[ad_1]

The Federal Reserve is slamming on the brakes to stem inflation — with another 75-basis-point rate hike expected Wednesday — even as the U.S. economy is sucking wind. A Fed-induced recession now seems highly likely.

X

Much of the debate is focused on whether a downturn will start this year or 2023. Increasingly, the most timely indicators suggest a recession is imminent — if not already here.

While even a shallow recession could cost over a million jobs, a near-term growth relapse may not be the worst outcome. It would help ease the biggest inflation outbreak in decades, letting Fed rate hikes end more quickly. That might avoid a more-severe recession that wallops corporate profits and provokes a further sharp sell-off for the S&P 500.

Yet under any economic scenario, inflation fears won’t subside without more pain from the Fed. The unemployment rate is bound to rise. That could come abruptly, or last into 2024 as the Fed’s low-probability “soft-landing” projections envision. So stock market investors should be realistic about prospects for a sustainable near-term rally.

As long as inflation remains a concern, Federal Reserve policymakers are unlikely to grant a stock market reprieve, BCA Research chief equity strategist Irene Tunkel told firm clients in a Monday webinar.

“Someone has to pay the price,” she said. To alleviate the “regressive tax” of inflation on poorer households, the Fed aims to cool demand via a reverse wealth effect, diverting much of the pain to “people who have wealth, who have money in the market.”

Fed Recession: Now Or Later?

Recent economic data has sent up no shortage of red flags. Initial jobless claims rose to 251,000 in the week of July 16. While historically low, claims have jumped about 50% from March lows. Some prior recessions have started after just a 20% rise in claims, notes Charles Schwab chief investment strategist Liz Ann Sonders.

Meanwhile, housing starts have plunged 14% over the past two months amid a spike in mortgage rates. Inflation-adjusted consumer spending fell 0.4% in May, more than erasing a 0.3% gain in April. The Institute for Supply Management’s manufacturing survey showed new orders suddenly turned negative in June.

Most economists have been bumping up the odds of recession. Yet there’s one big reason that many think it’s still a ways off. The June jobs report showed employers added a stronger-than-expected 372,000 jobs. If job and income growth really are still robust, the economy probably won’t give way quickly.

Job Market: Weaker Than It Looks

Yet a closer look is in order. Recall that the Labor Department’s household survey showed that the ranks of the employed fell by 315,000 in June. The survey shows 347,000 fewer people working than in March.

Economists often take dissonant household readings with a grain of salt, because the sample is smaller and margin of error greater than the employer survey. Yet, the “household survey tends to lead (employer) payrolls around economic inflection points,” Sonders wrote.

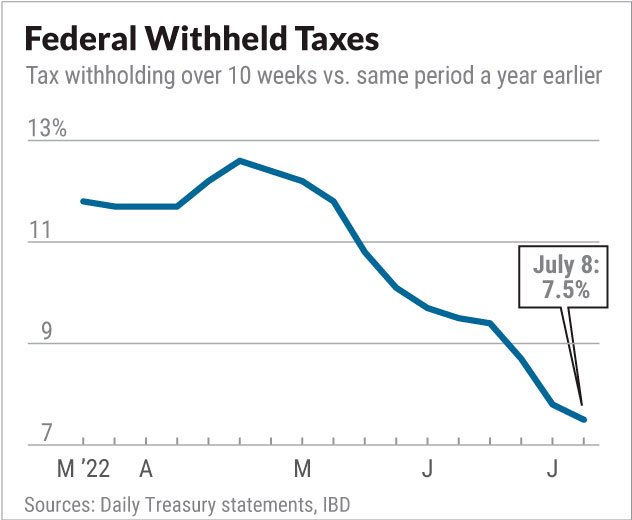

This may be one of those times. An IBD analysis of Treasury inflows finds that the growth rate of federal income and employment taxes withheld from worker paychecks has been sliding sharply. Growth in those tax receipts over the 10 weeks through July 8 faded to just 7.5% from a year ago. That’s down from about 12% through mid-May.

This may be one of those times. An IBD analysis of Treasury inflows finds that the growth rate of federal income and employment taxes withheld from worker paychecks has been sliding sharply. Growth in those tax receipts over the 10 weeks through July 8 faded to just 7.5% from a year ago. That’s down from about 12% through mid-May.

The tax data suggests that aggregate labor income — reflecting gains in wages, hiring and incentive pay across the economy — has hit an inflection point. Labor income is now shrinking in real terms.

Matt Trivisonno, who tracks tax withholdings for investors at DailyJobsUpdate.com to spot such inflection points, told IBD that he’s also seeing “a nasty reversal,” at odds with the supposedly strong job market.

Trivisonno said he’s “expecting the 372,000 jobs gained in June to be revised away in the future.”

