[ad_1]

The environmental, social, and governance (ESG) fund industry reached a crossroads on 26 August 2021.

That day, investigations by the SEC and the German regulator BaFin into allegations that Deutsche Bank’s DWS had overstated the claimed ESG integration of a portion of its funds were reported in the press.

With the end of this age of innocence, ESG marketing jargon morphed into actual regulatory risk with real-world consequences: DWS stock fell ~15%, wiping €1.2 billion from the market cap, and has yet to meaningfully recover.

Potential mis-selling by DWS, a serious charge in the United Kingdom, was raised by the Financial Times and sent tremors of fear reverberating throughout the sector.

The trans-national nature of the enhanced regulatory scrutiny of the ESG fund complex represented another sea change.

The US investigation showed that the SEC’s new Climate and ESG Task Force was more than just regulatory greenwashing. Indeed, BaFin only commenced its probe into German-domiciled DWS after the SEC launched its inquiry. The German regulator would have had a hard time explaining why it wasn’t looking into allegations against a company under its direct supervision when a foreign counterpart was.

Shortly before the DWS news broke, the Financial Conduct Authority (FCA) had urged all UK asset managers to make certain that ESG fund products were adequately resourced amid the avalanche of new ESG fund launches.

Managers must balance the ESG fund sector’s parabolic growth against the higher costs of running these products and the potentially significant regulatory risks. The winners in this lucrative race will be those that can concretely demonstrate that various ESG inputs are truly integrated into products at the fund level.

This is a natural part of the sector’s maturation process. The priorities of asset owners as they allocate to ESG funds continue to evolve. The chart below, based on data from BNP Paribas, shows the speed and direction of that evolution:

Most Important Factors When Selecting an ESG Manager

| 2017 | 2019 | |

| ESG Values / Mission Statement | 38% | 27% |

| Track Record | 14% | 46% |

| ESG Reporting Capability | 11% | 29% |

Source: BNP Paribas

In 2017, a compelling ESG “mission statement” was the most critical data point in ESG manager selection.

Subsequently, fund performance and reporting took on greater import.

The manager’s ability to demonstrate how ESG considerations are incorporated into a fund’s investment and research process will be the next major selection criteria.

As recent events show, the pressure will come not just from asset owners, but increasingly from regulators and non-governmental organizations (NGOs).

Clearly, all fund products should do what they say on the tin. But given the societal importance of ESG objectives and the prioritization that most G7 governments accord them, the regulatory scrutiny of ESG funds will only grow.

There are three key priorities for asset managers running ESG funds:

- Control spiraling ESG costs, including those around data and stewardship.

- Demonstrate that fundamental and ESG considerations are incorporated at the fund level. ESG criteria in themselves are not enough. A portfolio can’t run on carbon data alone. Other fundamental data are required.

- Ensure that the quantity of ESG inputs and their integration is appropriate for the fund product. This can differ significantly between funds.

