, “independently” audited. Their accounts are reviewed by accountancy firms that can earn advisory and due diligence fees from the same fund managers’ portfolio companies. There are obvious conflicts of interest.

Data released by PE firms have, occasionally, been independently critiqued. In May 1989, for example, a Brookings Institution analyst testified before the Subcommittee of the House of Representatives following his review of a KKR study on that firm’s performance. The transcript of the hearing is quite entertaining, diplomatically highlighting “methodological problems,” “conflicting data,” and the need for adjustments in KKR’s report. The analyst also pointed out that the samples reviewed by KKR are small, which is a common issue in an industry that releases data on a sporadic and inconstant basis.

Other than auditors, a more independent category of critics has looked at interim IRR data. Scholars have researched the risk of overstatement. For instance, Stephen N. Kaplan and Antoinette Schoar reported a correlation of 0.89 between the final IRR and the interim IRR for a large sample of PE funds.2 Their results suggest that the interim performance of a mature PE fund is a valid proxy of final performance.

Yet, most academic research on PE suffers from two major shortcomings. First, it depends on voluntary disclosure by fund managers. So there is an obvious bias to the available data. Only in rare instances is disclosure the result of regulatory requirements, as in the states of California, Oregon, and Washington.

Second, the data set is usually a tiny sample of the total PE firm and fund universe. There is an implicit risk that the information is not representative of the whole population. Most researchers openly acknowledge that shortcoming. They need to go a step further and acknowledge that an incomplete or non-representative data set may discredit some, if not most, of their findings. The acronym GIGO — garbage in, garbage out — comes to mind.

To be clear, the reliability deficit is not specific to academic research on private equity. Few consultants, pundits, or journalists realize that data from most industry research firms is self-reported. If university students were asked to voluntarily submit their grades to prospective recruiters, who would be more likely to do so, the best students or the worst?

Another issue that applies to the academic research referenced above: From a practitioner’s standpoint, the correlation is probably meaningless. Let’s assume that a fund manager provides prospective investors, or limited partners (LPs), with an interim IRR of 11%. But the fund manager knows that the final number will be closer to 8%, which ends up being the fully realized return. That might still generate a high correlation factor that appears academically relevant. Yet many prospective investors might well have walked away if they had known 8% was the more realistic figure. The interim number of 11% did the trick from the fund manager’s standpoint: It fooled enough prospective LPs into investing.

The long delay in getting genuinely final and fully realized IRR numbers gives PE fund managers a fantastic opportunity to fudge interim numbers while raising subsequent vintage funds that might turn out to confirm, or not, a fund manager’s performance.

2. IRRs can be manipulated.

A much bigger issue with the IRR is that its reliance on the time value of money (TVM) makes it very easy to doctor.

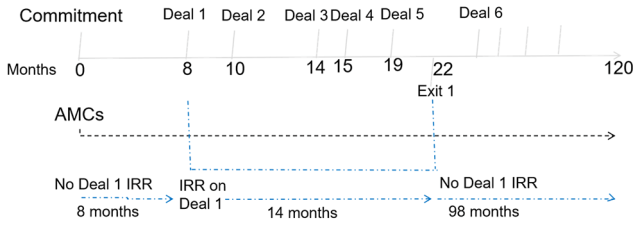

“When you commit the money [to private equity firms] they don’t take the money, but you pay a fee on the money that you’ve committed . . . you really have to have that money to come up with at any time. And of course, it makes their return look better, if you sit there for a long time in Treasury bills, which you have to hold, because they can call you up and demand the money, and they don’t count that [in their IRR calculations].”

The following chart depicts the phenomenon Buffett described:

The IRR for Deal 1 will only include the holding period running from Month 8 to Month 22. It will not take into account the likely lower returns achieved by LPs prior to that investment.

If LP investors are charged annual management commissions (AMCs) to commit their capital for a period of 10 years, shouldn’t the IRR prior to any LBO transaction, at which point the capital call takes place, be included to show the true performance of private equity? Buffett argues that it should.

There are more disingenuous ways to play with the TVM and manipulate returns. For instance, fund managers can delay the moment when they will draw down commitments from their LPs. The subscription credit line has become an especially popular instrument in this regard. It allows fund managers to temporarily borrow money from a bank in order to delay calling funds from LPs and delay the moment when the clock starts ticking from an IRR calculation standpoint. In some instances, these credit lines can remain in use for months and potentially artificially boost IRRs by several basis points.

Alternatively, a fund manager can accelerate the upstreaming of proceeds to their LPs by carrying out partial or full realizations. Many PE firms have become experts at quick flips and repeat dividend recapitalizations.

One way to standardize reporting would be to adopt the Global Investment Performance Standards (GIPS) from CFA Institute. This set of voluntary ethical guidelines encourages full disclosure and fair representation of investment performance to promote performance transparency and “enable investors to directly compare one firm’s track record with another firm’s record.”

Post-Truth Reporting

Subscription credit lines, quick flips, and dividend recaps are fantastic methods to boost returns without improving the fundamentals of the underlying assets. Slowly and imperceptibly, private equity has entered a world of post-truth performance and revealed that its rainmakers can be as manipulative as they are dogmatic.

Even if fund managers called it straight every time, assessing value creation is far from an exact science. One 2016 report from INSEAD Business School and consultants Duff & Phelps is honest enough to admit:

“the vast majority of studies leaves large residual values [of PE’s value creation process] unaccounted for and tends to employ simplifying assumptions in order to assess large datasets and populate incomplete transaction information.”

In conclusion, meshing realized and unrealized data blends into one single number the real returns achieved from selling an investee together with the fabricated returns of remaining portfolio assets. And IRRs can be massaged further by delaying cash outflows and accelerating cash inflows. This all makes any analysis of PE performance by prospective investors and academics almost nonsensical.

“In space, no one can hear you scream.” This catchphrase from the motion picture Alien can be refashioned and applied to the veil of trade secrecy, embroidered as it is with the magic of financial expertise, that shrouds private equity performance:

“In private markets, no one can figure out your true performance.”

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

1 Data is based on an analysis of 200 private equity funds dissolved in 2015. Partial years are rounded to the nearest whole year.

2 Mentioned in “The Performance of Private Equity Funds: Does Diversification Matter?” by Ulrich Lossen.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Photographed by MR.ANUJAK JAIMOOK

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.