[ad_1]

With its riveting victory over France in the World Cup finals and the heroics of its all-time great team captain Lionel Messi, Argentina has good reason to celebrate.

But as the post-World Cup glow subsides, the country faces significant and deep-seated economic and financial challenges. Inflation reached an annualized rate of 92.4% for the period ending 30 November 2022, placing added pressure on a population already hard hit by years of stagflation and anemic economic growth. Moreover, after three decades of deficit spending, concerns about the solvency of Argentina’s public debt remain ever present. Indeed, the current prices of credit default swaps (CDS) indicate a 60% chance of default by 2024, according to Cbonds data.

Argentina has not always endured such dire economic conditions. In fact, it was the 10th richest country in the world per capital in the early 20th century. To be “as rich as an Argentine” was a common aspiration.

So what explains Argentina’s fall from the economic heights, how can it recover, and what lessons does it offer other emerging market economies?

Argentina’ economic golden age from 1860 to 1930 owed much to its agricultural breadbasket, the Pampas, and the bounty of wheat, corn, wine, and beef it produced. Foreign investment from Germany, France, and the United Kingdom flowed in, and high wages attracted immigrants from Italy, Spain, and elsewhere. From 1860 to 1899, Argentina’s real GDP advanced at an astonishing clip of 7.7%. per year.

During the first two decades of the 1900s, Argentina’s economy outperformed both Canada’s and Australia’s. Making a bet on Argentina’s future, Harrods even opened its first overseas location in the capital of Buenos Aires.

With the Great Depression, however, Argentina’s decades of economic expansion came to a halt. Though the pain was global and other nations suffered similar economic declines, Argentina has yet to return to a trajectory of sustained economic growth.

Inflationary Shock and the Maradona Era

Where did Argentina stray from its development path? As the Great Depression led to a collapse in Argentina’s exports, widespread populist discontent destabilized the government. Over the next 50 years, populist regimes alternated with military dictatorships. Scarred by the export shocks of the Great Depression, Argentina’s economy turned inward. Rather than grow international trade, the country’s leaders embraced a misguided economic philosophy of self-sufficiency.

Formulated by the economist Raul Prebisch, this approach sought to protect the development of domestic industries through import tariffs, subsidies, and even the nationalization of certain sectors of the economy. Following a coup d’etat in 1976, the new military junta began to reverse some of these protectionist policies and open up the economy to more international trade. But economic liberalization and the junta’s interests did not always coincide, and amid the country’s deteriorating finances, the initial results were mixed, so these efforts were soon dialed back. In 1978 meanwhile, Argentina hosted the World Cup, and the national team captured it first championship. Though the tournament had its share of controversy — state intervention was not limited to the Argentine economy — the victory constituted a bright moment in an otherwise dark era for the country.

An ongoing challenge in this era stemmed from tax revenue, or the lack of it. Shortfalls grew especially severe in the midst of the Falklands War in the early 1980s and like many governments before it, Argentina’s rulers printed more and more money to finance the conflict, setting off rampant inflation and debasing the currency. By the end of the war, the annualized inflation rate was running at 82% per year.

Argentina Inflation Rate (%), 1978 to 1984

Annual Change on Consumer Price Index

High inflation was a worldwide phenomenon in the 1980s, and Argentina was hardly alone in its struggles. As economists explored heterodox shocks to control rising prices and following a return to democratic government in 1983, Argentina’s leaders implemented the Austral Plan two years later. This replaced the traditional Argentinian peso with a new currency, the austral. (Though critics described the austral as effectively a peso with three zeros chopped off.) The Austral Plan also included wage freezes and tariff reductions.

Initially, the program reduced inflation to a more modest yearly rate of 50% or so. In 1986, the country’s GDP grew at a respectable annualized 6.1%, and, behind the legendary Diego Maradona, Argentina captured its second World Cup.

But the hoped-for recovery proved illusory as what became known as Argentina’s lost decade dragged on and economic growth continued to sputter. Massive fiscal deficits led the government to increase its money printing and inflation ramped up to unprecedented levels. In July 1989, it was running at 200% per month and ended the year at an annual hyperinflationary rate of nearly 5,000%.

Argentina Inflation Rate (%), 1984 to 1990

Annual Change on Consumer Price Index

The Reform Era

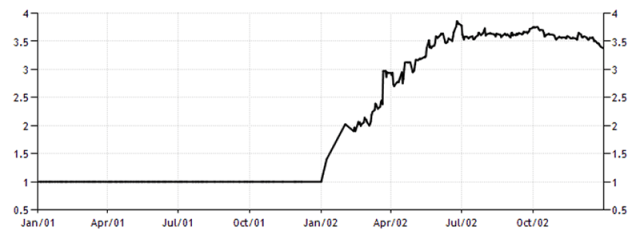

When Carlos Menem took office in December 1989, public expenses and the fiscal deficit added up to about 36% and 7.6% of GDP for the year, respectively. Menem lifted price controls, removed barriers to cross-border capital flows and international trade, simplified the tax code, and privatized several state companies. But his most fateful decision was converting the austral back to the peso and pegging it to the US dollar. This marked the beginning of what became known as the “convertibility regime,” which lasted into the early 2000s.

