[ad_1]

For more reading on inflation, check out Puzzles of Inflation, Money, and Debt by Thomas S. Coleman, Bryan J. Oliver, and Laurence B. Siegel from the CFA Institute Research Foundation.

As most of us in the West will take some time off at the end of the year, I want to invite you to think about your investments and what the next year and the years thereafter will bring. In particular, I want you to consider all the ways in which you could be wrong.

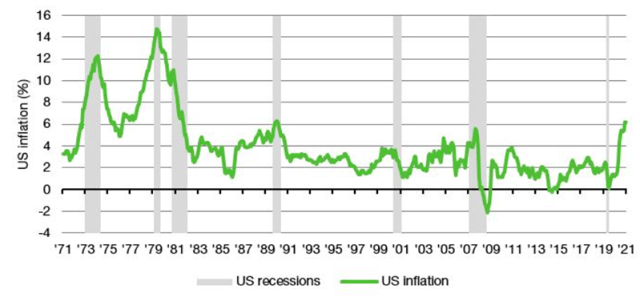

Over the last several weeks and into early January, I am going through this process professionally, as I write my big annual outlook for 2022. And one of the topics that I wrestle with is inflation. I remain in the camp of those who believe that current inflation — energy price inflation, in particular — will be transitory and decline once demand for energy falls in the spring. I am not as sanguine about inflation as the US Federal Reserve: I expect it will be higher than the Fed forecasts, but I still think inflation will decline next year and beyond.

But what if it doesn’t?

One thing I have to do is to consider what happens if inflation is not transitory. What if energy shortages and supply chain disruptions persist throughout 2022? What if higher energy prices come through in the form of higher real wages and there’s a wage-price spiral like we had in the 1970s? How would that affect my portfolio and how would I change my investments if it were to happen?

US Inflation, 1971 to 2021

And then, once I have considered all that, I do something else. I think about why the scenario I think will not happen should not happen. This is where it gets difficult. Our natural impulse is to just dismiss potential developments that contradict our pre-conceived notions without much examination. Our instinct is to hand wave and assume that things have always reverted to some sort of normal after a period of abnormal. In a sense, I believe inflation will revert to a pre-pandemic normal, while those who expect inflation to get out of control anticipate a normal reminiscent of the 1970s and 1980s.

But remember: There is no law of gravity in finance. A constant theme throughout my last three years writing about finance has been how the world has changed substantially since the global financial crisis (GFC). Things don’t work like they did in the 1980s or 1990s, let alone the 1970s.

So, I have to force myself to explain how things will work out and back it up with data, not anecdotes. And I challenge you to do the same with your opinions and expectations. Don’t make your case with anecdotes or fall into other rhetorical pitfalls, slippery slope arguments, and the like: “If we allow this to happen and don’t fight inflation now, it will entrench itself and get out of control.” You will lose credibility in my eyes and I will file your opinions in the drawer labeled “Ideologue.”

My golden rule is to only dismiss an outcome if you can show beyond a reasonable doubt why it cannot happen. If you can’t do that, consider the possibility that you will be wrong and what that might mean for your investments.

By now, many of you are smiling. Why? Because my view that inflation will be transitory is the one that receives the most pushback from investors these days. Contrary to the economists, the consensus among professional investors seems to be that the inflation picture will grow worse next year.

US Cyclically Adjusted PE Ratio (CAPE)

But here is something to ponder: If you’re convinced that inflation — and interest rates — will reverse a decades-long trend and begin a prolonged upswing, you must also believe that stock markets are significantly overvalued. Hundreds of charts, especially the cyclically adjusted PE (CAPE) ratio popularized by Robert Shiller, show how the US stock market soared into overvalued territory a long time ago.

So many investors have sounded the alarm: Current valuations are unsustainable and have to come down. That’s been their refrain for more than a decade. And they have been wrong for more than a decade.

So my question about US valuations coming down is: What if they don’t?

For more from Joachim Klement, CFA, don’t miss Risk Profiling and Tolerance and 7 Mistakes Every Investor Makes (and How to Avoid Them) and sign up for his regular commentary at Klement on Investing.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / gremlin

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.