[ad_1]

The credit markets have developed a highly concentrated buy-side structure since the global financial crisis (GFC). Driven largely by regulators, this has limited financial institutions’ ability to provide market liquidity at a critical time. As low interest rates and central bank bond buying have inflated corporate bond issuance, liquidity-providing facilities are more important than ever.

As a consequence, market participants have turned to exchange-traded funds (ETFs) to access an ostensibly alternative source of liquidity, creating a new and important buy-side investor as a result. However, as our analysis shows, this liquidity expectation is not wholly accurate. The high concentration among ETF providers — and the resulting replication of ETF algorithms — has focused trading pressure on specific bonds, creating more volatility as well as higher liquidity costs when ETFs face selling pressure.

Within this context, other questions remain: For example, what are the implications for the wider fund management industry, particularly alpha-seeking active managers and asset owners considering portfolio construction decisions?

How Has Corporate Bond ETF Growth Affected the “Alpha Stars”?

Passive investing’s increased market share has exerted pricing pressure on active managers’ business models. Beyond the ETF’s low-cost nature, ETF scalability is a direct threat to the largest active funds that have dominated the space. Indeed, just 10 firms account for 38% of actively managed assets under management (AUM).

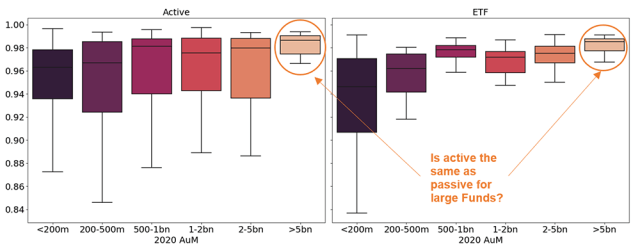

We compared the risk budgets of active and passive funds to see how much they dedicated to alpha generation. As expected, active funds directed more of their risk budgets to generating alpha than their passive counterparts. Yet, while this mostly held true, the largest funds — those with more than $5 billion in AUM — did not carry more specific risk than comparably sized ETFs.

Active vs. Passive Funds: Percent of Variance Explained by the Five First PCA Factors Split by 2020 Funds’ AUM for 2016–2021, Monthly Data

Universe of active corporate bond mutual funds with AUM above $50 million as of 31 December 2020. Alpha is estimated as the difference in performance between a portfolio of ETF funds and each active fund in the universe each year. Replications are based on loadings of each fund’s return regression on PCA factors computed on a set of 487 ICE-BofA indices over the same year over five years.

Usually, credit selection-driven alpha generation is based on identifying mis-pricings at each instrument level. However, such mis-pricing opportunities cancel out on average and are not scalable.

Can active managers therefore adapt their alpha-generation skills to their need for scale? Is alpha generation even scalable? Robert F. Stambaugh contends that active managers’ skills will likely yield decreasing returns with scale: “The greater skill allows those managers to identify profit opportunities more accurately,” he writes, “but active management in aggregate then corrects prices more, shrinking the profits those opportunities offer.”

Intuitively, active managers that strive for issuer selection alpha at scale will accelerate price discovery to the point where their skill return vanishes. If this is correct, the race for scale among active managers in response to low-cost ETF competition may be self-defeating.

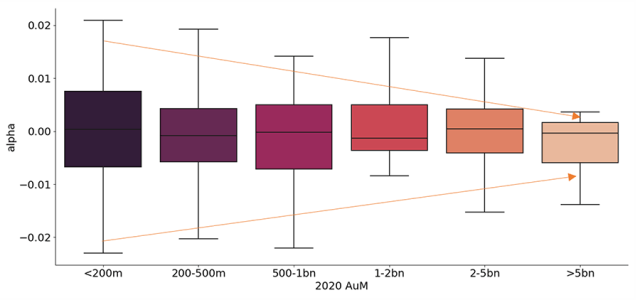

Corporate Bond Mutual Funds: Alpha Distribution Split by 2020 AUM, 2016–2021, Monthly Data

Universe of active corporate bonds mutual funds with AUM above $50 million as of 31 December 2020. Alpha is estimated as the difference in performance between each active fund in the universe and a portfolio of ETFs each year. Replications are based on loadings of each fund’s return regression on PCA factors computed on a set of 487 ICE-BofA indices over the same year over five years.

