[ad_1]

Introduction

A falling stock market is not bad for everyone. Sure, many investors lose out as their portfolios decline in value, but those who are just starting to invest or have underweighted equities can benefit from lower valuations, which tend to deliver higher returns over the long term.

Naturally, equity markets do not fall without reason. As the economic environment changes, so do expectations. The positive feedback loop that sends valuations rising eventually reverses course and turns negative. But at some point, economic and business conditions stabilize and valuations come down enough to attract new investors and lure old ones back in. For instance, companies with anticyclical business models can increase their appeal by raising their dividend payments.

But not all securities markets exhibit the same dynamic as that of equities. For example, the Italian lira consistently lost value against the Deutsche Mark for decades before both currencies were merged into the euro, and currencies can effectively become worthless when hyperinflation sets in.

So, what about cryptocurrency tokens? Critics have long raised concerns about their intrinsic value, or lack thereof, and there doesn’t seem to be a relationship between a token’s price and the product for which it is supposed to serve as a medium of exchange.

But with nearly 10,000 cryptocurrencies available, security selection should matter. So, does it? Can token pickers demonstrate differentiated performance?

Probability of Making Money in Cryptocurrencies

One of the more profitable approaches to cryptocurrencies is to invest in the private seed round of a start-up seeking token financing. The early price tends to be heavily discounted relative to the public sale price, which is comparable to pre-IPO investing.

But more than four out of five tokens trade below their initial trading price, according to an analysis of nearly 10,000 cryptocurrencies by Jackdaw Capital, a London-based asset manager.

Crypto Tokens: Current Price vs. Initial Trading Price

Types of Tokens

Such odds — less than 20% that a token traded on an exchange will eclipse its initial listing price — make token investing challenging. But there are different kinds of tokens. Some categories might still offer investors the prospect of attractive returns via security selection.

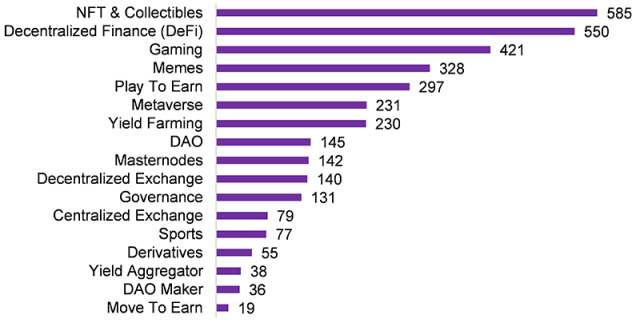

To find out, we constructed a universe of the more than 3,500 tokens trading today and divided them into 17 categories. The largest category — non-fungible token (NFT) and collectibles — had 585 constituents, while the smallest — move to earn — had only 19. These token varieties represent different crypto products that ought to be relatively uncorrelated.

Token Types: By the Numbers

Token Performance

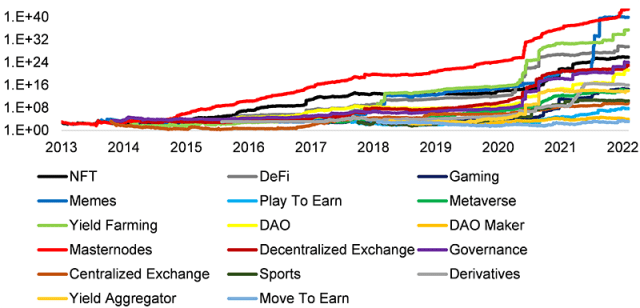

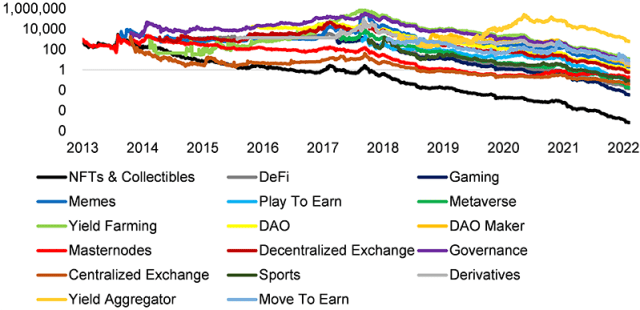

Next, we created equal-weighted indices for each of the 17 token categories. The majority of our categories have only a few years of trading history, but NFTs and masternodes go back to 2013 with track records of almost a decade.

Most of these indices generated such abnormally high performance that we needed a logarithmic scale to measure them. This explains much of crypto’s appeal: The potential for 1,000% annual returns can be tough to resist.

