[ad_1]

We live in an era of responsible and sustainable investment, with environmental, social, and governance (ESG) considerations assuming ever-increasing importance and priority in investment decision making and portfolio construction.

Between 2014 and 2018, the total value of “sustainable and responsible” investment assets in the United States grew at a compound rate of 16% per annum to $11.995 trillion, or 25.7% of all managed assets. While the societal benefits of ESG investing may seem obvious, whether socially responsible funds generate superior risk-adjusted returns compared with their conventional counterparts still has no clear answer. Some studies report evidence of a positive relationship between socially responsible investing and abnormal returns, while others report a negative relationship.

Another big question for researchers is whether the application of ESG values may lead to market inefficiencies — and therefore create the potential for abnormal returns. Previous studies have largely focused on measuring returns within short periods around the announcement of ESG-related news. Ours is the first to examine longer-run returns up to 90 days after ESG announcements.

Our investigation was motivated by other studies highlighting how large inflows into funds with high social responsibility ratings encourage institutional investors to focus relatively more on ESG characteristics of stocks than fundamentals, and how socially responsible funds are less inclined to sell stocks with high ESG ratings, even after negative news on fundamentals.

We began with the prediction that investor bias towards ESG considerations might result in overreaction to ESG-related news announcements. This prediction was grounded in salience theory, which holds that when the attention of decision makers is disproportionately directed to one or a few factors — in this case, ESG issues — those factors will receive disproportionate weighting in subsequent judgments.

We theorized that this prediction should apply particularly to ESG controversies, given that bad news tends to be more salient than good. Thus, when institutional investors observe a negative shock to the ESG attributes of a stock, we expect they will tend to overestimate the probability of further shocks, resulting in a stronger tendency to sell and a larger fall in the stock price than fundamental considerations might justify.

Our study demonstrates that the price reaction to ESG news events is more pronounced for firms with a higher institutional holding before the news release and that there is a statistically significant decrease in institutional holdings following the release of bad ESG news compared with changes after good news.

If these return patterns can be attributed to institutional investor overreaction, then we expect both the announcement returns and subsequent mean reversion to be stronger when opportunities for arbitrage are more limited. Thus, we show that the abnormal returns are stronger for smaller stocks, which have higher volatility and are harder to short sell. Further, consistent with the prediction that negative phenomena will attract more attention than positive, we also show that the overreaction is greater for bad ESG news than good ESG news.

Methods and Findings

The study focused on the constituent stocks of the S&P Composite 1500 Index in the United States. We used return data from the Center for Research in Security Prices (CRSP) and sourced information about ESG news events from RavenPack News Analytics’s Dow Jones Edition, which includes material from Dow Jones Newswires, which covers the Wall Street Journal, Barron’s, and MarketWatch. By applying filters to RavenPack’s news classification system, we were able to isolate individual events in ESG-related sub-categories. (These categories are labor issues, war conflict, security, natural disasters, pollution, industrial accidents, civil unrest, corporate responsibility, crime, and health.)

Events were categorized further — as positive or negative — using RavenPack’s news sentiment methodology. Our final sample comprised 82,435 firm-event observations between January 2000 and December 2018.

Stock returns around ESG news events were examined using the event study statistical method that often employed when assessing the impact of an event on the value of a firm. (For model specifications, refer to the main paper.) The method involves finding the abnormal return attributable to the event, adjusting for returns that stem from Carhart four factors — market risk, size, value, and momentum. To measure the returns around ESG announcements, we calculated the cumulative abnormal return (CAR) for 21 trading days centered on each news release day.

Across all firms in our sample, the study found a statistically significant cumulative abnormal return at the 0.01 level for the 21-day window of -0.773% around bad news, while the average abnormal return of -0.004% around good news was insignificant. The findings are in line with our prediction that the behavior of institutional investors would reflect their concern about fund outflows when they held stocks subject to ESG controversies.

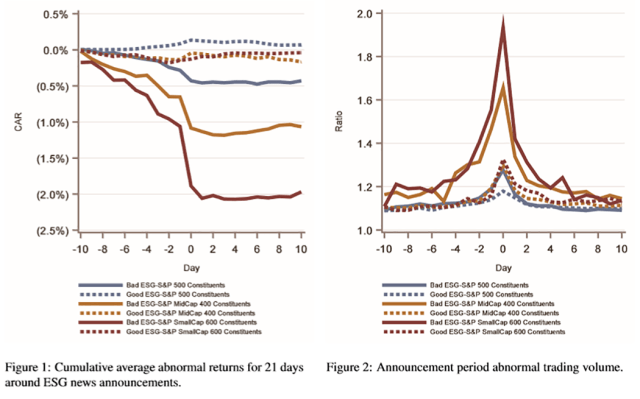

To demonstrate the return patterns around ESG news announcements, we collated cumulative average abnormal returns for 21 days across a number of categories (see Figure 1). First, we separated events into good news and bad news. Second, we categorized stocks according to size, collating separate results for firms in the S&P 500 Index.

