[ad_1]

The COVID-19 pandemic has drastically changed many people’s financial circumstances — causing everything from job losses to increased health care expenses — and those affected have been turning to the wealth management industry for help during this difficult time. In fact, a survey by The College for Financial Planning found that 71% of advisers report they have more clients now than they did before COVID-19. Moreover, the pandemic has changed how financial advice is delivered: It has made meetings more personal, technology more integral, and advice more holistic. Even after the pandemic ends, these positive changes to the adviser–client relationship can and should continue throughout 2021 and beyond.

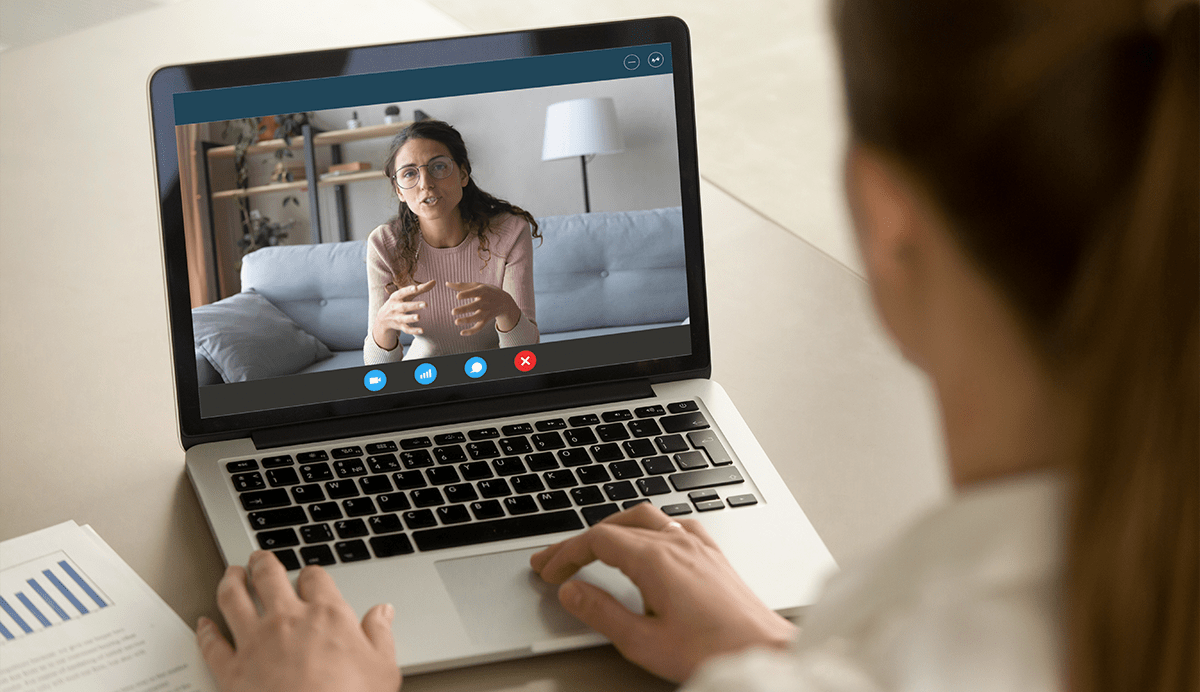

For me, one commercial truly encapsulates the wealth management industry’s role in clients’ lives during the pandemic and how working from home can strengthen the advisor–client relationship. The “J.P. Morgan Advisors Are Here for You” spot shows advisers working on their laptops at the kitchen table, from their desk, and on the couch, balancing work and childcare, and holding virtual meetings. What makes the commercial so powerful is that these scenes create common ground and help break down the barrier between adviser and client that some investors feel when they enter an adviser’s office.

Let’s keep the common ground we’ve gained.

Even when advisers start to return to the office, we as an industry should maintain some of that positive pandemic informality. For some advisers and firms that may mean continuing to hold virtual meetings with clients. These glimpses into each other’s homes and lives can do wonders for the human-to-human bond between adviser and client .

Furthermore, even advisers and firms that resume in-person interactions can take away some lessons from the virtual meetings they held during the pandemic. For instance, planning meetings don’t have to be formal business conversations. Having a relaxed and personal exchange with a client may open up new lines of conversation and create better insight into their needs.

Let’s stay ahead of the digital curve.

At the start of the pandemic, many advisers and their firms had to rush to update their technological capabilities to handle the transition to virtual. As Deloitte notes in its recent white paper on how wealth managers can recover from the pandemic and thrive, “Critical business workflows are being digitized to enable changes in both client behavior and accommodate field personnel working remotely.” For example, advisers had be able to onboard new clients and open new accounts virtually, all while managing such risks as know your customer (KYC) and SEC Regulation Best Interest disclosure requirements, Deloitte explains.

The use of digital channels across generational divides is here to stay. I’ve written and spoken a lot on the difference between digital natives — millennials and later generations who have grown up using computers — and digital immigrants. Well, living through COVID-19 has made people of all ages more comfortable with technology, and it has shaped clients’ expectations. For instance, looking forward, Deloitte anticipates that the next challenge for wealth management firms will be to provide interactive planning and performance reporting tools in either a virtual or in-person setting. The firms that do so could have an advantage when it comes to deepening their relationships with clients, Deloitte says.

Clients really do need holistic financial advice.

One of the many things that this pandemic has taught is the power and perils of the domino effect. For example, a client suffering from financial distress after a sudden job loss doesn’t just have the loss of income to worry about. They also may have concerns about their health insurance coverage, future career and earning prospects, ability to retire or pay for their children’s education costs, etc. Advisers should let clients and prospects know that they take a holistic approach to meeting their financial needs — and that they can engage with them however they prefer, both in-person and digitally.

And most of all, advisers have to listen. They have to hear their clients’ needs and demonstrate that they are not just selling a product but are working in their clients’ best interests.

It’s time for a readjustment, not back to normal.

For a long time, I’ve said that wealth managers need to adopt digital technology and a personalized approach to delivering financial advice. The pandemic has crystalized just how necessary this is. With the rollout of the COVID-19 vaccines, we can look forward to life getting back to “normal” eventually.

But to truly thrive and meet clients’ needs, the wealth management industry doesn’t need “back to normal.” Rather, we need to learn from the pandemic and embrace technology and human-to-human interactions, whether they’re through a computer screen or across a desk.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / fizkes

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.