Earlier this year, the combination of prolonged ultra-loose economic policy, broken supply chains and the tumultuous geopolitical landscape led to rocketing inflation in the United States, a country that had struggled to keep its head above the self-selected 2% target.

Facing eye-watering, four-decade highs in the CPI, Governor Powell began hiking rates in March. Since then, the Fed has raised the benchmark fed funds rate by 300 bps, settling on a corridor of 3% – 3.25% this month.

Are you looking for fast-news, hot-tips and market analysis? Sign-up for the Invezz newsletter, today.

In last week’s meeting, the Fed raised rates by 75 bps for the third consecutive time, thrice the standard rate of monetary tightening.

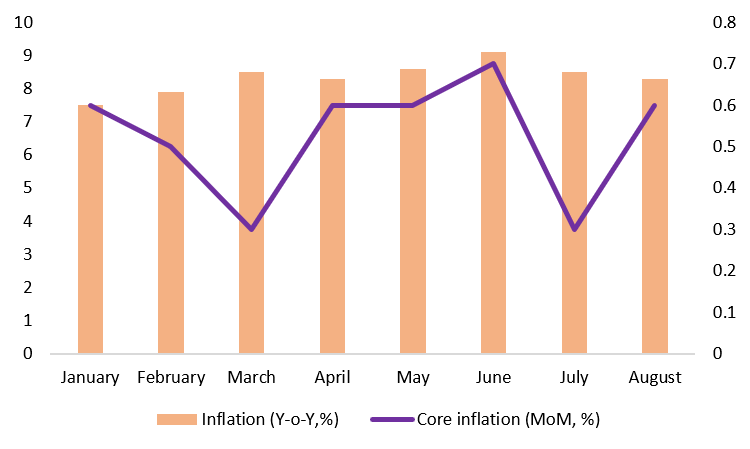

As reported previously on Invezz, the latest CPI data registered a disappointing 8.3% with core inflation being above expectations.

Given the rate of rising prices, Krishna Guha, Vice-Chairman of Evercore ISI and previously, an Executive Vice President at the New York Fed, believes that,

The Fed has to do more on rates.

Although the Fed’s 75 bps hike was widely expected, the FOMC’s announcement at the September meeting shook markets as the S&P 500 plummeted to below 3,700 levels, tremendous volatility gripped the treasury market and the DXY sped to 114.0 at the time of writing.

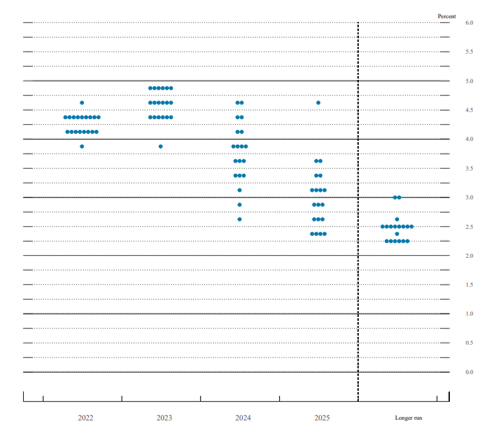

The key driver for the panic was the Fed’s Summary of Economic Projections and in particular, the much-awaited dot-plot.

Essentially, the dot-plot shows the opinion of each FOMC member as well as the presidents of each Fed bank, on where they think the Federal Funds rate should be headed. To the dismay of the markets, rates appear to be on track to tighten by another 125 bps during this calendar year itself, i.e., is expected to reach 4.25-4.5% in the December meeting.

The plot further suggests that Fed leadership is expecting to hike in 2023 before settling near 5%.

This graph requires caution while interpreting and is only reflective of the opinions of the individual Fed participants. As announced many times before, the Fed is a data-driven institution, which means new developments could alter this path.

Do note that the dots are positioned at the mid-point of a range, and do not indicate a precise target rate.

Geoff Dennis, independent emerging markets commentator, adjunct Assistant Professor at St. Mary’s College of California, and previously Head of Global Emerging Markets Strategy at UBS in Boston, noted,

There was no need for the Fed to signal so overtly that Fed Funds would be raised by another 75 basis points (in the) next meeting before a potential slowdown to a 50 bps hike in the last meeting of 2022…. inflation is not accelerating; it is falling on both core and headline, just less rapidly than the market was assuming.

In the most recent CPI data, high core inflation of 0.6% had caused the market to panic, even though there were four previous readings of above 0.6 – 0.7% in 2022.

What about the lag?

It is well-known that monetary policy transmission does not occur instantly in any economy. There is a lag between the Fed’s decision-making and the unravelling of the full impact on the ground.

The Federal Reserve Bank of San Francisco states that,

The lags can vary a lot, too. For example, the major effects on output can take anywhere from three months to two years. And the effects on inflation tend to involve even longer lags, perhaps one to three years, or more.

The difficulty is that with its emphasis on accelerated rate hikes, the Fed could quite conceivably hike too hard, too fast, and trigger an economic recession, or even worse.

