[ad_1]

Advanced economies started cooling off about 50 years ago. Official data state it plainly. For the past two decades, most economies in North America and Europe have slowed to a crawl or stalled altogether.

Real inflation-adjusted GDP compound annual growth rates (CAGR) in the United States went from 4.2% and 4.5% on average in the 1950s and 1960s, respectively, to approximately 3.2% throughout the 1970s, 1980s, and 1990s, before dropping to 1.8% from 2000 through 2020. On a GDP-per-capita basis, the picture is even bleaker: Average CAGR dove from 3.2% in the 1960s to 1% from 2000 through 2020.

Eight years ago, former US Treasury secretary Larry Summers described the growth experienced in the years preceding the global financial crisis (GFC) as an illusion and, dusting off a phrase first coined during the Great Depression, said the country may have entered a period of “secular stagnation.”

Several factors may contribute to this plight: An aging population tends to save more and consume less; amid rising inequality, the rich also save more of their wealth rather than invest it productively; and automation puts pressure on wages, further depressing consumption.

But the causes of this lethargic growth do not concern us here. What matters is that, partly in reaction to this slowdown, capitalism had to evolve.

Variant 3: Financial Capitalism — A Deregulated Model

While there is no fulcrum moment marking the start of financialization, no clear point in time when world finance pivoted from a centralized to an uber-intermediated model, 15 August 1971 serves as a good bookend.

On that day, President Richard Nixon announced that the United States would unpeg the dollar from gold, thus undermining the Bretton Woods System. The move encouraged innovation. Synthetic derivatives were created: The Chicago Mercantile Exchange launched futures contracts written on financial instruments the following year and the Chicago Board of Trade introduced the first interest rate future contracts three years later. Arbitrage, options trading, and various other activities grew exponentially.

By 2011, the over-the-counter (OTC) and exchange-traded derivatives market amounted to almost $800 trillion. A decade later, it is presumably much larger.

Beside the conventional, if exotically named, options, swaps, forwards, and futures, slower growth helped usher in the securitization boom.

Mortgage-backed securities (MBS) were introduced by US government-backed mortgage guarantor Ginnie Mae in 1970. Soon after, investment bank Salomon Brothers created the first privately issued MBS. Securitization then penetrated the corporate bond market in the form of collateralized debt obligations (CDOs), which specialist firm Drexel Burnham Lambert developed in the 1980s.

Mass Credit Creation

A market for corporate bonds emerged in the late 19th and early 20th centuries and bumbled along for decades as a sideshow to the main event: the equity markets. That changed in the 1980s. High-yield bonds became all the rage amid the junk bond era as debt took center stage.

The securitization of commodified debt products benefited consumers, corporations, and governments. Once everybody could readily access and trade credit with few if any restraints, accumulating debt became a normal way of life.

Thanks to credit, corporations could handle the stalling US economy, introducing new growth strategies and pushing products onto consumers who could not always afford them.

With the mass commercialization of credit, debt overtook equity as the principal source of capital accumulation. Credit became a new commodity. Before long, it began to eclipse the commodity that had dominated the world economy for almost a century: oil. Amid the two global supply shocks of the 1970s, petroleum had lost much of its luster.

New Custodians of People’s Money

With world markets no longer guided by the principles of Bretton Woods, governments couldn’t coordinate strong leadership across the global economy. Many launched ambitious economic democratization programs. Markets were expected to self-regulate.

Since Reaganomics in the 1980s, laissez-faireism has become a normal economic policy. Successive US administrations have more or less conceded their inability to manage an increasingly complex, global, and debt-ridden economy. Uncontrolled money printing in the aftermath of the GFC and during the COVID-19 pandemic has reinforced that belief.

Other Western markets adopted deregulation as a default mechanism, which helped to boost growth. While the shareholder capitalism model coped well with the changes — partly compensating for economic stagnation with intensified, debt-funded M&A activity — the financial markets eventually took over.

Financial capitalism’s chief operators are banks, insurers, hedge funds, private capital firms, bond investors, traders, and retirement plan managers, among numerous other agents. These administrators of other people’s money, not the capital owners or corporate executives, are the most influential economic actors.

They secure mandates to manage, lend, and invest money within a loose set of contractual and regulatory guidelines. They prosper by amassing assets on a proprietary basis and generating proceeds from deals, extracting myriad fees from interactions with borrowers, consumers, investors, and depositors.

Under this model, wealth is transaction-based rather than primarily operational as it was in classical, industrial capitalism. Increasingly, such transactional value is magnified via the use of credit.

Credit as a Source of Wealth Accumulation

When John Maynard Keynes’s ideas were gaining traction in the 1930s, over-saving was seen as a risk that could lead to demand shortages, under-investment, and unemployment.

