[ad_1]

Many US investors allocate to international equities in the belief that it diversifies portfolio risk without compromising long-term returns.

While this may have been true in decades past, the evolution of the global economy has altered the relationship between US and international stocks. Today, equity investments in many of the developed economies that dominate the MSCI EAFE and ACWI ex USA indices yield little in the way of diversification benefits.

This means investors should look critically at both their total exposure to international equities and their specific exposures to international market segments.

Defining International Diversification Down

Why do investors allocate to international stocks? Because of data like that in the chart below. Since 1970, as measured by the MSCI EAFE NR USD Index, international equities have slightly underperformed and demonstrated more volatility than their US counterparts, as measured by the MSCI USA TR Index, but a portfolio composed of 10%–60% international and 40%–90% domestic equities, rebalanced monthly, improved overall returns, risk-adjusted returns, or both.

Model Portfolios, January 1970 to June 2019, Rebalanced Monthly

Source: Bloomberg; return and volatility figures based on annualized monthly data

This is a powerful data point and a compelling argument for allocating to international stocks.

Yet this only accounts for the nearly 50-year sample period in aggregate. It does not consider the trends in returns and diversification benefits. Focus on these, and a different picture develops.

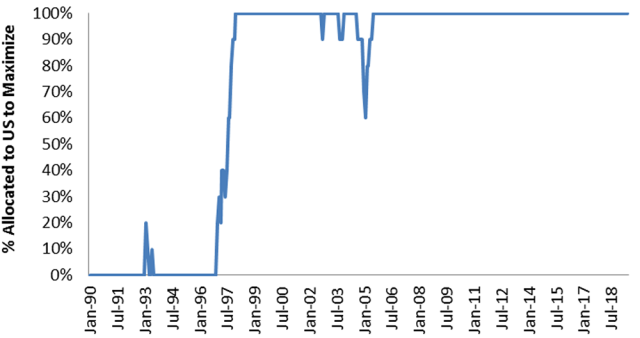

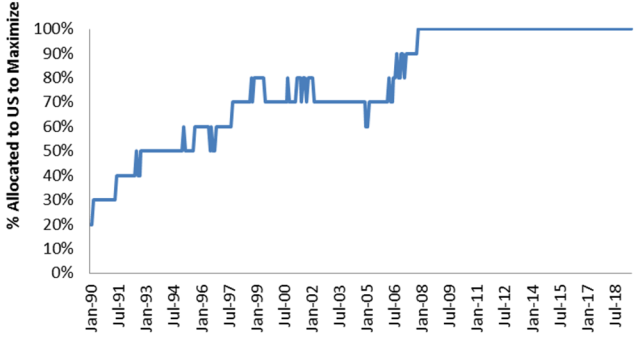

The following two charts visualize monthly rolling 20-year periods between January 1970 and June 2019. The first shows the percentage a global equity portfolio would have had to allocate to US stocks to maximize returns; the second, how much ought to have been allocated to US equities to maximize risk-adjusted returns, or annualized return divided by annualized volatility.

Percent of Global Equity Portfolio Allocated to US Equities to Maximize Returns, Rolling 20-Year Data, Rebalanced Monthly

Period Ending

Source: Bloomberg

Percent of Global Equity Portfolio Allocated to US Equities to Maximize Risk-Adjusted Returns, Rolling 20-Year Data, Rebalanced Monthly

Period Ending

Source: Bloomberg

According to the first chart, sometime in the mid‐1990s, international stocks stopped outperforming US equities and have underperformed ever since.

Investors might be willing to sacrificing some returns in order to diversify a portfolio and reduce risk. But if that is the case, the second chart presents a troubling picture.

To maximize an equity portfolio’s risk-adjusted returns, the percentage allocated to US stocks has slowly drifted toward 100%. This means that not only have international stocks lagged their US counterparts over the last several decades, but their diversification benefits have also deteriorated.

What’s Changed?

So how has the correlation between US and international markets shifted? What is the cause, and more critically, what are the asset allocation implications?

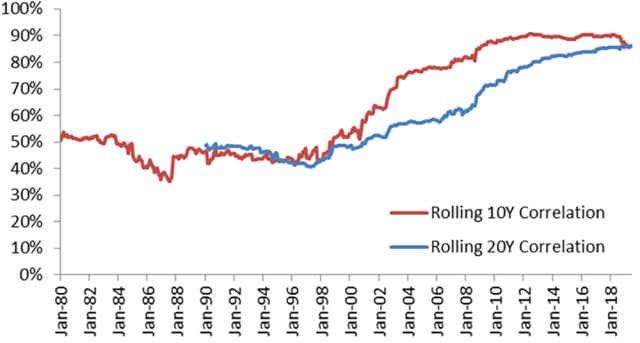

The correlation trend between the MSCI USA and MSCI EAFE over rolling 10- and 20-year periods from January 1970 to June 2019 is depicted in the chart below. It demonstrates that international equities offered a significant diversification benefit up until 1998.