Our assessment of how alpha generation has evolved in a defined corporate bond universe over the last five years reflects this conclusion. To echo Stambaugh, the scalability of observed alpha generation remains a challenge: The higher a fund’s AUM, the lower the dispersion of outcomes in terms of alpha.

Selection can clearly add value for funds below $200 million in AUM: The first quartile of these funds generated more than 0.75% of alpha per year and up to 2% annually over the last five years. Yet this demonstrates that greater AUM reduced the magnitude of potential outcomes: In funds with more than $5 billion in AUM, even first quartile funds barely provide more than 0.5% of alpha each year.

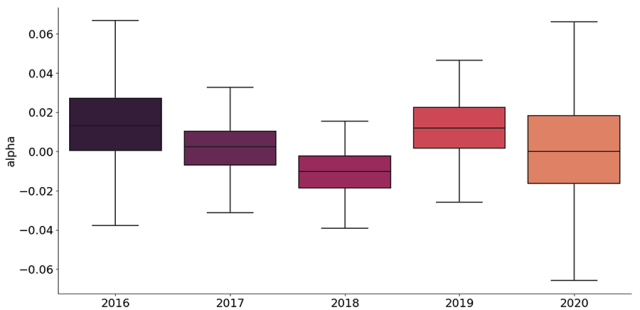

Further, the dynamics of alpha generation over time shows a recurring pattern: The vast majority of funds record good and bad years in tandem. For example: 75% of our identified fund universe underperformed an equivalent ETF-based strategy in 2018, while 75% outperformed the year after. This is not consistent with the concept of alpha and suggests either a common factor is missing from the ETF sample or a high correlation among timing and credit selection bets across active managers.

Corporate Bond Mutual Funds: Yearly Alpha Distribution, Weekly Data

Universe of active corporate bond mutual funds with AUM above $50 million as of 31 December 2020. Alpha is estimated as the difference in performance between a portfolio of ETFs and each active fund in the universe each year. Replications are based on loadings of each fund’s weekly return regression on PCA factors computed on a set of 487 ICE-BofA indices over the same year.

Identifying the funds with the best alpha-generating skills is a tough job in the best of times, but our analysis suggests that whatever the AUM, the probability of selecting the right manager is comparable to a random coin toss.

What Does This Mean for Investors?

The increased complexity of global credit markets brought about by the GFC and exacerbated by the pandemic leaves much for investors to consider. Two conclusions stand out. First, intense competitive pressure on the corporate bond market’s buy-side is highly concentrated both for ETFs and active management. And while ETFs have increased their market share in the credit space, this comes at some cost for long-term investors: They face the same concentration risk as the indices they replicate, an increased liquidity premium, and further buy-side concentration in the race to reach critical mass.

Second, active managers, the largest funds in particular, face sizeable challenges in delivering alpha. They demonstrate a convergence towards passive with respect to the risk allocated to bond picking or market-timing skills as performance drivers. This alpha delivery challenge raises questions about the extent to which active managers can operate in credit markets at scale.

With this in mind, quantitatively driven credit investing may be the only realistic way for active managers to achieve ETF-like scalability. An approach based on maximum diversification principles, for example, can expose investors to a wide set of risk and thus excess return drivers through issuer selection while controlling these exposures over time. Portfolio construction based on such a quantitative compass can also position a portfolio in a barbell-trade-like way in the space of credit market risk drivers. This could enable a scalable investment process that addresses the formidable breadth of fixed-income markets.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Haitong Yu

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.