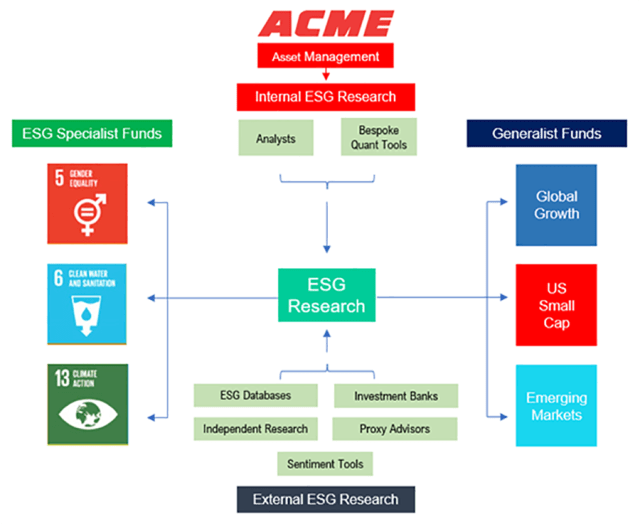

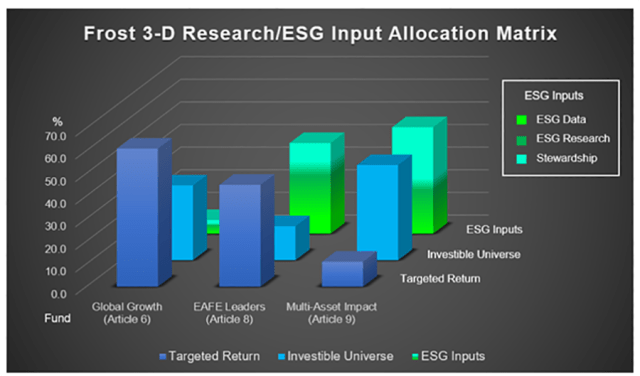

The broad spectrum of fund objectives and the diversity of ESG factors applied to the funds are depicted in the following chart:

Few managers, not even those with longstanding and sophisticated ESG processes, have overcome the challenges associated with the space. Managers must value and allocate inputs, including ESG databases and proxy advisers. These don’t lend themselves to the document / interaction counting that often drives fundamental research valuation. And different types of funds — Articles 6, 8, and 9 — mandate different considerations in different quantities.

With these challenges in mind, and based on insights from CFA United Kingdom, CFA Institute, and Stanford University, Frost Consulting has developed a three-dimensional framework for valuing and allocating ESG inputs while integrating them with fundamental research — at the fund level and across a limitless variety of multi-asset class products.

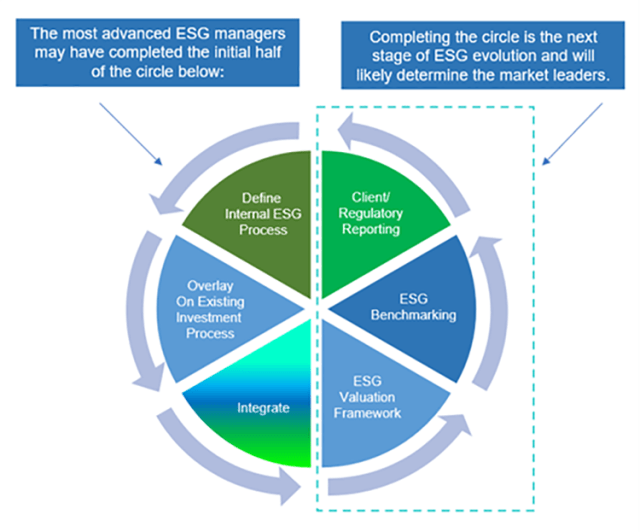

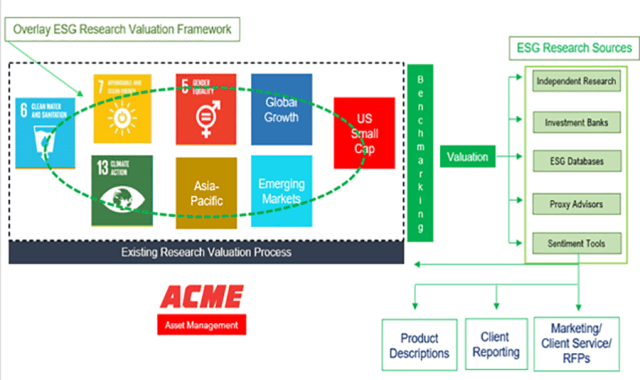

This can conclusively demonstrate to asset owners and regulators that a manager’s ESG products have sufficient and appropriate inputs, while addressing cross-subsidization issues.

This process has the capacity to bring managers “full circle” in order to systematically accelerate their ESG product launches and development across asset classes.

Managers that can meet the challenge and demonstrate true ESG integration to asset owners and consultants will be well-positioned to capture the ESG category’s growth potential.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Greg Pease

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.