[ad_1]

Your potential alpha isn’t just where the map differs from the territory. It’s where the map differs from the territory and where other investors are misusing that map.

Continuing in the wake of the previous memo, let’s examine the balance sheet.

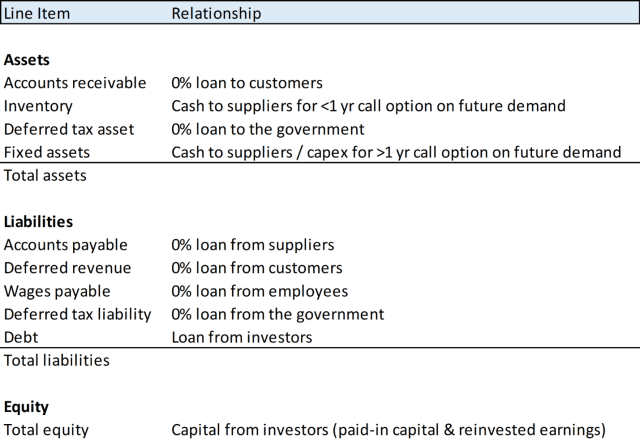

Counting the Whole Balance Sheet

Equity and debt investors are the most common sources of capital, but they aren’t the only ones.

Warren Buffett introduced many

investors to the concept of insurance float — cash collected in advance from

customers that is akin to a 0% loan. In a way, insurers are estimating the

acquisition cost and default rate of these 0% quasi-loans.

You can extend Buffett’s thinking to categorize each balance sheet line item by the relationship it represents: customers, suppliers, employees, investors, and the government.

Categorizing the Balance Sheet by Relationships

If you characterize these float sources as 0% loans, you should analyze them with a debt investor’s mindset. These quasi-loans can be useful or risky depending on their credit, maturity, and liquidity profiles. For example, supplier financing through accounts payable has been a cheap capital source for Costco but a source of pain for some factor finance firms.

Inventory and fixed assets don’t fit this quasi-loan mold. They more closely resemble real call options. A company buys inventory with the expectation that this real option will end up in the money — that a future customer will buy the goods. Suppliers typically have no obligation to return the cash if the inventory doesn’t sell, so it’s not a quasi-loan. Fixed assets work in much the same way. It’s a fun intellectual exercise to model writeoffs, depreciation, and amortization as decay on those real options, but so far I haven’t found this to be a material source of alpha.

Rethinking the cost of capital may be

more useful.

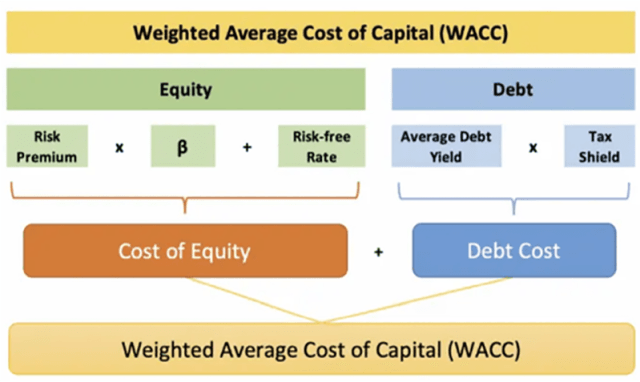

WACC Should Include All Liabilities

Cost of capital is a tenuous concept.

Charlie Munger amusingly calls it a “perfectly amazing

mental malfunction.”

Different people have different capital sources and opportunity costs. Why do we assume that every investor should use the same discount rate? Moreover, a company’s cost of capital is path dependent at the company level and the macro level. Why do we project one static discount rate instead of simulating many potential paths for cost of capital?

