[ad_1]

The J-curve narrative in private equity (PE) investments has accompanied the growth of private markets up to the present. That narrative deserves a quiet obsolescence.

Here’s why.

The J-Curve

Private market funds tend not to be invested all up front. Rather investors contractually agree to supply the necessary capital to the investment manager, over time and upon request, to finance the acquisitions that compose the investment portfolio. Portfolio investments are not sold off all at once either but are divested over time, with the related cash proceeds then returned to investors.

The J-curve describes either a PE fund’s progressive performance, as measured by the internal rate of return (IRR), or the related net cash position of the investor. While it is indeed a function of how a PE fund uses cash over time, the J-curve is more often associated with the IRR narrative. By pointing to better future results, the J-curve’s story helps mitigate the usually unpleasant effect of the IRR’s initial downward plunge — related to the high relative weight, in the IRR calculation, of the expenses and fees incurred earlier in a PE fund’s lifecycle.

The S-Curve

But the J-curve narrative has always simplified an underlying sigmoid pattern: an S-curve.

How does the S-curve evolve the J-curve concept? By modeling the impact of decreasing marginal returns relative to the self-liquidating nature of private market transactions. In their various iterations, J-curves do not properly describe time’s influence on cash flows. Time has a financial cost that makes the more distant distributions progressively less relevant and leads to marginally decreasing returns.

Without a sigmoid correction, the J-curve may suggest that “patience” will lead to more money or higher returns and that the IRR reinvestment assumption will hold true.

To understand and manage the S-curve requires a duration-based and time-weighted performance calculation strategy. Duration marks where the J becomes an S and provides the interpretative and predictive shift that sharpens the pricing and risk management perspective.

S-Curve, So What?

Investors want to better understand the risk and return outlook of their private market allocations. They want to know how it compares to those of other asset classes. They also need to measure and manage their private market pacing and overcommitment strategy.

Ex post closet-indexing comparisons have limited practical application. Gauging the S-curves, however, yields actionable and quantifiable insights in terms of both benchmarking and returns.

The portfolio management possibilities of private market investments are more complex than those of more liquid asset classes. Equity portfolios, for example, can be efficiently constructed and are easier to rebalance. They eliminate the private markets’ funding and reinvestment risk as well as their target allocation challenges.

The J-curve narrative assumes annualized and chained IRRs, as do most current PE indices and metrics. Moreover, the time-weighted rate of returns (TWRs) computed using modified Dietz methods are really just proxies for the IRR. They deliver misleading performance information. Neglecting the de-risking effect of distributions is like attributing a value of Beta=1 to non-reinvested S&P 500 dividends: It biases the portfolio risk information.

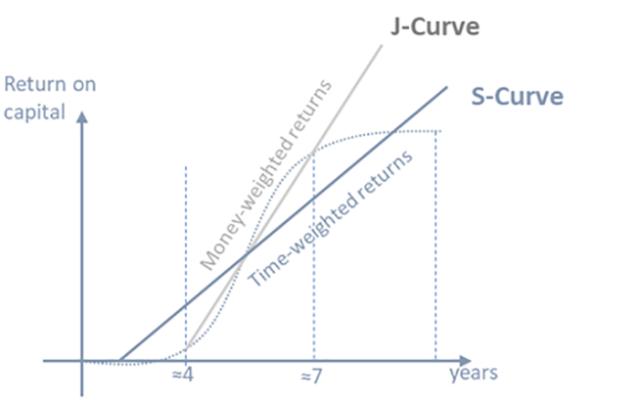

To visualize the difference, the steeper line in the following graphic shows the return outlook of the money-weighted metrics currently in use. The more conservative line reflects the true average dollar creation over time by relying on S-curve and time-weighted duration-adjusted return on capital (DARC) information.

Competing Curves: The S-Curve vs. the J-Curve in Private Equity

The J-curve line represents capital growth if IRR returns were applicable to the whole commitment and reinvestment was instant. That requires a liquid market and fairly valued NAVs trading at par. The S-curve, on the other hand, models the true dollar creation of the private fund portfolio: It puts the IRR in the context of time in a realistic investment pacing and overcommitment framework.

The underlying thesis is supported by data. The long-term median IRR is 13.3%, according to McKinsey & Company, for example, but US pension funds reported long-term PE returns of 9.3%: A realistic steady-state overcommitment strategy of 1.4x would be broadly confirmed by the 1.5x since-inception net multiple earned by a large global PE investor.1

Of course, the performance numbers aren’t the whole story. Private market investing is about more than outperformance. The risk-adjusted contribution is equally essential. That can only be estimated with S-curves and DARC-weighted returns.

That’s why incorporating the de-risking effect of durations — where the S-curves twist — is critical to both accurate benchmarking and effective portfolio management.

1. A 1.5x multiple and a related 13.3% IRR imply a net duration of over 3.2 years, approximated by using the formula linking TVPI and IRR: DUR=ln (Multiple)/ ln (1+IRR). As the net duration is forward (i.e., it does not start at time zero), a reasonably standard three-year ramping up phase pushes the total duration to 6.2 years. In a simplified calculation, the 1.5x multiple is equivalent to the annualized 6.6% DARC return since inception (i.e., 1.5^(1/6.2)-1= 6.6%) and in turn to a 9.3% time-weighted return on the steady state invested capital, which requires a 1.4x overcommitment (i.e., only 71% of the commitment is typically invested, hence the DARC return of the fund is “leveraged” to compute the return of the invested capital, 6.6%/0.71=9.3%).

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Photos by R A Kearton

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.