[ad_1]

Exchange-traded funds (ETFs) have increased market access for millions of investors, a development that most have cheered. Yet there are lingering concerns that ETFs have injected new risks into the system.

These concerns are based on misperceptions.

That is the conclusion of a growing body of evidence culled from actual market events and data collected by the US Securities and Exchange Commission (SEC).

The misperceptions generally involve the role ETFs play in volatile markets and the reliability and inner workings of the ETF ecosystem. They are being driven by the rapid growth of ETFs, which currently measure $6.1 trillion of assets under management.1 Some fear that this vast and ongoing expansion has created potentially systemic risks.

We disagree. We believe that the opposite is true: ETFs are a boon to financial markets, especially at scale.

Here are three reasons why:

1. ETFs are a pressure valve.

Yes, ETFs play a role in stressed markets — a positive one. Because they are bought and sold on exchanges like stocks, ETFs add a layer of liquidity that makes it easier for investors to set prices when the underlying markets may be frozen or difficult to trade.

Think of it this way: ETFs act as a “pressure valve” in uncertain times.

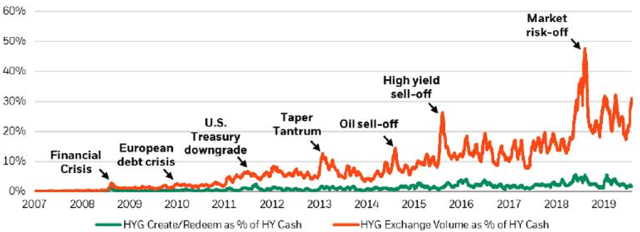

This development has been a game changer, particularly in fixed-income markets, which can be challenging to trade even on good days. When bond prices roller-coastered during the so-called Taper Tantrum in June 2013, bond ETFs stepped in. Trading volumes in the largest high-yield bond ETFs spiked to as high as 25% of the underlying market.2 That pattern has been amplified in subsequent shocks, as more investors turn to ETFs to express their market views in real time.

Representative High-Yield ETF Market Activity

2. Creation and redemption activity is a fraction of ETF trading.

A related question often arises around the role of ETFs in the primary (or underlying) market, where ETF shares are created and redeemed. Some, speculate that such activity strongly influences individual stock trading.

But our research shows that ETF flows — no matter how vigorous — have very little impact on activity in the primary markets. The reason: Most ETF trades simply result in a change of ownership rather than buying and selling in the underlying assets.

Creations and redemptions are typically a fraction of trading in ETF shares. Recent data shows that secondary-to-primary activity occurs at a 5:1 ratio. This means that for every $5 of ETF activity in the secondary market, only $1 flows through to the primary (underlying) market.3

3. The ETF ecosystem is incredibly robust.

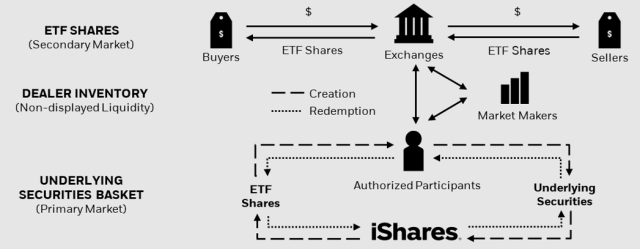

Authorized participants (APs) play central roles in the ETF ecosystem. These institutions help ensure accurate pricing and smooth trading in all market conditions. APs transact with ETF issuers to create or redeem ETF shares based on market demand.

Until recently, data on the AP universe have been difficult to source. That has led to unsubstantiated speculation that their services are both overly concentrated among a few firms and that they are potentially unreliable, at risk of stepping away from their responsibilities during volatile markets.

The SEC has delivered some much-needed transparency to the subject. Thanks to the SEC’s investment company reporting modernization reforms, we now know the true breadth and depth of the AP universe.

Over a recent reporting period, 52 APs contracted across US-listed ETF. Of these, 36 created and redeemed shares, with the largest accounting for less than 25% of such activities.4

This array of APs also addresses the supposed “step away” risk. APs compete to take advantage of arbitrage opportunities in any difference between the market prices of ETF shares and the fair value of underlying securities. That economic incentive makes it almost certain that someone will step in, regardless of market conditions. Should every AP choose to hang back for some reason, an ETF would simply trade at a discount or premium, similar to a closed-end fund.

Building for the Future

The rapid growth of ETFs has led many, including academics and the press, to question the role that ETFs play in financial markets. In response, policymakers and global standard-setting bodies have spent a lot of time researching the performance and mechanics of these evolving products.

We have made progress through new regulations. The ETF Rule in the United States, for example, offers investors more transparency than ever before. But there is still more to be done.

We also need to develop a classification framework that lays out the different types of exchange-traded products (ETPs) and their attendant risks — something that BlackRock has long advocated.

A lack of clarity can sow confusion and disappointment, particularly during periods of market turbulence. A case in point is the volatility spike in February 2018. That’s when a 115% jump in the Cboe Volatility Index (VIX) caused ETPs tied to inverse strategies to decline precipitously, and famously led to the closure of an inverse exchange traded note (ETN), an unsecured obligation.

In contrast, “traditional” ETFs generally performed well — some even with near-record volumes of trading. While both types of products performed as designed, commentators didn’t note the difference.

“The evolution of ETFs is far from over,” Maureen O’Hara and Ayan Bhattacharya observe in ETFs and Systemic Risks. On that, we agree.

As new market events unfold, more data and insights into ETF performance in varying market conditions will become available. To truly make progress, we must use this data to test these hypotheses rather than speculate about them.

1. Markit, BlackRock, as of 31 December 2019. (Excludes exchange-traded commodity, exchange-traded note, and exchange-traded mutual fund assets.)

2. Bloomberg, 18 June 2013 through 25 June 2013.

3. Bloomberg, BlackRock, Form N-CEN, as of 13 November 2019.

4. BlackRock, Form N-CEN, as of 13 November 2019.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

© 2020 BlackRock, Inc. All rights reserved.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images/Jan Auer / EyeEm

Professional Learning for CFA Institute Members

Select articles are eligible for Professional Learning (PL) credit. Record credits easily using the CFA Institute Members App, available on iOS and Android.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.