But if we insist on using this formula, we should at least count all of the capital sources that companies tap. To start, here is the current definition of the weighted average cost of capital (WACC):

Weighted Average Cost of Capital (Current Definition)

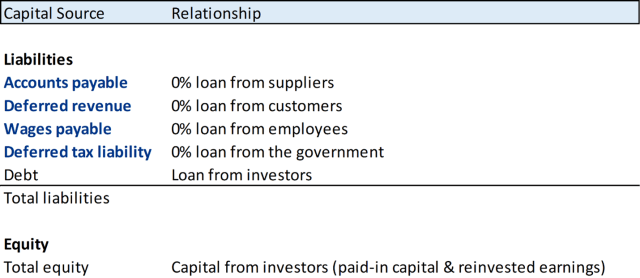

The traditional WACC is limited to capital provided by investors. It really should be expanded to include non-investor capital sources, as highlighted in blue below.

Cost of Capital Should Include All Liabilities

Two companies could have the same

traditional WACC — only debt and equity from investors — but one could have a

cheaper true cost of capital when those 0% quasi-loans are included.

Non-investor capital sources have

interesting nuances of their own.

Employee and government financing are deferred expenses, so they aren’t true capital inflows. They are, however, quite useful for large corporations with steady cash-flow streams to shield. Berkshire Hathaway’s ballooning deferred tax liability is a prime example here.

Customer and supplier financing are sources of new capital. In these scenarios, customers pay ahead of time, and suppliers send inventory to a company before requiring payment. Examples of customer financing include Kickstarter projects, Tesla’s $14 billion Model 3 pre-sale, and annual contracts in SaaS. Some examples of supplier financing are Walmart’s extension of their payment terms from net 20 to net 90 and small merchants guaranteeing inventory availability to Groupon’s marketplace.

This broadened WACC can be an alpha opportunity when a company has an underappreciated capital source and, more importantly, when that source can meaningfully change a company’s overall cost of capital.

The Market Value of Equity

When Luca Pacioli codified

double-entry accounting in 1494, publicly traded

stocks did not exist.

That’s probably why early accounting standards weren’t built to update the balance sheet based on fair market value. Why pay attention to quotes in the stock market when there was no stock market to pay attention to?

To this day, GAAP accounting only tracks equity book value at historical cost — contributed capital plus retained earnings after taxes and dividends. If the stock market prices that equity higher or lower than book value, this new valuation is not incorporated into the company’s accounting.

The problem is that companies continue to transact in their own equity after going public. In fact, making it easier to transact in their own equity is the entire point of going public. A public company should have less difficulty selling equity to outside investors, granting equity compensation to employees, and buying back equity from the market. How can investors track these transactions if they aren’t fully reported?

The way to fix this is to add a GAAP

line item for the market value of equity.

Adding a Line Item for Equity Market Value

To sidestep the debate between historical cost and fair value measures, we could add new mark-to-market line items to the balance sheet. We could also report mark-to-market changes separately from operating income. This approach would avoid jitters in the income statement and answer Buffett’s related criticism of ASC 321.

Investors are already doing this

indirectly. Popular metrics like enterprise value and the Q ratio effectively mark

equity to stock market value. Directly tracking the fair market value of equity

would make clear which companies are savvy dealers in their own equity and

which are masking their underperformance with dilution.

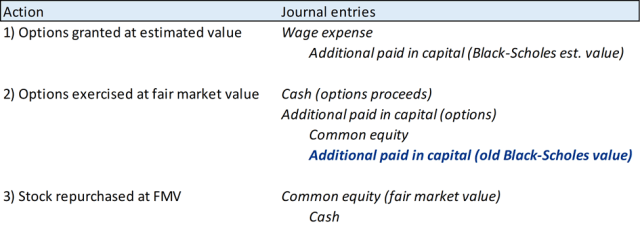

Counting Shared-Based Comp the Right Way

This new line item for equity market value would also let us properly measure share-based compensation (SBC). As it stands today, we don’t mark SBC to market.

How Share-Based Compensation Is Currently Practiced

When SBC is first granted, an appraiser comes up with a low equity valuation that gives the employee a favorable tax treatment. We just need to true up the wage expense for the current equity value when the employee exercises their options.