Correlations between US and international equities over long-term time horizons now fall consistently between 80% and 90%.

Rolling 10- and 20-Year Correlation: MSCI USA vs. MSCI EAFE

Period Ending

Source: Bloomberg

The precise cause of this shift is difficult to pinpoint, but globalization and the internet revolution have likely played a role. And neither of these developments is likely to be dialed back. There is no returning to a pre‐1998 correlation relationship.

Furthermore, barring a profound shift in investor expectations for returns and volatility, the increased correlation between US and international equities should affect how US investors allocate to global stocks.

So how should these observations influence how we build our portfolios? Let’s look at two reasonable long-term capital market assumptions and assess the impact of increasing the correlation between US and international equities from 65%, or the long-term average since 1970, to 86%, the current 10- and 20-year correlation between the MSCI USA Index and the MSCI EAFE Index.

Long-Term Capital Management Assumptions

| Returns | Volatility | |

| International Bull

Believe international equities will earn a premium due to increased risk or valuation discount. |

US Equity Return: 7.75%

International Equity Return: 8% |

US Equity Volatility: 16%

International Equity Volatility: 18% |

| Domestic Bull

Believe international equities will not outperform US equities over time. |

US Equity Return: 7.75%

International Equity Return: 7.75% |

US Equity Volatility: 16%

International Equity Volatility: 18% |

Note: Volatility assumptions are based on long-term relationships between MSCI EAFE and MSCI USA Indices. The volatility spread between the two indices has been relatively stable over time, with EAFE exhibiting on average a 2% premium.

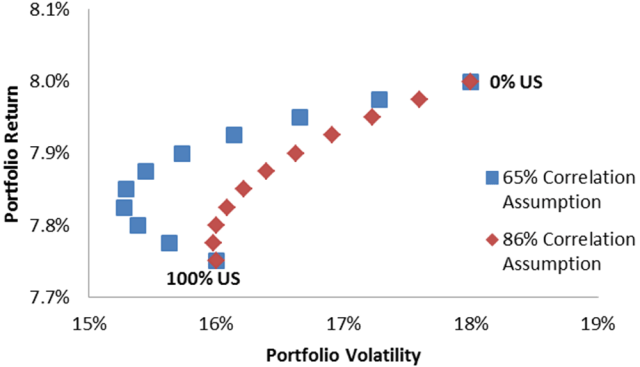

The graphic below models the International Bull scenario. Simply adjusting the correlation assumption significantly reduces the diversification benefits of international equities.

We can allocate up to 20% of our portfolio to international stocks to enhance returns without increasing volatility. From there, however, any increased international allocation is a tradeoff between risk and return. Under the old 65% correlation assumption, we could allocate up to 60% to international equities without increasing overall portfolio risk.

Efficient Frontier of Global Equity Portfolio by US Equity Allocation

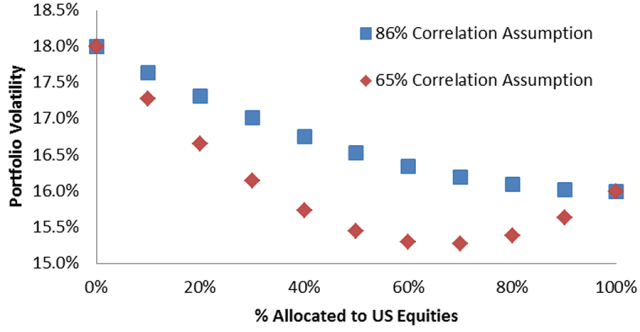

Finally, in the Domestic Bull scenario visualized below, a traditional efficient frontier may not be the best way to determine the optimal exposure to international equities.

Since both US and global stocks are expected to achieve the same return, the total international allocation should be based on how well global stocks reduce overall portfolio risk. But once again, international equities play a lesser role.

Since international equities neither enhance returns nor reduce volatility, the model recommends anywhere between a 0% and a 20% allocation to the asset class.

Volatility Profile of Global Equity Portfolio by US Equity Allocation

The Silver Lining

The evolving relationship between US and international equities means that long‐term investments in broad-based international indices add less value to a portfolio than in the past.

As a result, investors should re‐evaluate the assumptions they have made based on the long-term relationship of US and global stocks and consider adjusting their allocations accordingly.

To be sure, this analysis focuses on a broad, index-based approach to international investing. While reduced allocations to international stocks may make sense, investors should continue to seek out opportunities in niche segments of the global market to push out the efficient frontier and regain the diversification benefits that international equities once offered.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images/chaluk

Continuing Education for CFA Institute Members

Select articles are eligible for continuing education (CE) credit. Record credits easily using the CFA Institute Members App, available on iOS and Android.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.