A natural tendency to save did not solely affect consumers. In his book Money, John Kenneth Galbraith observed that, in the past, “wise governments had always sought to balance their budget. Failure to do so had always been proof of political inadequacy.”

When consumer credit became pervasive in the post-World War II era, it extended people’s individual consumption, funding a “way of life,” in consumer society parlance — nowadays, we would say “lifestyle.” Financial intermediaries feed off that lifestyle by selling credit solutions.

Citizens are not just expected to consume. Depositors must also turn into investors, occasionally trading on margin. The more — and the more frequently — they consume and trade, the better. Consumption and investments are greater sources of fees for intermediaries than cash deposits could ever be. As the saying du jour goes: cash is trash.

For businesses, hoarding cash is not commendable either. In a system essentially submerged in debt, the primary value trigger is not reinvested profits or cash accumulation. Many corporations, especially those that are private equity-backed, frequently report accumulated losses in their accounts.

The Age of Leverage

Thanks to financial engineering, debt has leapfrogged stock issuance and retained earnings as the leading mechanism for wealth accumulation. Another trend underlines this fact: debt-fueled stock buybacks.

Public investors — activist hedge funds, in particular — exert significant pressure on corporate executives to leverage up their balance sheets to either repurchase shares or pay out special dividends. The old argument for buybacks was that holding cash is unproductive. If management has nothing to spend it on, why not return it to stockholders who will find ways to put it to good use?

Substituting debt for equity is a classic trick in PE firms’ toolkit, but publicly listed corporations have made it a common practice. Even cash-rich companies are in on it. Earlier this year, Apple raised $14 billion of bonds despite hoarding $200 billion of cash equivalents in the bank. Most of that liquidity was held abroad; Apple did not fancy paying tax on remittance. In modern capitalism, unnecessary cash leakage, such as paying taxes, is to be avoided.

Traditionally, bond issuance’s main function was to fund capital expenditure. But this relationship no longer holds. Corporate debt is used as a tool to return proceeds to shareholders, not to fund growth. Wealth accumulates outside rather than within the corporate remit.

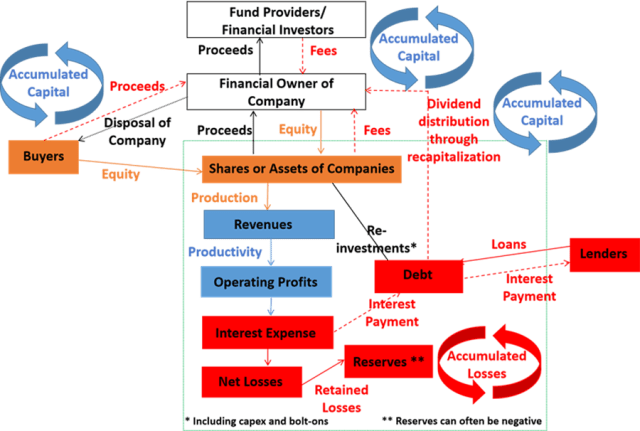

Value Creation in Private Equity

The Financial Model of Value Creation

A novel process has come to global economies since the 1970s.

- Financial markets are irrigated by two wellsprings: credit and fees.

- Significant corporate wealth accumulates exogenously, including via financial engineering, as the illustration above demonstrates, although a portion also is harvested from operational improvement.

- Accumulated capital leaks out of the company through fees, dividend distributions, and proceeds from disposals.

- Many firms also draw revenue by extracting fees from assets under management (AUM) and redistributing or restructuring assets.

- A substantial proportion of market participants, including PE firms, are short-term investors managing other people’s money. They require a much more dynamic model to accumulate capital.

- The narrow ownership time frame redirects business strategy and operational management towards more expedient methods of value enhancement. For that reason, this system is often dubbed runaway capitalism or capitalism on steroids.

- The risk of default stays within the corporate remit in the form of accumulated losses. These losses are not assumed by financial intermediaries.

This business model is a direct, if distorted, descendant of shareholder capitalism. Value is generated from transaction-based activity and routine operational improvements. Benefits do not accrue primarily to shareholders, however. The process unreasonably enriches intermediaries that levy a litany of agency fees.

In sum, wealth accumulation in financial capitalism is characterized by three elements:

- Unrestricted liquidity, heralded by deregulation.

- Ubiquitous credit: Debt is cheaper than equity — thus, it permeates all economic activity.

- Frequent transactions optimize profitability through recurrent capital gains and enduring fee generation.

Financial markets are run by credit hogs whose success depends on a transactional approach that supports faster — even if temporary — value creation. Yet the concept of maximizing long-term shareholder returns has not disappeared altogether. We will see in Part 3 that it survives in digital capitalism.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Tetra Images

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.