[ad_1]

After the 2020 market plunge and subsequent recovery, now is a good time to revisit the logic of dollar-cost averaging (DCA) in investing.

Benjamin Graham first popularized DCA in his seminal 1949 book The Intelligent Investor. He writes:

“Dollar-cost averaging [ . . . ] means simply that the practitioner invests in common stocks the same number of dollars each month or each quarter. In this way he buys more shares when the market is low than when it is high, and he is likely to end up with a satisfactory overall price for all his holdings.”

DCA is a sound strategy when clients are saving or investing a lump sum. During a client’s accumulation years, DCA adds discipline to the process. When clients invest every month in a brokerage account, for example, DCA mitigates what behavioral economists call self-control bias, or the tendency to consume today at the expense of saving for tomorrow. And mathematically, DCA means money starts compounding earlier.

Beyond brokerage accounts, DCA works well with employer-sponsored 401(k) accounts and with dividend reinvestment plans (DRIPs), when, say, a company pays a large dividend but the client doesn’t need the income immediately.

DCA’s benefits are not as obvious when allocating a lump sum. But clients can lower the downside risk of investing the proceeds from a pension payout, inheritance, sale of a business, simple account transfer, etc., with a DCA approach rather than investing it all at once.

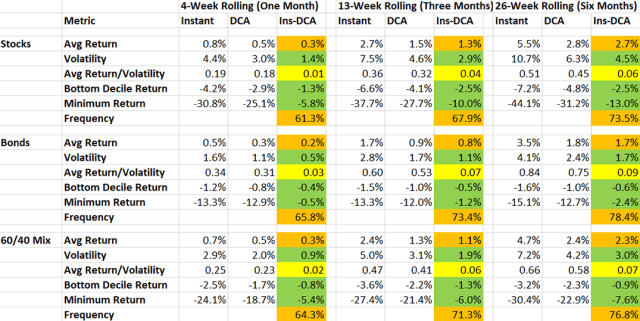

By comparing historical returns, we quantified just how much DCA can lower that downside risk. We examined index portfolios for stocks, bonds, and 60/40 mixes across rolling time periods since 1990. For the DCA period, we assumed the lump sum was invested on a weekly basis over one, three, and six months, which are more realistic time frames than monthly installments over a year since most clients would find the latter inordinately long. Moreover, the longer the time frame, the further the asset mix will stray from the target, and clients who need investment income in retirement simply won’t want to wait a full year to allocate all the proceeds.

Our findings are distilled in the following chart:

Immediate vs. DCA Investing

Notes: Using weekly data from 1 Jan. 1990 to 30 Nov. 2020; Stocks are S&P 500 TR. Bonds are Barclay’s US Corporate TR.

The colored columns show the difference in returns between immediate and DCA. The orange squares denote when the immediate approach worked better, the green when the DCA was preferable, and yellow when immediate is slightly better.

Consistent patterns emerge across the three asset sections and across the rolling time periods. Investing immediately generates higher average rolling returns than DCA with the delta rising as the length of the rolling periods increase. The higher returns result from compounding earlier with no cash drag. The frequency that immediate outperforms DCA also increases over longer time frames.

So what advantages does DCA bring for downside risk?

Volatility, or standard deviation, decreases with DCA and the difference grows with time. DCA’s benefits are especially clear with the bottom decile and worst returns, which follow a similar pattern. The average rolling return/volatility ratio is slightly but immaterially better for immediate investing. Of course, since these are rolling returns over short periods, risk free rates will be low and the more precise Sharpe ratio will follow a similar pattern. So immediate investing generally produces higher returns, but with more risk, especially on the downside.

Most clients will appreciate the DCA’s lower risk. All investors are prone to regret aversion and loss aversion biases, or, respectively, the tendency to avoid action out of fear it will turn out badly and to feel losses more strongly than gains. Indeed, the potential for losses is on average twice as powerful a motivator as the potential for gains. These impulses are likely amplified for retirees with large sums of fresh cash.

Indeed, DCA offers the most upside to retirees and those on the cusp of retirement. First, retired clients rely more on investment income and generating that income will be their first priority. Second, DCA is a hedge against sequence of returns risk, or the potential for large losses early in retirement. The “bite” such losses take out of a portfolio is bigger the earlier it occurs. DCA can lower the risk of such outcomes. In the chart, the worst four-week rolling return for a 60/40 portfolio over the last 30 years was -24.1% in March 2020. A DCA approach would have reduced that loss to -18.7%. And by actively selecting the most attractive stocks and bonds, that downside risk could be mitigated even further.

In sum, the wisdom of DCA is time-tested. DCA has broad applications for all manner of clients, but especially for those in or near retirement and for whom income generation is more of a priority. For lump-sum investing, our analysis demonstrates its utility as a risk-reduction technique.

And finally, lest we forget, DCA was good enough for Ben Graham. So who are we to argue?

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Advisory services offered

through Wealth Enhancement Advisory Services, LLC, a registered investment

advisor and affiliate of Wealth Enhancement Group®. Wealth Enhancement Group is

a registered trademark of Wealth Enhancement Group, LLC.

Image credit: ©Getty Images / LdF

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.