The Federal Reserve’s ‘Most Anticipated’ Recession In History May Be Coming

Job Openings Revisited

But what about all those job openings? “I’m not aware of a time when we’ve had two job openings for every unemployed person,” Fed chief Jerome Powell said in May.

Job listings have since fallen by 600,000, or 5%. But the picture has only changed on the margins. The latest Labor Department data shows 11.3 million openings vs. 5.9 million unemployed.

Fed officials aim to cool the economy enough to reduce excess job openings and dampen wage growth, without provoking significant layoffs.

Yet a new paper from the Peterson Institute for International Economics co-authored by former Treasury Secretary Larry Summers paints those job openings in a different light. The high number of openings only partly reflects the level of economic activity. A high level of job switching has also played a role. Another more troubling factor, the paper argues, is that the economy has become less efficient in matching workers to jobs. If true, the labor market may be even tighter than the 3.6% unemployment rate, near a half-century low, suggests.

That finding yields two unwelcome conclusions: The natural, or noninflationary, rate of unemployment may be more than a percentage point higher than the Federal Reserve thinks. And bringing down the ratio of job openings to unemployed workers likely won’t happen “without a substantial increase in the unemployment rate.”

Hope For A Soft Landing?

Amid all the Federal Reserve recession talk as policymakers move aggressively to slay inflation, some on Wall Street still think Powell & Co. can nail a soft landing.

Amid all the Federal Reserve recession talk as policymakers move aggressively to slay inflation, some on Wall Street still think Powell & Co. can nail a soft landing.

The price of oil and other commodities has already fallen sharply. That could turn modest declines in real spending into modest gains. If inflation comes down enough and the job market weakens just enough, the Fed may slow, then pause rate hikes later this year, the thinking goes. Expectations of a Fed pivot have sparked broad-based stock market gains this week.

Yet even in a soft-landing scenario, the near-term outlook for the stock market may not be particularly bullish.

“In our base case for a soft landing, we think stocks will be largely range-bound with continued elevated volatility as investors assess the durability of economic and corporate profit growth in the face of aggressive Fed rate hikes and declining real consumer incomes,” wrote Solita Marcelli, chief investment officer Americas at UBS Global Wealth Management. “Historically, equity bear markets typically only end when the Fed starts to cut interest rates or the market begins to anticipate a re-acceleration in business activity and corporate profit growth. Both of these potential upside catalysts are unlikely to materialize in the near term.”

S&P 500 Earnings Outlook

If the job market and inflation soften enough for Fed rate hikes to end early, what will that mean for corporate pricing power and profits? Morgan Stanley Chief Investment Officer Mike Wilson sees the S&P 500 falling to 3,400 in a soft-landing scenario. He’s betting that inflation will cool much more than expected amid lackluster demand. That suggests big earnings downgrades are on the way.

“Profits were inflated because of inflation. Now they’re going to deflate, because we’re going to have deflation in a lot of different areas,” he told CNBC on July 12.

In Wilson’s view, the counter-argument — that S&P 500 profits will hold up — implies that “inflation is going to stay hot and pricing power is going to remain robust.” To Wilson, that seems unlikely “in an environment where we’re already seeing demand destruction and consumer confidence is tanking.”

BCA’s Tunkel says analysts have yet to cut their estimates that S&P 500 earnings will rise about 10% over the next year. In her view, stocks could fall another 10% if EPS growth is cut to zero.

“Earnings could be the next casualty,” Jefferies strategist Desh Peramunetilleke wrote this month. He noted that EPS has fallen an average 17% over the past 10 recessions.

Most Americans Think The U.S. Is In A Recession: IBD/TIPP

S&P 500 Valuation Contraction

It’s no coincidence that the S&P 500 hit at least a temporary bottom in mid-June, just as the 10-year Treasury yield was spiking close to 3.5%, a level last seen in 2011. To a large extent, the S&P 500’s 24.5% decline from the peak to trough reflected a compression of valuations, as investors used a higher risk-free rate (the 10-year Treasury yield) to discount future earnings back to the present.

Through Friday’s close, the S&P 500 has cut its losses to 17.8% below its Jan. 4 peak. The major indexes have reclaimed their 50-day lines heading into the Federal Reserve meeting and a slew of earnings reports.

Be sure to read IBD’s daily afternoon The Big Picture column to stay in sync with key market trends and learn what they mean for your trading decisions.

With the 10-year Treasury yield easing below 3% lately as investors brace for a slowdown — or worse — stock valuations have recovered a bit. Yet in a soft landing that skirts recession and a significant hit to employment, Treasury yields may hold near current levels. That means there may be limited additional relief on the valuation front, even amid a softer earnings outlook.