The results show a clear negative abnormal return when firms are subject to bad ESG news, but no clear pattern around positive ESG news. The negative returns around bad ESG news are substantially larger in magnitude for the smallest stocks. There is also evidence of possible leakage of information ahead of bad news events, as cumulative abnormal returns begin occurring several days before news releases.

We also examined abnormal trading volumes from 10 days prior to the ESG news announcement to 10 days after. The results are presented in Figure 2. (The abnormal trading volume is calculated as the ratio of trading volume at day t of the trading volume averaged between day t = −255 and t = −46.)

We identified a clear increase in abnormal volumes around bad ESG news and only a small increase around positive news. The increase around bad ESG news was also more pronounced with smaller stocks and — consistent with other evidence of potential leakages of information — there was an increase in abnormal trading volumes several days before the release of bad news.

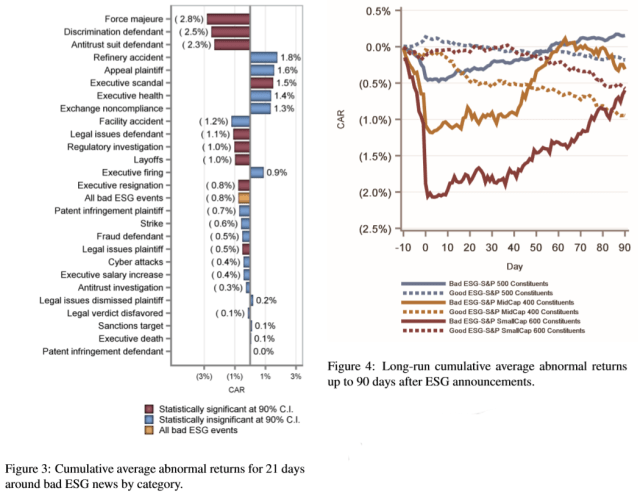

We also examined which categories of ESG bad news generated the greatest stock price reaction (see Figure 3) over the 21 trading days centered on the ESG news announcement date. The largest negative abnormal returns were related to corporate governance: force majeure. in which a firm seeks to be excused from performing its part of a contract; discrimination defendant in which the company is sued for discrimination; and antitrust suit when the company is the defendant in a legal action for unfair business practices.

To further test the proposition that investors with a strong focus on firms’ ESG characteristics are likely to overreact to ESG news, we analyzed institutional investor holdings around ESG news events. The results confirm a pattern of decreased institutional holdings around the time of bad ESG news and the change in institutional ownership around ESG events was also noticeably larger for small- and mid-cap stocks. The results provide further evidence of a subset of institutional investors selling stock holdings following ESG controversies, and in doing so, contributing to significant negative returns around the time of the event.

If investors overestimate ESG risk for a stock after a bad news event, it follows that the reaction of the market will be out of step with the change in fundamentals associated with the news — and abnormal returns will result. To test this proposition, we examined longer-run post-announcement returns subsequent to the initial negative returns around ESG controversies.

Evidence of positive abnormal returns in the 90-day period after bad ESG news announcements is shown in Figure 4 below. As we predicted, returns were larger in magnitude for smaller capitalization stocks, and there was no long-term trend in abnormal returns following positive news announcements.

In addition to the singular relationship between ESG announcements and returns, we conducted a multivariate analysis to see whether particular characteristics of firms affected returns around ESG announcements. We also examined whether overreactions were accentuated in small firms and in those with a large proportion of the outstanding equity held by transient institutional investors.

Our multivariate analysis confirmed that the abnormal returns around bad ESG news were greater than around good ESG news and that abnormal returns around bad ESG news were larger for smaller firms. Similarly, the abnormal returns were larger for firms with a greater proportion of transient investors, demonstrating the follow-on effects of such investors overweighting the probability of realizing ESG risks again in the future.

Conclusion

Salience theory suggests that investors overestimate the probabilities associated with salient events. So when an ESG controversy occurs, investors overestimate the chances that the event will recur and therefore overreact to the news. Consistent with this proposition, our study found a negative effect on returns when negative ESG news was released, but that these returns mean reverted over the subsequent 90 days.

The impacts — both for announcement returns and subsequent reversals — were strongest for smaller capitalization stocks and those stocks held by more transient investors before the news release.

Our research has several important implications:

- First, we demonstrate the potentially adverse implications for market efficiency of biases induced by the growing focus on ESG information.

- Second, our study shows why institutional investors that adopt ESG in their information set need to carefully condition their trading activities around ESG news releases to avoid overreaction and consequent losses.

- Finally, given the observed overreactions to ESG news, there may be potential for contrarians to buy stocks after the release of negative ESG news and prompt from the subsequent mean reversion.

For more on this subject, check out the full study from Bei Cui, PhD, and Paul Docherty, PhD.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Arsgera

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.