The lack of clarity around marking equity to market and SBC creates significant potential for alpha. It’s already challenging to screen for capital allocation — return on shares issued, return on shares repurchased, and acquisition deal structures. But the most important capital allocation metric is even more opaque — return on employees hired. Right now, it can be difficult for investors to see who is earning the highest return on the teams they’ve built.

The alpha opportunity is to find

entrepreneurs who are world-class capital allocators and underappreciated for

it. Think of the greats: Henry Singleton issuing

highly valued Teledyne equity for M&A and then buying back shares on the

cheap in the 1970s and 1980s. John Malone paying 6x

EBITDA (post-cost synergies) in cash and debt to consolidate small cable

operators into TCI. Mark Leonard adding niche

vertical software products to the Constellation Software portfolio.

Finding just one of these capital allocators early on would have made an investor’s career. In a decade, we may look back at the most charismatic team builders in the same light.

The Potential for Network-Based Accounting

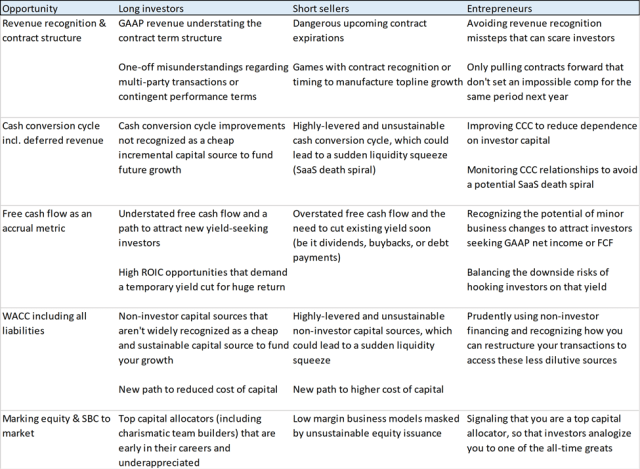

The strategies in this series are a sampling of how you can generate alpha from GAAP as it is interpreted today. How you use them depends on your strategy, whether you’re a long investor, a short seller, or an entrepreneur.

Alpha-Generating Accounting Opportunities

How long these alpha opportunities last will depend on how GAAP and fundamental investment strategies evolve over time. Double-entry accounting was developed with pen and paper. Computers could transform the foundation upon which GAAP and investment analysis are built.

Put in plain English, businesses run

on relationships. Double-entry accounting helps us track those relationships,

but GAAP currently has each company report as if it is a separate entity. We

want an easy way to see all of those relationships at once.

You might call this network-based

accounting.

Contracts are the legal marker of relationships between business entities. They are the “connective tissue in modern economics” in the words of Nobel laureate Oliver Hart. With an updated framework, we could graph networks of contracts between companies. This approach wasn’t feasible in a pre-computing era, and it’s hardly practical today with our current data standards. Renovating GAAP for the computing era would make these relationship models viable.

I think the future of accounting lies in agent-based modeling. We could treat companies as individual agents to simulate how they are interacting now and how they might interact in the future. You’d be able to see each company’s network of relationships with its customers, employees, suppliers, investors, competitors, the government, and the public at large. Some of these relationships are barely mentioned in our current model of GAAP.

Dozens of due diligence questions

would be easier to answer with network-based accounting.

Does a company have long-term or short-term customer relationships? Have the company’s suppliers started to provide interest-free financing? Could its investors be suddenly forced to sell out? And the scary one: Is there some contagious risk that could threaten the company’s network of key relationships?

The capital markets could be much, much more efficient if this framework could be properly abstracted into software. But for now, that’s just a fun conversation to have after work.

Today, I’m more interested in the alpha that we can generate with the markets as they are currently structured. And I think that GAAP and the way that investors react to GAAP reports will create significant opportunities for a long time to come.

Thanks to Tom King, Nadav Manham, Ben

Reinhardt, Kevin Shin, and Slater Stich for their help with these memos.

You can read more from Luke Constable in Lembas Capital’s Library.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: Grandjean, Martin / Wikimedia

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.