By contrast, even a moderate recession could spur the Federal Reserve to cut its key interest rate all the way back to zero, Arend Kapteyn, Global Head of Economics and Strategy Research at UBS, told reporters in a Tuesday call. That would help to “reverse the liquidity shock” of recent months and reinflate stock multiples, he says.

A key question for stock valuations, then, is what it will take for the Fed to pause and begin to reverse policy tightening.

Bear Market News And How To Handle A Market Correction

Fed Pivot Or U-Turn

In late 2018, the last time the Fed was hiking with both fists — via rate hikes and shrinking its balance sheet — all it took was a 20% S&P 500 drawdown to provoke an about-face. By fall 2019, the Fed was cutting rates and buying bonds again.

“The market still thinks that weak growth prints are going to get the Fed to back off,” Nomura senior economist Robert Dent told IBD. But “inflation has really tied their hands.”

In a June 18 report, Dent and fellow economist Aichi Amemiya made a Q4 recession call. They expect a “one-mandate Fed” — having effectively ditched its mandate to maximize employment so it can wrestle down inflation — to tighten financial conditions until the consumer and job market roll over.

The Nomura economists see Fed rate hikes at each of the next five meetings, with a 75-basis-point move on Wednesday. They expect a 50-basis-point move in September, followed by quarter-point hikes in November, December and February.

A pause could come sooner, but that will depend on inflation. Dent notes that Federal Reserve Gov. Christopher Waller, who is on the hawkish side, has said a pause in rate hikes could come once inflation subsides to a 2.5%-3% annualized rate. That equates to monthly inflation readings of about 0.2%-0.25%.

Dent expects that the Fed will continue quantitative tightening, letting bonds run off the balance sheet as they mature, until policymakers start cutting rates in October 2023 to avoid a deeper recession.

Looking For The Next Big Stock Market Winners? Start With These 3 Steps

Federal Reserve Policy Lags

It’s finally clear that inflation has peaked and is now on the way down. That’s certainly fodder for a short-term stock market rally. But there’s no reason to think that a peak in the CPI necessarily means a bottom for the S&P 500.

The U.S. economy is entering a tunnel, not seeing the proverbial light at the end. Despite the aggressively hawkish Fed posture, a range of U.S. financial conditions indexes, from the Chicago Fed to Goldman Sachs, still show conditions across equity and bond markets are only approaching neutral, after years of easy money.

That’s partly because of time lags before Fed policy hits the economy and partly because the Fed’s policy rate, though rising fast, has yet to reach a level that economists see as restrictive. Plus, the Fed only just began shrinking its balance sheet. So far, it’s down about $36 billion, or 0.4% of the $8.9 trillion total. But the pace will quicken to as much as $95 billion per month in August.

No Goldilocks Scenario

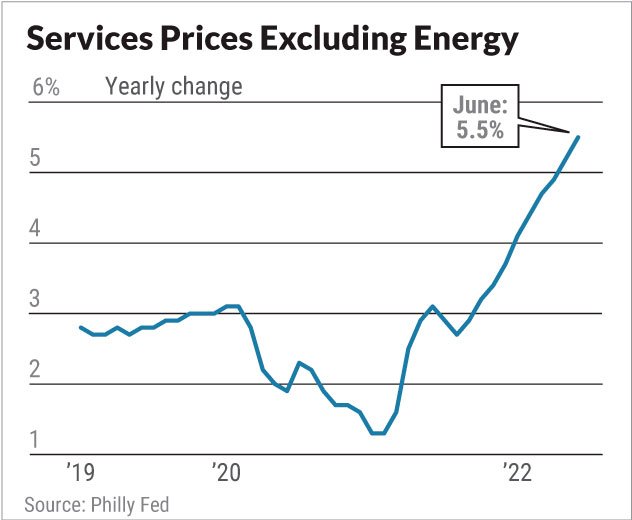

“We see inflation deeply entrenched in the economy,” Goldman Sachs CEO David Solomon said on the July 18 earnings call.

While gas prices have tumbled from their peak and goods prices have come down, nonenergy services inflation accelerated to a 30-year-high 5.5% in June. That covers 57% of consumer budgets, including categories like rent and medical services that are linked to elevated wage growth.

It may take more time and harsher medicine for the Fed to sufficiently dampen those price pressures. Or maybe it will happen faster than expected, if we really are on the cusp of a Fed-led recession. Either way, the economy and job market are in for a tough period. Stock market investors aren’t likely to be completely spared.

YOU MAY ALSO LIKE:

Why This IBD Tool Simplifies The Search For Top Stocks

Catch The Next Big Winning Stock With MarketSmith

Want To Get Quick Profits And Avoid Big Losses? Try SwingTrader

Best Growth Stocks To Buy And Watch

Market Rally Faces Earnings Wave, Big Fed Rate Hike; What To Do

[ad_2]

Image and article originally from www.investors.com. Read the original article here.