[ad_1]

Dividends and buybacks are poised for a comeback this year. How can analysts gauge whether they contribute to a firm’s intrinsic value?

Corporations responded to the onset of the COVID-19 pandemic by slashing costs and raising liquidity.

In the United States, non-financial companies now hold $2.6 trillion in cash, the equivalent of over 5% of total assets. That’s down from an all-time peak of 6% set last summer. Meanwhile, net debt-to-EBITDA ratios are well below those in previous decades.

US Corporate Cash/Assets

Sources: US Federal Reserve and Wealth Enhancement Group, as of 31 March 2021.

As earnings growth and the larger economy start to recover, companies are poised to deploy their cash through capital expenditures (capex), mergers and acquisitions (M&A), and cash givebacks to shareholders in the form of dividends and buybacks.

According to Bloomberg consensus projections, S&P 500 earnings will grow over 50% in 2021 and Goldman Sachs predicts increases of 5% and 35% in dividends and buybacks, respectively.

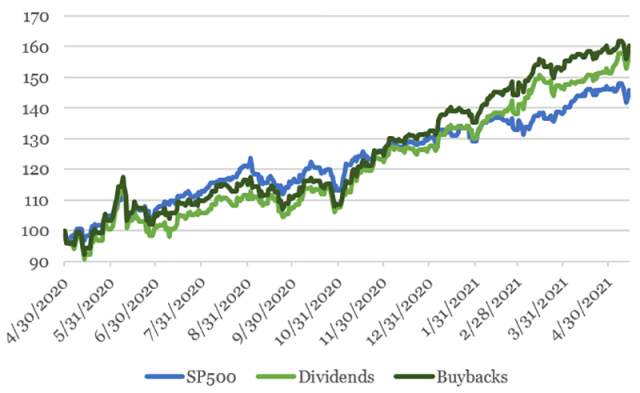

Cash givebacks should be a significant driver of stock returns, especially amid such low interest rates. Indeed, dividend and buyback stocks started outperforming the S&P 500 in early 2021.

Buyback and Dividend Stocks vs. The S&P 500

Sources: Bloomberg, S&P, Goldman Sachs, and Wealth Enhancement Group, as of 14 May 2021

While shareholders generally benefit from cash givebacks, the appeal and utility of such transactions vary by company.

Cash givebacks should boost a firm’s intrinsic value. The question is how to determine if a particular giveback accomplishes that goal. That requires a multi-step evaluation framework that answers three questions:

1. Does the company have prospective capex, R&D, or M&A activities on which to deploy its cash?

Assessing the outlook for a firm’s particular projects is a tricky enterprise: The spectrum of such activities runs the gamut and the investment details tend not to be transparent or public. Nevertheless, history can be a useful guide.

Has the company struggled in the past to generate return on capital (ROC) above its cost of capital (COC)? If so, that trend is likely to continue unless the prospective projects markedly differ from their predecessors. If ROC is expected to be low versus the COC, however, then cash givebacks become that much more appealing.

For companies with short histories, analysts can look at key capex projects or M&A. For the former, there should be a positive net present value (NPV). For M&A, to add value at the highest level, the NPV of the synergies should be more than the premium paid above the target company’s intrinsic value.

2. How much money can the firm afford to allocate to givebacks?

To determine the size of the outlay a company should earmark for shareholders, free cash flow (FCF) generation and financial leverage are good metrics to look at. The higher a company’s FCF margin, the more latitude it has to give back. An FCF margin above the market and at least equal to comparables demonstrates strong FCF generation.

But FCF variability also has to be assessed. Major drivers of FCF volatility include the corporation’s growth stage and its sector’s cyclicality. An early-stage high-growth company will generally have lower and more sporadic FCF than an established firm. Corporations with revenues and profitability tightly tethered to economic activity will also have more changeable FCF.

Three methods help assess a company’s debt level and whether it is over, under, or appropriately levered:

- Comparables: This simple approach weighs a company’s debt ratios against those of other firms in the same industry.

- Downside Operating Profitability: This method determines an acceptable level of credit risk assuming the worst-case scenario based on historic financials or projecting forward financials. Minimum credit ratios must be met for an acceptable level of default risk, targeted credit rating, and to adhere to bond covenants.

- Minimizing the Cost of Capital: This is the most theoretical method but helps round out the analysis. The optimal balance of debt to equity minimizes the cost of capital and therefore maximizes intrinsic firm value. How? By identifying the minimal-weighted average cost of capital (WACC) by combining a firm’s cost of debt, or interest rate, and cost of equity, or required rate of return for shareholders, for every mix of debt/equity.

By triangulating these approaches, analysts can determine an optimal leverage level.

Combining the outlook for a firm’s projects with its cash flow and leverage profile can inform an overall giveback strategy. The matrix below demonstrates the four blends:

Calibrating Cash Giveback Capacity

| Bad Projects | Good Projects | |

| Strong Free Cash Flow | Increase Givebacks Decrease Investments |

Increase Givebacks Accumulate Cash for New Investments |

| Weak Free Cash Flow | Decrease Givebacks Decrease Investments |

Decrease Givebacks Increase Investments |

Note: If firms are under or overlevered, givebacks can be adjusted upward or downward accordingly.

Source: Wealth Enhancement Group

3. Should those givebacks be dividends or buybacks?

Determining the best form of cash giveback is the final step in the process. For dividends, firms should have strong FCF generation without undue variability and have advanced beyond their fastest growth stage. The market interprets dividend changes as signals from management. It often reads the initiation of a dividend to mean a company’s long-term growth prospects have dimmed. Benchmarking against the dividend yields and payouts of similar firms can offer useful insights.

A buyback’s suitability hinges on the answers to the following questions:

1. Is the stock undervalued?

If an equity is trading below its intrinsic value, it is a good investment, and it makes sense to buy back shares.

2. What is the firm’s growth stage?

If the company is past the early growth stage when it is investing heavily, buying shares may be appropriate.

3. Is the firm in a cyclical industry?

If so, the flexibility of buybacks may make them preferable to dividends.

4. How important are employee stock options for attracting and retaining talent?

Many companies, especially in the tech sector, issue options to their staff and need to buy back shares to offset share dilution.

5. Is the tax rate on capital gains different than dividends?

Tax rates vary by investor type. Currently, long-term capital gains are taxed at the same rate as dividends.

In the United States, there are legislative proposals to increase taxes on the highest-earning individuals and on corporations. Political outcomes are difficult to forecast, but increasing the capital gains rate on less than 1% of investors should not materially change the buyback vs. dividend decision. Raising corporate tax rates would crimp FCF but also increase the benefit of taking on more debt to create an interest expense tax shield.

With corporate cash balances at record high levels, firms are likely to continue increasing their cash givebacks to benefit shareholders. But investors need to be aware that while givebacks are generally a good idea, some are better than others.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / champc

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.