The fixed-exchange rate regime, or currency board, was not a new concept, and many other countries have pursued similar arrangements. But when nations peg their currency to a foreign one, they effectively forfeit their ability to conduct independent monetary policy. If the US economy grew more rapidly than its Argentinian counterpart, Argentina’s central bank had to print more money to keep up with the fixed rate of exchange. This drove domestic inflation higher as the peso supply outpaced domestic production.

In effect, the currency board was in thrall to US monetary policy. Still, the fixed-exchange rate regime initially showed promise. Inflation ran over 2,000% in 1990 but declined to only 1.6% in 1995. The Argentine government also reduced the deficit from over 7% of GDP in 1989 to 2.3% in 1990.

Taming inflation led to a huge reduction in poverty. In 1990, 29% of greater Buenos Aires households lived below the poverty line. By 1995, that had fallen to 13%.

The Cost of Monetary Policy Dependence

Menem’s economic reforms appeared to be working. But in late 1994, Mexico devalued its currency, letting it float rather than exhaust its foreign exchange reserves defending it.

This set off a chain reaction. Capital fled from Mexico, and in a phenomenon dubbed “The Tequila Effect.” investors looked around and saw the potential for other nations — Argentina among them — to float their currencies as well, This catalyzed massive capital flight out of Argentina. With fewer dollars circulating, the government slashed the money supply. Interest rates doubled from 10% to 20% in less than a year, fueling a painful recession and widespread unemployment.

Argentina Interbank Rate (%)

With no mechanism for monetary stimulus, the government increased fiscal spending and grew the public debt. In 1991, total public debt was US$61.4 billion. Only five years later, it was US$90.5 billion.

Then the Asian financial crisis of the late 1990s spread first to Russia, then to Brazil, and then to Argentina. The government kept betting that the problem was temporary and grew the fiscal deficit even further. By 1998, public expenditures were US$118 billion, almost 50% of GDP, and in what became known as the Argentine Great Depression, the economy plunged into the abyss.

The Messi Era

In 2001, Argentina had among the highest debt yields in the world with no serious plans to address them. This raised questions about the banking system’s solvency. Were there enough dollars to cover deposits? Many didn’t think so. A bank run ensued and with it the collapse of the currency regime.

Argentinean Peso

While the Argentine Great Depression officially ended in 2002, the economy has shown little progress in the decades since. The last 20 years have been an unenviable sequence of IMF programs and bailouts, debt defaults and renegotiations, soaring inflation, and a Byzantine FX system designed to limit access to foreign denominations. This has created a black market for currencies and a series of parallel exchange rates, such as “Dollar Coldplay” and “Dollar Qatar” for those who want to buy concert or World Cup tickets.

What lessons does the Argentine experience over the last several decades offer other emerging markets? The experiment with dollarization demonstrates that artificial currency pegs make currency devaluation almost inevitable and are thus best avoided.

But on a larger level, the nation’s plight illustrates the importance of sound government policy. Political turbulence and the inconsistent and at-times contradictory initiatives of successive Argentine governments have been longstanding headwinds to revitalizing the nation’s economic competitiveness. They have driven investors away. Controlling spending and avoiding chronic fiscal deficits are critical. When the Argentine government managed to keep costs down and balance the budget, the economy rebounded and with it the nation’s overall quality of life.

Argentinean GDP, in US Billions

The Path Forward

Today, Argentina has the highest inflation in the G20 and its 2022 GDP is not far from where it was in 1998. The country has effectively endured a lost quarter century.

Thanks to debt renegotiations, default is unlikely in 2023, but significant maturities will come due over the next couple years. The nation’s extraordinary fiscal and monetary problems defy easy solutions.

But Argentina’s World Cup performance perhaps provides a hopeful parallel. Between the Maradona- and Messi-led triumphs of 1986 and 2022 was a painful 36-year period during which the Argentine national team did not live up to its promise or its storied history. Yet, in 2022, it shook off more than a generation of disappointment to redeem itself. Hopefully, Argentina’s economy will chart a similar path in the years ahead and restore its earlier tradition of growth and prosperity.

Of course, whatever remedies Argentina’s government institutes must be congruent with the laws of finance. Money flows to where investments show the most promise and the least volatility, and Argentina has not been such a place for a long time. Indeed, reviving its economic vitality after nearly a century of setbacks and stagnation will require skill and leadership in the fiscal and monetary realms as great as Maradona and Messi demonstrated on the soccer pitch.

If you liked this post, don’t forget to subscribe to Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image courtesy of Кирилл Венедиктов via Wikimedia Commons under the Attribution-ShareAlike 3.0 Unported license. Cropped.

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.