For instance, Lacy Hunt, Chief Economist at Hoisington Investment Management Company said,

Inflation rate has clearly peaked and is heading downward.

However, some eminent names are in support of the Fed’s move to continue tightening.

Former Dallas Fed President Richard Fisher did not mince his words,

…they got work to do. The business of the landing, hard or soft, the greater evil is inflation if you’re a central banker.

Guha concurs, arguing that,

I think the Fed has no choice but to err in the direction of doing a bit too much because the cost of allowing high and variable inflation to become embedded in the US economy is greater, significantly than the cost of causing a recession…

Most interestingly, he believes that the Fed can bring prices in line with an acceptable trajectory in the medium to long run, noting:

…on a two to three-year time horizon and beyond, the Fed owns inflation in the US, period.

Somewhat contrary to Fisher’s and Guha’s stance, the Fed itself appears to be reluctant to acknowledge the rising probability that a recession could occur at all.

According to Mike Shedlock, an investment advisor for SitkaPacific Capital Management who runs the popular blog MishTalk, monetary policymakers are,

Purposely and wimpishly ducking recession calls, the Fed never directly projects recessions. But from where we are now, their 2022 GDP forecast goes beyond wildly optimistic and implies no recession…. It’s much easier politically to keep hiking rates if you do not forecast a recession, than if you do.

The Fed needs to think about slowing down

In an interview with Bloomberg, Danielle DiMartino Booth, CEO of Quill Intelligence, and an advisor to the Dallas Fed from 2006 to 2015 claimed that,

…(Jay Powell) knows (that) a year from now we are not going to be so crazy worried about inflation and yet he’s going to keep going.

Echoing Dennis, Hunt and Booth, the Federal Reserve Bank of New York’s Center for Microeconomic Data’s Survey of Consumer Expectations dated September 12th, found that both one-year and three-year-ahead inflation expectations declined steeply, while home price expectations fell below pre-pandemic levels.

As noted in my earlier article, shelter inflation in the US is calculated in a manner that usually causes the index to lag other components of the CPI. With housing accounting for two-fifths of the core CPI and having eased by two-thirds since April 2022, there is likely a lag adjustment period during which reported CPI figures will appear more durable than they are.

An incensed Jeremy Seigel, the Russell E. Palmer Professor Emeritus of Finance at Wharton, University of Pennsylvania, also pointed to falling commodity prices as part of the evidence that consumer prices are easing.

To keep up to date, check out Invezz’s latest research on global commodities.

But then why tighten so hard into a recession?

Knowing that monetary policy is a lagged enterprise and with signs of easing, is the Fed right to keep hiking as aggressively as they are indicating?

Over the weekend, Dennis noted,

(I) was asked in a media interview if the Fed ‘wanted’ to drive the economy into recession. I said no, but sometimes you wonder… (there is) no reason for policy overkill… the risk of recession has materially increased.

One potential argument for the actions of the Fed is that it is tired of its waning market credibility.

In the run-up to the Fed meeting, despite Powell’s committed rhetoric, and the aggressive hawkishness at the Jackson Hole conference (commentary of which is available in my earlier article), markets still expected the Fed to ultimately capitulate and ease financial conditions, i.e., show weakness in their resolve to tackle high inflation.

This is the reality of the Fed put, the idea that if equity markets and other financial instruments begin to lose value too fast, monetary authorities will step in and provide support with highly accommodative policies no matter what.

As per Mott Capital Management, in a September 18th piece titled, “The Fed Needs to Break the Market at This Week’s Meeting”, fed funds futures markets continued to price in rate cuts before the end of 2023, contrary to Powell’s announcements.

Since the Fed can only take action on short-term rates, aggressive forward guidance would be needed to convince the markets that inflation will be brought down, and kept down at any cost. Where better to signal such intent than the September dot-plot?

Given the Fed’s shaky market credibility, Mott Capital Management argued that the September dot-plot had to communicate that rates would continue to be hiked and would stay high – a goal it seems to have met in an emphatic fashion.

Post the meeting, Booth went on to say:

I think the fed has already told us that they are going too far… It’s not inflation, he’s already seeing signs of disinflation in discretionary goods. We’ve all seen signs of housing turning…and that to me means he (Powell) wants to break the market psyche of the fed is always going to have your back.

To reiterate, Booth believes that Fed hawkishness is not about inflation, or at the least, not just about inflation.

This is an altogether different possibility. The Fed may continue to raise rates not to keep inflation in check, but to convince markets that they will not falter in that quest.

In short, the Fed wants to establish its independence from the market, and drive its own monetary policy in a break from collaborative and responsive central banking over the past decade.

In the recent past, the Fed has been especially weighed down by its inability to reach 2%, its premature policy reversal in 2019, and then its insistence that inflation was transient. To exorcise these ghosts, Powell would have to break the Fed put.

If Booth is correct, expect much more destruction in financial markets in the time to come.

Invest in crypto, stocks, ETFs & more in minutes with our preferred broker, eToro.

10/10

68% of retail CFD accounts lose money

[ad_2]

Image and article originally from invezz.com. Read the original article here.