[ad_1]

Governments around the world have deployed massive stimulus to battle the economic effects of COVID-19. And as economies reopen, there is a fear of rising consumer prices. As a result, investors, market strategists, and other market participants are increasingly thinking about the impact that inflation could have on their portfolios.

Given this environment, how can the Local Inflation factor and breakeven inflation help us understand how shifting inflation expectations might affect portfolios?

Inflation Breakevens and the Current Environment

The inflation breakeven rate gauges the market’s inflation outlook by calculating the difference between the yield of a nominal bond and that of an inflation-linked bond with the same maturity. At first approximation, the 10-year breakeven inflation rate implies what market participants expect inflation, as measured by the Consumer Price Index, will be over the next 10 years.1

During the COVID-19-induced market crash in February and March 2020, inflation breakevens fell dramatically, as the following time series plot demonstrates. Why? Probably because inflation expectations declined. But other factors, including relative liquidity differences between nominal and inflation-linked bonds, might also have been at work.

10-Year Breakeven Inflation Rate

But if breakevens are proxies for inflation expectations, they are not what they were early last spring. They have been on a prolonged upswing since mid-April thanks to the enormous pandemic-related stimulus.

The message is clear: Rising inflation is a concern.

So how in practical terms can investors manage their inflation risk?

Before addressing that question, we first need to understand the relationship between inflation breakevens and the Local Inflation factor.

The Local Inflation factor, in its raw implementation, with no residualization to other factors, attempts to capture the market’s outlook for inflation and thereby provide a hedge against inflationary risk. The raw Local Inflation factor input is the total return difference between an inflation-linked bond index and a Treasury index.

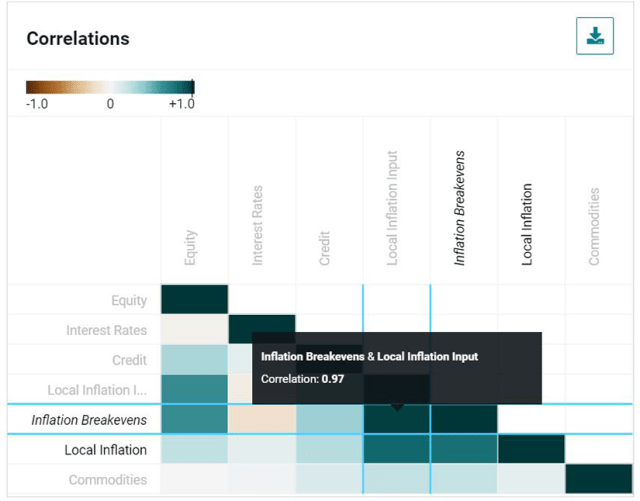

By construction, the Local Inflation factor increases when realized inflation is high relative to expectations, which can be captured by breakeven inflation. Hence, as the following chart shows, the raw Local Inflation factor has exhibited a 97% correlation with shifts in breakeven inflation over the last five years.

Correlations between Local Inflation Factor Inputs and Breakeven Inflation

Time period: 13 January 2016 to 12 January 2021, using rolling five-day returns.

However, in practice, the factor and risk analysis tool we use in our example — Venn — residualizes the less liquid Local Inflation factor to the more liquid core macro factors. Of these, three — Equity, Credit, and Commodities — also have positive correlations with breakeven inflation changes over this period. Thus, these risk factors have some inflation hedging capability embedded within them.

This offers an important lesson. When applying factor analysis to an investment or portfolio, exposure to Local Inflation as well as to the core macro factors and how they play into inflation exposure are critical considerations.

Managing Fixed-Income Portfolio Inflation Risk in Venn

So how can we manage inflation risks across a portfolio?

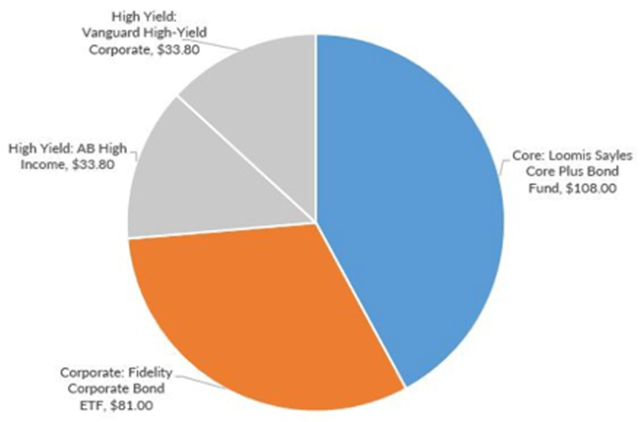

Using Venn, we’ll play the role of a fixed-income portfolio manager. In this case, our allocator wants to know how well their portfolio is hedged against inflation. Their current portfolio allocation across various fixed-income sectors and managers is as follows:

Starting Allocation of the Fixed-Income Portfolio

Of the $256.5 million portfolio, 42% is allocated to a core fixed-income fund, 32% to a corporate bond fund, and 26% split equally between two high-yield bond funds.