Token Performance by Type

Cryptocurrency Volatility

But the crypto market hit a rough patch over the last few months. Its total market capitalization decreased from nearly $3 trillion to less than $1 trillion, while bitcoin declined from an all-time high of $69,000 in November 2021 to $20,000 as of this writing.

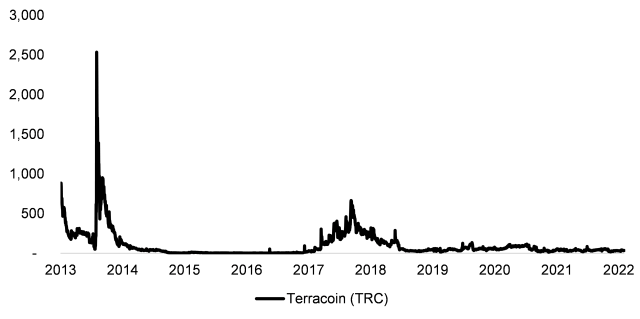

Still, the log charts hardly register the cryptocurrency crash of 2022 since token indices use the mean return and equal weighting for index calculations. Tokens exhibited such a high positive skew that the average return moved up significantly more than down. For example, Terracoin (TRC) skyrocketed from $52 to $2,535 in just a few days in 2013. The maximum a token can lose is 100%, but the upside could be parabolic.

Cryptocurrency Volatility: Performance of TRC

Token Performance Adjusted for Reality

Since the average investor cannot participate in every token sale, however, the mean return is not an accurate measure of a token index’s performance. The median return is a better metric. And it tells a much different story.

All 17 token types have lost money for their investors since the inception of the indices.

The performance between 2013 and 2018 — the peak of the first crypto bull market — was differentiated, although only a few tokens traded. Some token types — governance, for example — did well relative to, say, NFTs. From 2017 into 2018, however, hundreds of initial coin offerings (ICOs) took place. Many of these were, at best, speculative; others were outright scams.

Since 2018, all token varieties have been in a consistent decline. Despite their different purposes and ostensible business models, all types of tokens followed the same downward trajectory. This implies that security selection does not matter in the crypto space.

Furthermore, our universe is composed of tokens that are still trading and thus includes some survivorship bias. So, the returns are slightly overstated, which makes the perspective even more negative.

Token Performance by Type: Median Returns

Inflationary vs. Deflationary Tokens

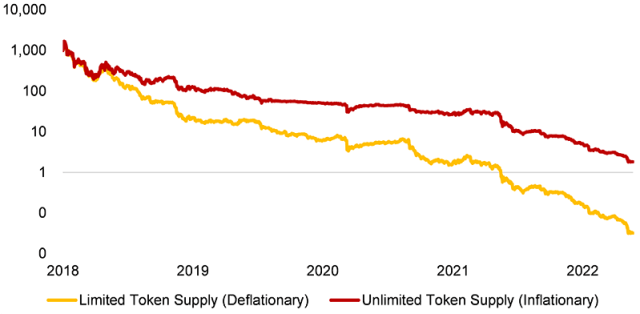

But maybe these bearish results are not as bad as they look. What happens if we differentiate between cryptocurrencies with a limited supply, like bitcoin, and those, like Ethereum, that have no supply constraints? Bitcoin and other limited-supply tokens could have a deflationary effect, especially when the issuer buys back tokens, while unlimited tokens could be inflationary as more and more tokens put downward pressure on token price.

We divided the 550 DeFi tokens in our universe along these lines and found little difference between these two varieties from 2018 to the present. The supposedly deflationary limited-supply tokens actually performed worse.

Performance of DeFi Tokens: Limited vs. Unlimited Token Supply

Further Thoughts

Fund managers have had a hard time creating value through security selection in equities and other traditional markets. Alpha generation has been low to negative over the last few decades. Theoretically, the new and complicated world of cryptocurrencies should offer plenty of information asymmetries that sophisticated investors can exploit.

But alas, theory and reality often clash in the investment world. All varieties of tokens exhibit the same negative performance trends, which makes it a challenging environment for security selection.

The average cryptocurrency hedge fund manager does not provide anything more than exposure to bitcoin. Investors can replicate such exposure themselves efficiently and at low cost through exchange-traded funds (ETFs).

The new world very much looks like the old world.

For more insights from Nicolas Rabener and the FactorResearch team, sign up for their email newsletter.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Nawadoln Siributr / EyeEm

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.