[ad_1]

What’s most surprising about aggregated private market performance calculations?

The widespread “tolerance” of mathematical errors, gross inaccuracy, and representativeness among private market investors, advisers, enthusiasts, detractors, and even academics.

In the traditional asset classes, investment professionals are laser-focused on every “micron” of performance difference in their attribution analyses. With private market assets, however, excessive approximation is the order of the day.

The Troubled Waters of Private Equity Performance Attribution

The variability of cash flows makes performance attribution of private market assets much more challenging: Returns aren’t generated by a stable underlying asset base, so there is no possibility of reinvestment or compounding.

As I’ve written before, today’s performance attribution toolkit is composed of metrics — internal rates of return (IRRs), total values to paid in (TVPIs), public market equivalents (PMEs), and the various alphas — that work at the single asset level at best but cannot be generalized.

So, what does generalization actually mean?

Comparability

In non-mathematical terms, generalization allows for meaningful comparisons. We should be able to tell whether a given IRR or TVPI is objectively “better” than another, that it represents more return or less risk.

Given two comparable investments, is a 15% IRR better than 10%? While the optical illusion implies that it is, in reality we can’t give an accurate response without more data. We need information about time and capital invested. That means time-weighted metrics rather than the money-weighted approximations currently in use.

That 10% IRR may be preferable if it is earned over a longer period of time, let’s say four years as opposed to two years for the 15%. This leads to a 1.4x multiple on invested capital (MOIC) for the 10%, which outpaces the 1.3x MOIC of the 15%. But we still need a duration component to reach any reasonable conclusion.

According to the IRR narrative, money recouped earlier could be reinvested at the same rate of return. But this is just an assumption. In fixed income, a prepayment is typically treated as reinvestment risk. Past returns are no guarantee of future results.

But let’s trouble the waters even more and throw another stone.

Is a 1.4x MOIC better than a 1.3x? Of course, right? In fact, it all depends on the real capital deployed versus the capital that was committed to be deployed. If the 1.4x MOIC is produced by drawn capital that is only 50% of a reference commitment and the 1.3x is made on an identical commitment that is 100% drawn, the latter outperforms the former.

Based on this logic, all derived PME and alpha calculations suffer from the same conceptual limitations. As a result, all money-weighted quartile information and rankings of and about private market investments can create significant data distortion.

Additivity

In mathematical terms, generalization implies that additivity is a precondition to any robust statistical analysis. The example above demonstrates that without accurate additivity, we can’t determine a representative average.

Financial mathematics rules dictate that averaging rates is only possible through compounding. But the IRR cannot be properly compounded over time. When IRRs are presented as annualized or horizon measures, or even worse from an accuracy standpoint as since inception returns, they can seriously misrepresent the actual returns.

But even if the IRR could be compounded as in our MOIC example, without more capital utilization information, the nature of the MOICs prevents us from properly averaging their performance.

The average IRR of our two hypothetical investments is not 12.5%, nor is the average MOIC of 1.35x the true average return. Again, we need a duration component as well as capital weighting data before we can make any meaningful estimates.

The Pooling Trap

Gross approximation is even more striking in aggregated private equity return calculations. Studies often pool cash flows, treating those from different funds as if they were from a single fund. This warps the data even more than our earlier examples.

Annualized differences worth many basis points are dealt with with no regard for mathematical accuracy or representativeness.

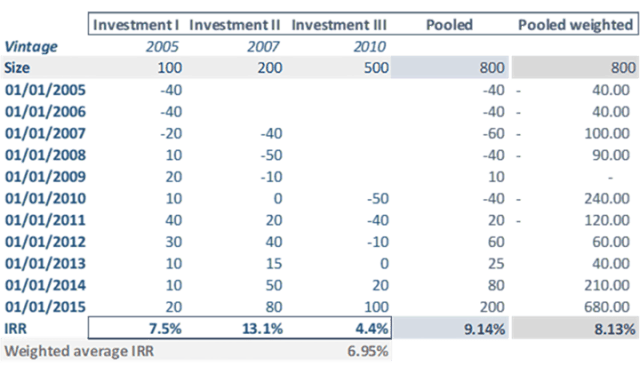

Pooling Cash Flows

The preceding table charts the cash flows of three funds of different sizes and vintages individually, pooled, and pooled and weighted. That is, the cash flows are calculated pro forma, weighting individual cash flows with the relative weight of the individual funds.

The pooled IRR of 9.14% differs from both the (mathematically incorrect) individual funds’ weighted average IRR of 6.95% and the pooled weighted IRR of 8.13%. Yet the performance number should unequivocally represent the value created by the funds.

What’s worse from an accuracy perspective is that the pooled numbers are presented as 10-year horizon returns, or since inception to the latest reporting date. So, even with the more conservative pooled weighted return, the since inception assumption suggests that the 800 pooled units of invested capital would become (1+8.13%) ^10=2.18x, or 1,748 units.

Since inception pooled returns create an obvious disconnect. The 800 units of capital invested in the three funds produced “only” 1,160 units of capital, well below the “impression” implied by the since inception pooled returns.

Unjustified confidence is often the result of since inception horizon returns. As the example shows, they generate the illusion of magnified wealth, by a factor of 1.5x in this case. This helps explain why marketing documents display far too many 10x private market benchmarks.

The DaRC Life Jacket

Some of the best advice I have ever received is to never trust the flows coming from a pool or the sea, or just aggregated calculations. Always take care.

To keep accurate information from drowning in the PE pool, the duration-adjusted return on capital (DaRC) methodology provides the necessary duration framework. It first corrects the multiples by considering the timing of the cash flows and then leverages the additivity attributes of the duration.

As a result, the pooled multiple remains in line with actual cash-flow balances: 1.45x. Then, with the proper net duration of 4.68 years, we calculate a credible average net time-weighted DaRC return of 8.39%.

To optimize allocation and risk management for a diversified portfolio, we need accurate performance numbers. But the current private market metrics too often fall short of that benchmark. We can do better.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images/PBNJ Productions

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Image and article originally from blogs.cfainstitute.org. Read the original article here.