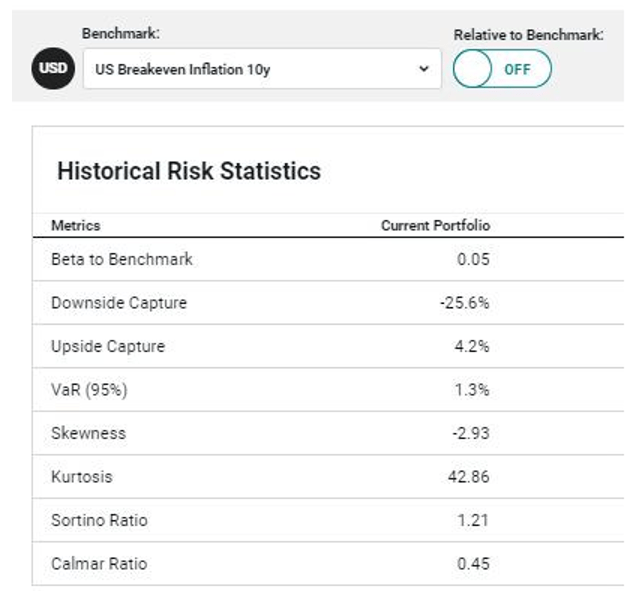

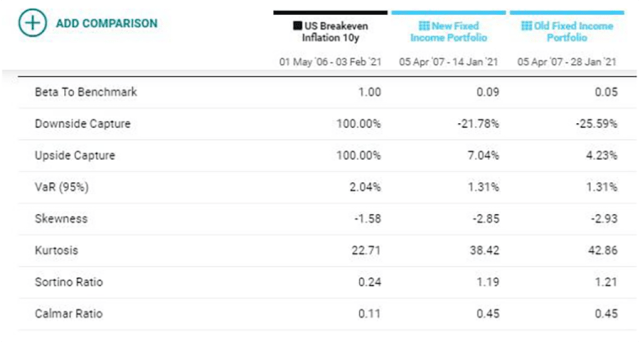

Using Venn’s Factor Analysis, we can measure the exposures to Local Inflation as well as to the core macro factors that the Local Inflation factor is residualized against. A simpler analysis might look at the portfolios univariate beta to the Bloomberg Barclays US 10 Year Breakeven Inflation Index, which, as we mentioned above, has a 97% correlation to Venn’s raw, unresidualized Local Inflation factor.

Historical Risk Statistics of the Fixed-Income Portfolio

Time period: 13 January 2016 to 12 January 12 2021, using rolling five-day returns.

The beta presented here is one way to measure a portfolio’s exposure to changes in the inflation outlook. But what does this beta actually mean?

The portfolio’s 0.05 beta indicates that if breakeven inflation goes up by 10 basis points (bps), the portfolio is forecast to return 4 bps.2 This suggests the portfolio and changing inflation expectations are positively correlated.

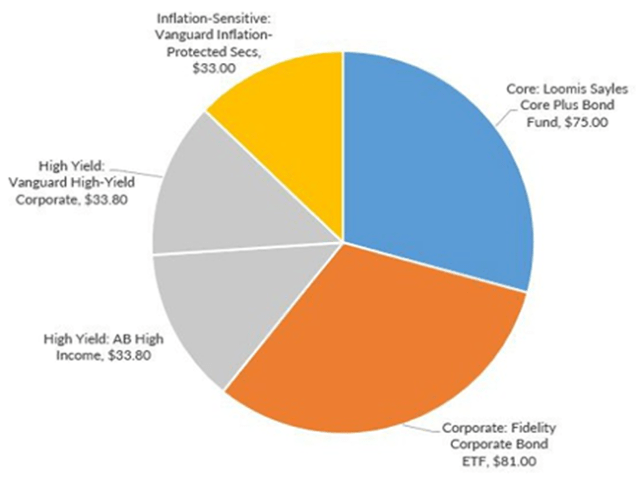

Now say as a fixed-income portfolio manager, we’re concerned about potential rising inflation and want to further hedge the portfolio against that risk. We are considering a Treasury Inflation-Protected Securities (TIPS) fund and want to see how that might shift our factor exposures and inflation sensitivity. So we test allocating to the TIPS fund by reducing the exposure to core fixed income.

Updated Allocation of the Fixed-Income Portfolio

What sort of effect did this have on the portfolio’s relationship to shifting inflation forecasts?

Historical Risk Statistics of the Updated Fixed-Income Portfolio

Time period: 13 January to 12 January 2021, using rolling five-day returns. The Bloomberg Barclays US 10 Year Breakeven Inflation Index is the benchmark.

The updated portfolio is more sensitive to inflation expectations, which suggests it is better hedged against rising inflation than the original portfolio.

From here, we can use the same process outlined above to test out other potential portfolio allocations, including to such inflation hedges as gold and natural resource equities, to see how they can further increase the portfolio’s inflation sensitivity.

No one knows what path inflation will take in the future. But investors may want to consider these steps to help them better understand just how well hedged their portfolios are against it. And if their inflation exposure is more than they are comfortable with, they can possibly take action to reduce it.

1. In theory, yield difference between nominal and inflation-linked bonds with the same maturity include more than just expected inflation. For example, it also may include an inflation risk premium. Relative liquidity differences and short-term investor demand can also affect pricing.

2. To convert from return space to yield change space, we multiply the beta by the duration. If we approximate the duration of the bonds in the TIPS and Treasuries indices as 8, then we can say that if inflation expectations go up by 10 bps, real yields will go down by 10 bps, assuming this move does not affect nominal yields, and TIPS’ return will be +80 bps. After multiplying by a beta of 0.05, the portfolio will go up by 4 bps.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image courtesy of the Gerald R. Ford Presidential Library and Museum via Wikimedia Commons

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.