[ad_1]

The coronavirus outbreak is first and foremost a health crisis, but it has also led to unprecedented volatility in financial markets across the globe.

So what role have exchange-traded funds (ETFs) played in the tumult?

Amid the greatest market turbulence in over a decade, ETFs have been a source of stability. And not for the first time.

ETFs successfully navigated the 2008 global financial crisis, the 2013 taper tantrum, the 2015 high-yield bond sell-off, and now the current coronavirus-driven market stresses.

Two points about ETF trading during the most volatile period, from 24 February to 27 March 2020, are worth remembering: First, many investors turned to ETFs to adjust positions and manage risk in their portfolios; and second, fixed-income ETFs served as an indispensable price-discovery mechanism, reflecting real-time prices when bond market liquidity was challenged.

Record Trading Volumes in the Face of Heightened Volatility

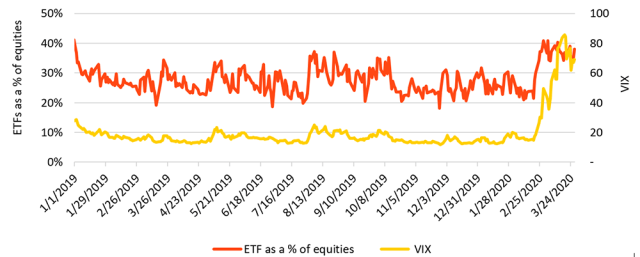

In past stressed market scenarios, ETF trading activity tended to increase when market volatility rose. This held true during the 24 February to 27 March interval.

Some data from that period are worth highlighting:1

- US-listed ETFs traded almost $6.4 trillion. By comparison, single-stock trading measured almost $11 trillion. So ETFs accounted for 37% of all equity trading. In 2019, they accounted for 27%.

- US-listed ETFs traded almost $256 billion per day on average, roughly three times their average 2019 daily trading volume.

- During the week of 9 March, ETF trading volumes in the United States surged to a record $1.4 trillion.

Investors have turned to ETFs during the current market stress for good reason: They have been efficient and effective tools for rebalancing holdings, hedging portfolios, and managing risk.

ETFs as a Percentage of Equity Trading vs. VIX

Fixed-income ETFs reflect real-time market prices.

ETF liquidity was crucial in the bond markets last month. While individual bonds trade in an opaque over-the-counter (OTC) market, fixed-income ETFs trade on-exchange, like equities. This ease of access means shares of fixed-income ETFs generally trade more often than their underlying bonds, even in calm markets.

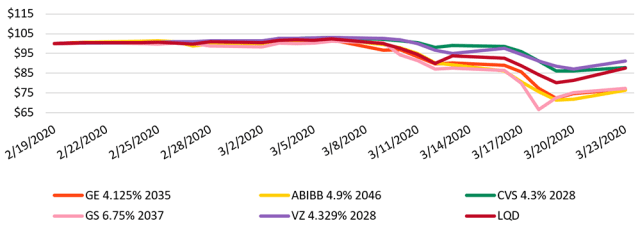

For example, fewer than 1% of the more than 21,000 publicly registered corporate bonds trade daily in the OTC market.2 On 12 March, a day of severe market dislocation, the iShares® iBoxx $ Investment Grade Corporate Bond ETF (LQD) traded almost 90,000 times on-exchange, while its top five holdings traded 37 times each on average.3

Because of this liquidity, fixed-income ETF prices incorporate more real-time information than even their most heavily traded portfolio bonds, demonstrating where there is an actionable price for the entire portfolio. This shows the power of ETFs as price discovery tools, particularly when markets are moving quickly.

This dynamic played out when bond market liquidity was under duress during the week of 9 March. Fixed-income ETFs traded at prices below their net asset value (NAV). The NAV is an estimate of the fair value of the underlying holdings, based on actual trades of portfolio bonds, estimates derived from trades of bonds from the same issuer or sector, or other market metrics. The ETF price shows what investors are actually willing to pay.

In other words, these discounts acted as “leading indicators” for underlying bond prices.

Price of LQD vs. Top Holdings, 19 February 2020 to 23 March 2020

| Name | Weight in LQD |

| GE Capital International Funding (GE) | 0.35% |

| Anheuser-Busch Companies Llc (ABIBB) | 0.31% |

| CVS Health Corp (CVS) | 0.31% |

| Verizon Communications Inc (VZ) | 0.22% |

| Goldman Sachs Group Inc. (GS) | 0.21% |

As of 23 March 2020. Holdings subject to change. For the most recent fund holdings, visit iShares.com. Information on non-iShares Fund securities is provided strictly for illustrative purposes and should not be deemed an offer to sell or a solicitation of an offer to buy shares of any security other than the iShares Funds, that are described in this material.

A common critique of ETFs, fixed-income ETFs in particular, is that they have not been tested in a stressed market environment. But in the recent stressed market environment, fixed-income ETFs provided clarity in an otherwise opaque segment of the market. At a challenging time for bond market liquidity, investors could gain (and sell) exposure by trading ETFs on-exchange.

In the worst volatility since the global financial crisis, investors looked to ETFs to transfer risk and allocate capital. In all environments, ETFs have performed as designed and provided access, liquidity, and transparency to the market.

ETFs have been tested time and time again. And each time, they have passed the test.

1. Bloomberg, BlackRock for the period 24 February 2020–27 March 2020.

2. Citigroup, “The coming revolution in credit portfolio trading” (November 2019)

3. BlackRock, TRACE (as of 12 March 2020)

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

© 2020 BlackRock, Inc. All rights reserved.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Julian Dewert

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.